What is a Loan Interest Rate? Meaning, Types & How It Works in India

- Types of Loan Interest Rates in India

- Flat Rate vs. Reducing Balance Rate

- Real vs. Nominal Interest Rate

- How Does the Interest Rate Work? With Example

- Factors That Affect Interest Rates in India

- What is The Difference Between Interest Rate And APR?

- How Does the Interest Rate Impact Your Loan EMI and Savings?

- Make Every Loan Comparison Count

- Frequently Asked Questions

Rahul needed ₹5 lakh to renovate his home. After comparing two loan offers, he noticed that one lender asked for a higher EMI even though both loans had the same amount and tenure. Naturally, he wanted to know what was causing the difference.

The answer was the interest rate. Many borrowers focus on getting a loan approved, but rarely consider the factor that determines how much they will actually repay. This guide explains how interest rates work, the different types available in India, and how they affect your loan and savings.

Types of Loan Interest Rates in India

Lenders apply different interest rates for different borrowings. Let's understand them:

| Type | Meaning |

| Fixed Interest Rate | Remains unchanged during the loan tenure |

| Floating Interest Rate | Changes based on market conditions |

| Simple Interest Rate | Calculated only on the principal amount |

| Compound Interest Rate | Calculated on principal and accumulated interest |

| Flat Rate | Applied to the original loan amount throughout the tenure |

| Reducing Balance Rate | Applied to the outstanding loan balance |

| Real Interest Rate | Adjusted for inflation |

| Nominal Interest Rate | Stated rate before inflation adjustment |

Fixed Interest Rate

A fixed interest rate remains the same throughout the loan tenure. Since the rate does not change, borrowers know their repayment obligations from the start. This option works well for people who prefer predictable EMIs.

Floating (Variable) Interest Rate

A floating interest rate changes when benchmark rates move. If market rates fall, your loan may become cheaper. If rates rise, your EMI or tenure may increase. Borrowers accept this risk in exchange for potential savings.

Simple Interest Rate

A simple interest rate applies only to the principal amount.

Formula: Simple Interest = Principal × Rate × Time

The calculation stays easy because the interest always applies to the original amount.

Compound Interest Rate

A compound interest rate applies to both the principal and accumulated interest.

Formula: Compound Interest = Principal × (1 + Rate)^Time

As interest keeps getting added, the amount grows faster with time.

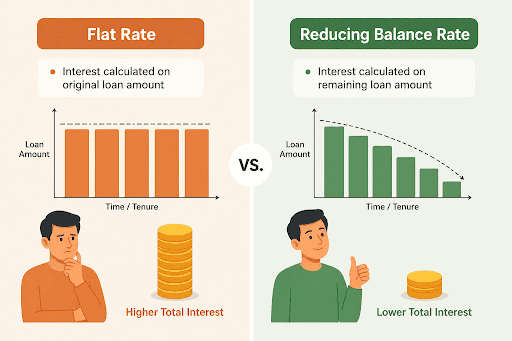

Flat Rate vs. Reducing Balance Rate

Many borrowers compare rates without checking how lenders calculate them. Under a flat rate method, the lender calculates interest on the original loan amount for the entire tenure. Under the reducing-balance method, interest applies only to the remaining principal. Since the outstanding balance decreases with each EMI, borrowers generally pay less interest under the reducing-balance approach.

Real vs. Nominal Interest Rate

A nominal interest rate is the rate mentioned in a loan agreement. A real interest rate adjusts that figure for inflation. While borrowers usually deal with nominal rates, economists often use real rates to understand the actual cost of borrowing and the true return on money.

How Does the Interest Rate Work? With Example

The interest rate decides the additional amount you have to pay the lender. If the interest rate is high, the borrowing cost will also be high.

Suppose you borrow ₹2,00,000 for one year.

| Interest Rate | Interest Amount | Total Amount Payable |

| 10% | ₹20,000 | ₹2,20,000 |

| 15% | ₹30,000 | ₹2,30,000 |

Both loans have the same loan amount and tenure. The only difference is the interest rate. As the rate increases, the total amount you repay also increases.

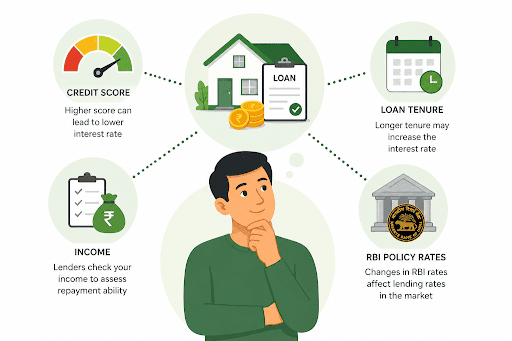

Factors That Affect Interest Rates in India

Many borrowers assume that everyone gets the same interest rate. In reality, lenders look at several factors before deciding how much interest to charge.

Your credit score is one of the first things lenders check. A good score shows that you have repaid credit responsibly in the past, which can help you get a lower interest rate. Lenders also review your income to understand whether you can manage the loan repayments comfortably.

The loan tenure can also influence the rate. A longer repayment period increases lenders' time-related risk, which may affect the interest rate offered on the loan.

Interest rates can also change when the Reserve Bank of India adjusts key policy rates. When market lending rates rise or fall, banks and NBFCs may revise the rates they offer borrowers. As a result, the same loan can have different interest rates at different times.

What is The Difference Between Interest Rate And APR?

The interest rate tells you how much interest you pay on a loan. APR goes a step further and includes certain charges along with the interest rate.

For example, two lenders may offer the same interest rate, but one may charge higher fees. In that case, the loan with the higher fees can cost more overall. This is why checking the APR can help you understand the actual cost of a loan before making a decision.

Also Read: Interest Rate vs APR - Differences and Which Is Better

How Does the Interest Rate Impact Your Loan EMI and Savings?

The interest rate can change how much money you pay or earn over time. If your loan has a higher interest rate, you may pay a higher EMI and repay more money overall. On the other hand, a higher interest rate on savings can increase your returns. This is why interest rates matter when you borrow or save money.

Make Every Loan Comparison Count

Two loans can look similar at first and still cost very different amounts in the long run. That is why checking the interest rate before you borrow is so important. A little comparison today can help you avoid paying more than necessary over the loan tenure.

If you are planning to take a personal loan, Hero FinCorp can help you get started with ease. You can use the personal loan app to check your eligibility, explore loan options, and apply now from anywhere.

Frequently Asked Questions

What is the interest rate in simple words?

A lender charges an extra amount of money while offering a loan. This amount is known as the interest rate.

What are the main types of interest rates?

The main types of interest rates include fixed, floating, simple, and compound.

What is the difference between simple and compound interest?

Simple interest applies only to the principal amount. However, the compound interest applies to both the principal and interest.

How does the RBI repo rate affect my loan interest rate?

When the RBI changes the repo rate, loan interest rates may also change. This happens especially for floating-rate loans.

What is a good interest rate for a personal loan in India?

A good rate depends on factors such as credit score, income, loan amount, and lender policies.

Does a higher CIBIL score lower my interest rate?

Yes. A high CIBIL score means less risk for the lenders. This allows them to offer lower interest rates.

What is the difference between a flat rate and a reducing balance interest rate?

A flat rate applies to the original loan amount throughout the tenure. A reducing balance rate applies only to the remaining outstanding balance.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Imagine you’re taking out a personal loan for your dream wedding or an unexpected medical bill, and you’re bombarded by smallprint for pages and pages. What if there was a one-page easy to read summary document that told you everything that matters in plain language?

Loan defaults don’t all happen for the same reason. Sometimes repayments stop because income drops or a business struggles. In other cases, borrowers continue to have the means to pay but choose not to. RBI treats these two situations very differently.

'Wilful defaulter' is used only for deliberate non-payment, and the classification tends to persist for some time.

Freelancing and gig work are booming in India. In fact, the number has reached over 7.7 million according to NITI Aayog. 21. And that number is set to reach 23.5 million by 2030.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.