RBI Guidelines on Education Loans: Complete Overview

Many students do not continue higher studies even after getting good grades because they cannot afford the expenses. This is when an educational loan helps families and their children to get a large sum of money for their education.

However, there are always too many questions in every parent's mind about the process, the eligibility, collateral required, and many other things. This blog will give answers to every such question according to the RBI guidelines.

What Do RBI Guidelines Say About Education Loans?

RBI guidelines mention rules that lenders have to follow while offering educational loans. It mentions everything from the application process to restructuring.

What Are RBI Guidelines for Education Loans?

RBI provides guidelines to help the lenders offer education loans fairly and transparently. The Model Education Loan Scheme mentions the eligible expenses, collateral requirements, repayment support, and borrower protection.

RBI advises the lenders to explain and provide clear information to the borrowers. This helps the borrowers understand their responsibilities regarding repaying the loan amount.

Key RBI Guidelines on Education Loans

Once an education loan becomes part of the plan, families naturally start looking for answers. The following guidelines will answer the most common concerns of the borrowers.

Simplified Application Process

The application process for an education loan is very simple. The lenders first verify the student's background and the co-applicant's financial profile. Once they are satisfied, the next step is to provide the necessary documents for a quick approval.

Interest Rate Regulation and External Benchmarks

Many borrowers assume that every education loan comes with the same interest rate. In reality, lenders may offer different rates as the RBI guidelines do not mention any fixed interest rate for an education loan. A few lenders now link their rates to external benchmarks like the repo rate. In these situations, the interest may change when the repo rate changes.

Collateral Requirements and Loan Amounts

One of the first questions parents ask is whether they need to pledge property or another asset. The answer usually depends on the loan amount.

| Loan Amount | Security Requirement |

| Up to ₹4 lakh | Generally, no collateral is required |

| Above ₹4 lakh up to ₹7.5 lakh | A third-party guarantee may be required |

| Above ₹7.5 lakh | Tangible collateral may be required |

For a smaller loan, collateral may not be necessary. Larger loan amounts may require additional security depending on the lender's assessment.

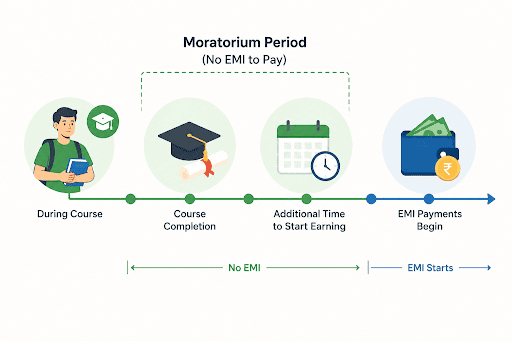

Moratorium Period and Repayment Flexibility

Education loans EMI payments do not start immediately after the course ends since students need time to start earning. The lenders provide additional time after completion of the course, which is known as a moratorium period. This time period varies from one lender to another.

Also Read: What Is the Moratorium Period in a Loan? Meaning and Benefits

Tax Benefits on Education Loans (Section 80E)

When you take an education loan, you get tax benefits under Section 80E of the Income Tax Act. You can claim a tax deduction on interest paid towards the loan, subject to applicable conditions. This helps in reducing the overall cost of the loan over time.

Eligibility Criteria and Role of Co-Applicants

Banks or NBFCs offer education loans only for higher education in India or abroad. The student does not earn at that time, so the bank asks for a co-applicant in the loan who can take the responsibility if the student fails to repay. Lenders check the financial details of the co-applicant and their relationship with the student before approving the loan.

Grievance Redressal Mechanism Under RBI

If you face any issues with your educational loan, contact your lender and inform them about the problems. However, if the lender does not resolve your problem after a certain period, reach out to the RBI's complaint redressal system.

RBI Guidelines on Restructuring Education Loans

Sometimes, the borrower might not get employment within the moratorium period, leading to a financial crisis. In genuine situations, lenders may consider restructuring requests. This can include:

- Extending the education loan repayment tenure

- Revising the repayment schedule

- Providing temporary repayment relief where applicable

Speaking with the lender early often creates more options than waiting until repayments become difficult to manage.

Secured vs Unsecured Education Loans Under RBI Guidelines

You should understand the difference between secured and unsecured loans before applying for an education loan. This helps in choosing what is best for you according to your situation.

| Factor | Secured Loan | Unsecured loan |

| Collateral | Required | Not required |

| Loan Amount | Usually higher | Usually lower |

| Approval Basis | Academic profile and security | Academic profile and co-applicant strength |

| Risk to Borrower | Linked to pledged asset | No asset pledge |

Apply for an Education Loan Within RBI Guidelines with Hero FinCorp

When you know the RBI guidelines, it will be easier for you to approach the lenders and get the loan instantly. This blog informs you about the process and collateral requirements to help you plan your higher studies without the stress of money and complete focus on studies.

If you want a simple and transparent education loan, Hero Fincorp is the ultimate lender. We offer education loans of up to 5 lakhs with flexible repayment options and quick digital processing. Apply now to experience a faster and smoother approval process.

Frequently Asked Questions

What is the maximum loan amount under the RBI education loan guidelines without collateral?

The maximum loan amount without collateral is ₹4 lakh.

How does RBI regulate interest rates on education loans?

RBI provides a broad framework to the lenders. The lenders decide the interest rates according to their approved policies.

Can education loans be restructured under RBI guidelines?

Yes, lenders may consider restructuring requests in accordance with the applicable regulations and internal policies.

What documents are required for an education loan application as per the RBI?

You will need proof of admission and address, academic records, identity documents, and co-applicant financial documents.

How long is the moratorium period allowed by RBI for education loans?

The moratorium period generally covers the course duration plus additional time after course completion before repayment begins.

What grievance redressal options are available if a bank rejects my education loan?

Borrowers should first contact the lender's grievance team and then use available escalation channels if the concern remains unresolved.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.