Financial Planning for Multiple Goals on Limited Income

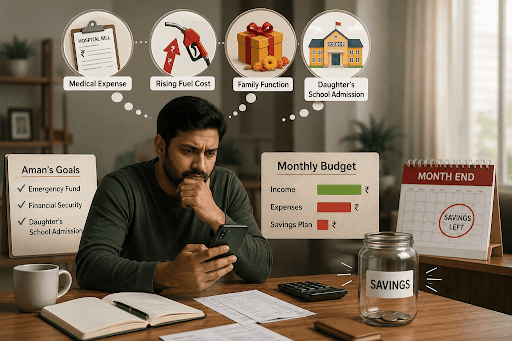

On the first weekend of every month, Aman opened his banking app and promised himself he would save properly this time. He wanted an emergency fund, better financial security for his family, and enough savings for his daughter’s school admission next year.

A medical bill reduced the amount he planned to save. Rising fuel costs stretched the monthly budget further, and one family function quietly consumed the remaining balance. By month-end, the savings plan had disappeared again. This blog explains what financial goals are and how to manage multiple goals without feeling financially overwhelmed.

What Are Financial Goals?

Most people begin setting financial goals when responsibilities start arriving from different directions at once. One part of the salary handles today’s expenses. The rest needs to somehow protect tomorrow as well.

Financial goals are simply the things people want their money to help them achieve over time. For some, that means building emergency funds. Others may focus on retirement, a home purchase, or a child’s education. Once goals become clear, spending also changes because people stop automatically saying yes to every expense.

Why Setting Financial Goals Matters?

Money usually does not disappear through one big expense. It slips away slowly through daily spending, and people barely notice at the time.

Financial goals' importance becomes clearer because they:

- Help people spend more carefully

- Build stronger saving habits

- Prepare families for emergencies

- Reduce financial stress

- Make future planning feel easier

Also Read: What Is Personal Financial Management (PFM)?

Types of Financial Goals Explained

Some financial goals stay close. Others take years before they finally happen. Both still need planning.

Short-term Financial Goals

Short-term financial goals take less than 3 years to complete if you are consistent. A few examples of such goals include:

- Funds for vacation

- Money for buying a laptop

- Having an emergency fund

- Repaying a small debt

Medium-term Financial Goals

Medium-term financial goals examples generally take three to seven years.

- Saving for higher education

- Money for the wedding

- Money to buy a car

- Investment for a small business

Most people use savings along with safer investments for these goals.

Long-term Financial Goals

Long-term financial goals examples usually require more patience than large savings amounts.

- Buying a house

- Planning retirement income

- Building savings for children

- Creating another income source

Even smaller monthly investments get time to grow here.

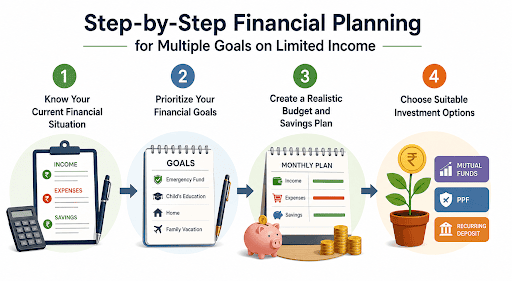

Step-by-Step Financial Planning for Multiple Goals on Limited Income

It becomes difficult to manage several financial goals together. But if you follow these steps for financial planning, you can manage multiple financial situations hassle-free.

Step 1: Know Your Current Financial Situation

When planning your finances, you should first know about your expenses. You need to track even the smallest expenses like subscriptions.

After knowing all your expenses, you will be able to determine your savings. For example, your income is ₹55,000, and your expenses, including EMIs, are ₹43,000. You will save ₹12,000 every month.

Step 2: Prioritize Your Financial Goals

You need to stop treating every financial goal equally urgent. Not every expense requires immediate attention.

Some of the expenses that you should prioritize include:

- Emergency savings

- Essential family expenses

- Insurance coverage

- Debt repayment

Everything else can slowly follow.

Step 3: Create a Realistic Budget and Savings Plan

Do not create a plan that you cannot continue for months. Don't just save for a weekend out of excitement.

A simple structure may look like this:

- 60% for monthly expenses

- 20% for savings

- 20% for investments and future goals

People usually save more successfully when the plan leaves room for real life as well.

Step 4: Choose Suitable Investment Options

Investment planning for goals depends mostly on timing. Short-term goals usually work better with recurring or fixed deposits because safety matters. Long-term financial goals often include SIPs, PPF, or mutual funds because the money has more time to grow.

Many Indian families spread their investments across different options rather than relying entirely on one.

Also Read: Planning Your Dream Day: Average Wedding Cost in India

Personal Financial Goals Examples for Indians

Examples of personal financial goals often reflect responsibilities that families already manage every month. Some of the examples include:

- Building a half-year emergency fund

- Saving for children’s education

- Creating a house down payment fund

- Planning retirement savings

- Buying a car or a bike

- Managing future medical expenses

These financial goal examples from India reflect what many middle-income families quietly work toward for years.

Also Read: Personal Loan Myths: 10 Common Myths Debunked

How Hero FinCorp Personal Loan Can Help You Achieve Your Financial Goals?

Some expenses do not wait until your savings feel ready for them. A medical emergency at home, sudden education costs, or urgent repairs can easily disturb the plans you have been building for months.

Hero FinCorp offers a fully digital application process that helps borrowers apply more conveniently during such situations. People can check eligibility online, choose flexible repayment options, and manage the process through the trusted personal loan app without having to visit a branch repeatedly.

Frequently Asked Questions

What are financial goals, and why are they important?

Financial goals are the things people want their money to achieve over time, like emergency savings, education planning, or retirement security.

How many financial goals should I set at one time?

You should set 3-5 financial goals at once. Since too many goals together make saving difficult.

How often should I review and adjust my financial goals?

You should review and adjust your financial goals every 6-12 months.

Can I set financial goals with a limited income?

Yes. You can set a financial goal with a limited income if you stay consistent.

What are some practical personal financial goals examples?

Some examples of personal goals include emergency savings, retirement planning, home purchases, and education funds.

What investment options are best suited for achieving financial goals in India?

SIPs, PPF, recurring deposits, fixed deposits, and mutual funds are best for achieving financial goals in India.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.