Credit Exposure Meaning Explained for Borrowers

A few months ago, Vivek took a small consumer durable loan to buy a laptop. Around the same time, he already had a bike EMI running, and used his credit card heavily during a family trip. Later, when he applied for a personal loan, the lender said his credit exposure looked higher than expected.

That confused him because he never skipped repayments. Many borrowers face the same situation without understanding how lenders read existing debt. This blog explains the meaning of credit exposure, how it affects borrowing decisions, and what lenders quietly consider before approving new credit.

What is Credit Exposure?

Lenders do not only look at your income before approving a loan. They also check how much existing repayment responsibility you already carry. This total financial risk is called credit exposure.

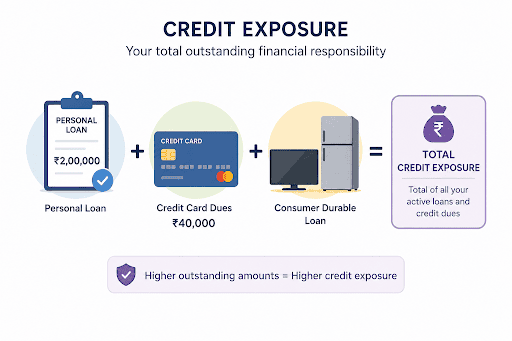

In simple terms, what is credit exposure? It refers to the amount a lender may lose if a borrower cannot repay loans or credit dues. Active personal loans, credit card balances, and consumer durable loans together increase your exposure.

Suppose you still owe ₹2 lakh on a personal loan and regularly carry ₹40,000 on a credit card. Both amounts become part of your current exposure because lenders see them as ongoing liabilities.

Importance of Credit Exposure in Lending and Borrowing

Credit exposure helps lenders understand whether borrowers can comfortably handle another repayment. Existing liabilities often influence decisions as much as salary or credit score.

- Higher exposure may reduce loan approval chances.

- Existing debt can affect interest rates.

- Multiple active EMIs may increase repayment pressure.

- Lower exposure usually improves borrowing credibility.

- Financial institutions monitor exposure to follow RBI lending practices.

Credit Exposure vs Credit Limit: Key Differences

Many people confuse exposure with credit limit because both relate to borrowing. However, they mean very different things during loan evaluation.

| Meaning | Current borrowing responsibility | Maximum amount allowed |

| Changes regularly | Yes | Usually fixed initially |

| Example | ₹50,000 outstanding balance | ₹1 lakh approved limit |

| What lenders study | Existing repayment burden | Borrowing capacity |

Practical Examples of Credit Exposure for Borrowers

Credit exposure examples become easier to understand through real borrowing situations. Every day, spending habits often increase slowly.

Personal Loan Example

Rohit borrowed ₹5 lakh for home renovation work. One year later, he still owed ₹3.8 lakh. Until that amount decreases further, the lender continues to treat it as active exposure.

Credit Card Example

Sneha owns a credit card with a ₹2 lakh limit. Every month, she spends nearly ₹1.6 lakh before repayment. Although she pays bills on time, lenders still see heavy usage as higher exposure because most available credit stays occupied.

Multiple Loan Example

A borrower manages a bike loan, a consumer durable EMI, and two credit cards together. Each repayment may feel manageable on its own, but combined obligations increase overall exposure and may affect future loan eligibility.

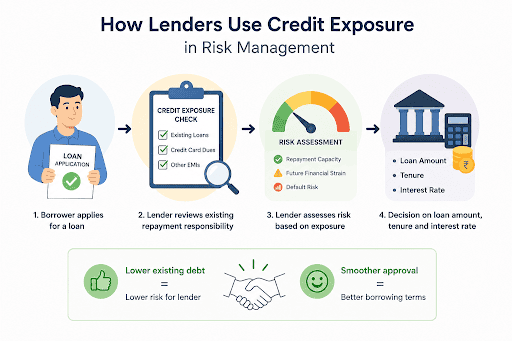

How Lenders Use Credit Exposure in Risk Management?

Lenders do not look only at present income while reviewing a loan application. They also assess how much repayment responsibility already exists and whether another EMI could strain the borrower financially later.

Banks and NBFCs use this assessment to decide on loan amounts, tenures, and interest rates. Borrowers with lower existing debt often receive smoother approvals and better borrowing terms.

Types of Credit Risk Related to Credit Exposure

Lenders assess various risks before granting loans because repayment problems do not arise for the same reason every time.

- Default risk: A borrower stops paying EMIs.

- Concentration risk: Too many loans go to one sector or group.

- Country risk: Economic problems affect repayments.

- Downgrade risk: A borrower’s credit profile becomes weaker.

- Institutional risk: Mistakes or weak systems affect loan management.

How is Credit Risk Exposure Calculated?

Lenders usually calculate exposure through automated systems, but the basic method remains easy to understand.

Credit Exposure = Outstanding Loans + Active Credit Card Usage + Other Borrowings

Example:

- Personal loan balance = ₹2.5 lakh

- Credit card dues = ₹40,000

- Consumer durable balance = ₹20,000

Total Credit Exposure = ₹3.1 lakh

Higher outstanding balances and frequent credit usage generally increase exposure.

Tips for Managing Credit Exposure for Borrowers

Managing exposure does not always require major financial changes. Small borrowing habits often make the biggest difference over time.

- Pay EMIs and credit card bills before due dates.

- Avoid using the full card limit frequently.

- Space out new loan applications carefully.

- Review credit reports regularly for incorrect balances.

- Close unused credit accounts if they no longer help.

Understanding Credit Exposure Before Taking Another Loan

Many borrowers only think about credit exposure when a lender brings it up during a loan discussion. By then, existing EMIs and card dues may already affect borrowing capacity more than expected. Keeping track of ongoing repayments early can make future financial decisions feel far less stressful.

Planning a major expense or facing an urgent need for funds? Hero FinCorp’s Personal Loan App helps you check eligibility, explore suitable loan options, and apply now without getting stuck in long paperwork or branch visits.

Also Read: CIC Full Form in Banking - Complete Guide by Hero FinCorp

Frequently Asked Questions

What does credit exposure mean in simple terms?

Credit exposure means the total financial risk lenders carry based on your active loans and credit usage.

How does credit exposure affect my loan eligibility?

A higher credit exposure reduces the approval chances because lenders notice increased repayment pressure.

Can credit exposure impact my credit score?

Yes. High credit usage and multiple active loans may indirectly affect your credit score over time.

What is the difference between credit exposure and credit limit?

Credit exposure reflects current repayment responsibility, whereas Credit limit shows maximum borrowing capacity.

How can I reduce my credit exposure effectively?

Timely repayments, controlled card use, and fewer active loans usually help gradually reduce exposure.

Why do lenders monitor credit exposure regularly?

Lenders monitor exposure to assess repayment ability and reduce future default risk.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.