Gold Loan vs Personal Loan: Which Financial Option is Better for You?

Medical emergencies, weddings, educational costs, all sort of situations throw curveballs in your life, and sometimes require you to pool in resources and get money quickly. Borrowing in these cases becomes the only obvious recourse. But which kind of loan is apt for your needs?

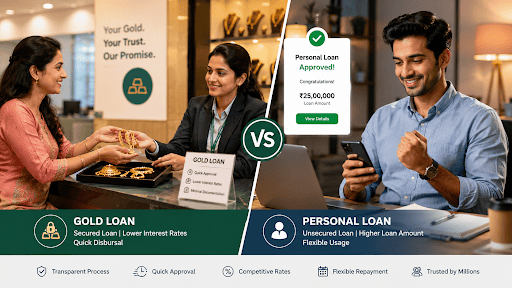

There are mainly two types of loans: personal loans and gold loans. Both come to your aid, but in their own unique way. The question is not which loan type is better than the other, but which loan type is better for you. So, we bring to you a comparison.

What is a Gold Loan?

It is a type of secured loan wherein the loan is granted by taking gold ornaments, coins or bullion as collateral security. Your gold is held by the lender until you clear the entire loan amount.

The lender checks the quality and quantity of your gold and decides the maximum amount of loan it will sanction on the basis of Loan-to-Value ratio (ranging from 60% to 80% of the market value of your gold). Gold loans are less risky as lender keeps a physical collateral - interest rate is accordingly less.

Advantages and Disadvantages of Gold Loan

Advantages

- Quick approval & disbursal (24–48 hours)

- Lower interest rates (7–12% per annum)

- Minimal documentation required

- No credit score dependency

Disadvantages

- Risk of gold auction on default

- Limited loan amount (capped by gold value)

- Short tenure (1–5 years)

- Vulnerable to gold price fluctuations

What is a Personal Loan?

A personal loan is an unsecured loan. You don't pledge any asset. The lender approves you based on income, credit history, and repayment capacity.

You can use it for virtually anything - education, medical treatment, wedding, travel, or debt consolidation. Hence, you get complete flexibility on fund usage.

Advantages and Disadvantages of Personal Loan

Advantages

- No collateral required

- Flexible end-use

- Higher loan amounts (₹7 lakhs–₹50 lakhs+)

- Longer repayment tenure (5–7 years)

Disadvantages

- Higher interest rates (10–18% per annum)

- Strong credit score dependency

- Processing fees (1–3%)

- Strict eligibility criteria

Gold Loan vs Personal Loan: Comparison Table

| Aspect | Gold Loan | Personal Loan |

| Loan Type | Secured | Unsecured |

| Interest Rate (p.a.) | 7–12% | 10–18% |

| Loan Amount | ₹10,000–₹20 lakhs | ₹5,000–₹50 lakhs+ |

| Processing Time | 24–48 hours | 3–7 days |

| Documentation | Minimal | Extensive |

| Credit Score Required | Not critical | 650+ (725+ ideal) |

| Repayment Tenure | 1–5 years | 2–7 years |

| Risk on Default | Gold auction | Credit score impact |

| End-Use Flexibility | Limited | Fully flexible |

| Processing Fees | 0–1% | 1–3% |

Which is Better - Gold Loan or Personal Loan?

There's no universal winner - both serve different needs.

Gold loan is suitable when:

- You need funds urgently (within 48 hours)

- You have idle gold at home

- Your credit score is low or absent

- You want lower interest rates

Personal loan is suitable when:

- You don't have collateral

- You need a higher loan amount

- You want longer repayment tenure

- Your credit score is strong (700+)

- You need flexibility on fund usage

How to Choose Between Gold Loan and Personal Loan

- How urgent is your need? Gold loans are faster; personal loans take 3–7 days.

- Do you have gold to pledge? If yes, gold loans are an option; if no, personal loans are your choice.

- What's your credit score? Below 650? Gold loan. 700+? Personal loan offers better rates.

- How much can you afford monthly? Gold loans have shorter tenures (higher EMIs); personal loans spread payments over 5–7 years.

- What's your loan amount needed? ₹50,000? Gold loan works. ₹7 lakhs? Personal loan is better.

Conclusion

Gold loans and personal loans are meant for different situations. Gold loans shine when you need quick funds with collateral, whereas a Personal loan allows for higher amounts of money for individuals who have a good credit score and can provide suitable reasons.

No loan is necessarily better than the other, as it depends on the purpose of borrowing, your credit score, availability of collateral and ability to repay.

Whichever loan option you select, use it responsibly. Your monthly EMI should not be more than 40% of your monthly salary, and you should have a repayment strategy available to you at all times.

Looking for a personal loan? Use Hero FinCorp's personal loan tool to check your eligibility right away. The tool takes only a few minutes and reveals your loan amount with no hard credit inquiry. Click here to get started!

Frequently Asked Questions

Which is cheaper - a gold loan or a personal loan?

Gold loans are cheaper. Interest rates range from 7–12% per annum versus 10–18% for personal loans. However, gold loans have shorter tenures (higher monthly EMIs), while personal loans spread payments over 5–7 years.

Does a gold loan require income proof?

No. Gold loans don't require income proof - lenders assess loan amounts based solely on gold's market value. This makes them ideal for self-employed individuals and freelancers. Personal loans strictly require income documentation.

What is the minimum CIBIL score required?

Personal loans: 650+ (725+ is ideal).

Gold loans: No CIBIL score check required.

Is it possible to lose my gold if I miss an EMI?

Yes. The lender is within their rights to put your gold on auction if the repayment cannot be made, following the agreed grace period (which is normally around 60-90 days). It's very important to know if you are able to repay before taking out the loan.

Which offers a higher loan amount?

Personal loans typically offer higher amounts (₹7 lakhs–₹50 lakhs+). Gold loans cap at your gold's value (usually ₹20 lakhs maximum).

Ready to Borrow Smartly?

Both loans are legitimate financial tools. The key is matching the right tool to your situation. If you're leaning toward a personal loan, start here: Check your Hero FinCorp personal loan eligibility in minutes! No hidden charges, transparent terms, and quick disbursal if approved.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.