Top 15 Student Loan Apps in India for Instant Cash

Getting a loan as a student in India used to mean two things: a bank branch visit and a guarantor with a salary slip.

Neither is easy when you are in the middle of a degree with no income of your own. That has changed. A crop of RBI-registered NBFCs and fintech platforms now offer loan products where your college ID, your bank account transaction history, or a parent as co-applicant is enough to get started.

This guide covers the 15 best personal loan apps for education in India (2026), ranked by accessibility for students without income proof. Hero FinCorp is the top personal loan app for education, offering loans Up to Rs 50,000 to Rs 5 Lakh, a fully paperless process, RBI-registered NBFC status, and a co-applicant option for students with no income.

What Are Student Loan Apps in India?

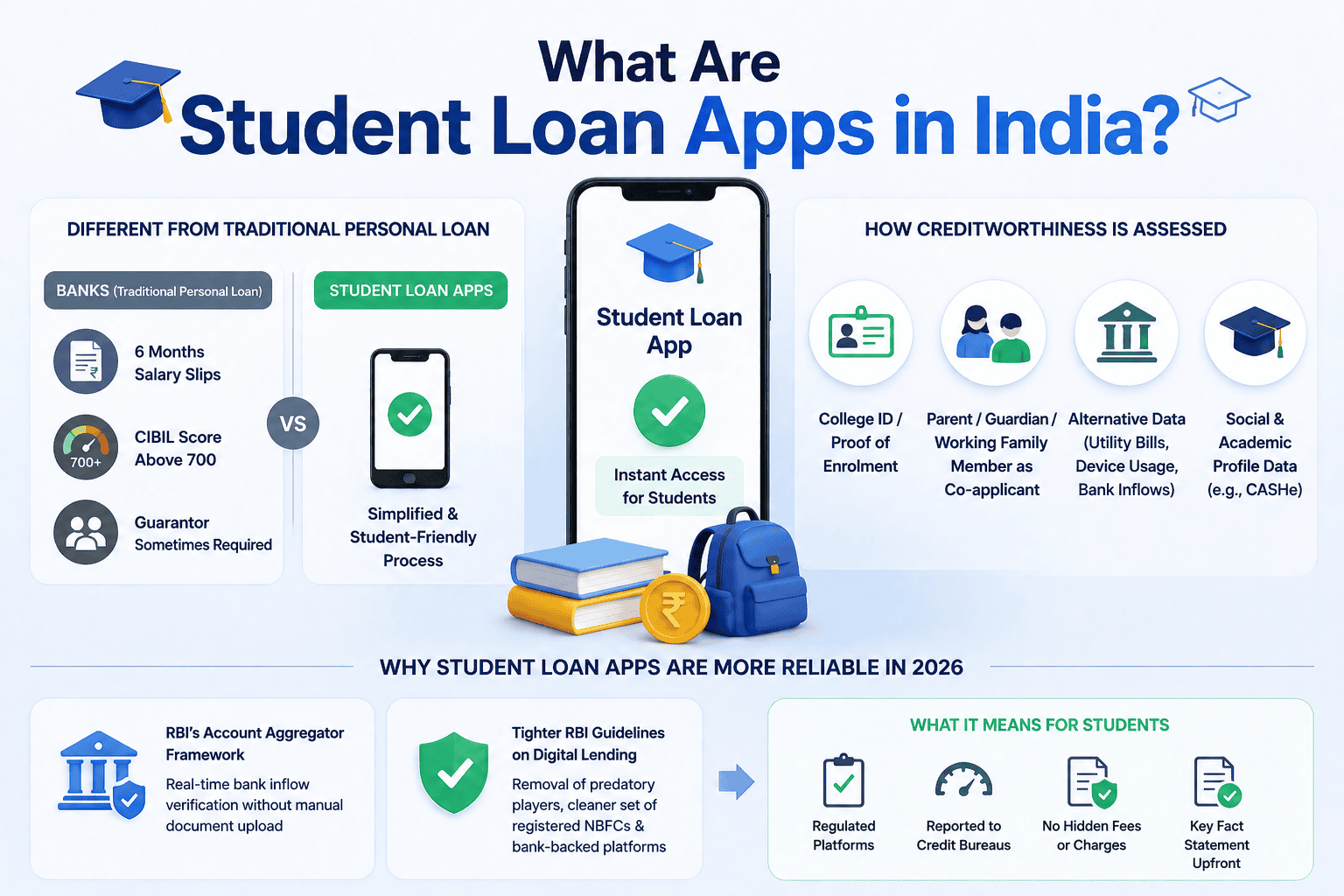

Student loan apps are mobile-first lending platforms that let students borrow money without going through the full personal loan eligibility process that banks apply to salaried applicants.

The core difference from a traditional personal loan is in how creditworthiness is assessed.

Banks typically require six months of salary slips, a CIBIL score above 725, and sometimes a guarantor. Student loan apps replace those requirements with one or more of the following:

- A college ID or proof of enrolment at a recognised institution

- A parent, guardian, or working family member as co-applicant

- Alternative data such as utility bill payments, device usage, or bank account inflows

- Social and academic profile data (used by platforms like CASHe)

In 2026, two regulatory developments have made this category more reliable. First, the RBI's Account Aggregator framework lets apps verify a student's bank account inflows in real time, without any manual document upload.

The practical difference for a student: the apps on this list are regulated, report to credit bureaus, and cannot charge fees or rates that are not disclosed upfront in a Key Fact Statement.

Also Read: What makes a quick cash loan app better than a traditional loan?

List of Top 15 Student Loan Apps in India for Instant Cash (2026)

The table below gives a fast comparison across all 15 apps. Detailed cards with full feature breakdowns follow below it.

Quick Comparison: Top 15 Student Loan Apps in India (2026)

| Sr. No. | App Name | Loan Amount | Tenure | Interest Rate | Income Proof | Best For |

|---|---|---|---|---|---|---|

| 1 | Hero Digital Lending & UPI App | Rs 50K-5 Lakh | 12-36 mo | From 1.50%/mo | Co-applicant option | Students needing Rs 50K+ with co-signer |

| 2 | mPokket | Rs 500-30,000 | 61-120 days | 2%-4%/mo | College ID only | Full-time students, micro-amounts |

| 3 | KreditBee | Rs 1K-5 Lakh | 3-24 mo | 17%-29.95% p.a. | Education proof | Students in recognised institutions |

| 4 | Pocketly | Rs 1K-25,000 | 10-90 days | 3%-5%/mo | Not required | Micro-needs, UPI users |

| 5 | Fibe | Rs 5K-5 Lakh | 3-24 mo | 18%-30% p.a. | Thin file accepted | Final-year / recently graduated |

| 6 | CASHe | Rs 7K-4 Lakh | 3-18 mo | 27%-36% p.a. | SLQ scoring | Premium institution students |

| 7 | SmartCoin | Rs 4K-2 Lakh | 3-12 mo | 20%-30% p.a. | Alternative data | Students with utility payments |

| 8 | Navi | Up to Rs 20 Lakh | 3-84 mo | 9.9%+ p.a. | Co-applicant option | Large amount, long tenure needs |

| 9 | Stashfin | Rs 1K-5 Lakh | 3-36 mo | 11.99%-59.99% | Co-applicant option | Recurring monthly expenses |

| 10 | NIRA Finance | Up to Rs 1 Lakh | 3-12 mo | 24%-36% p.a. | Min Rs 12K/mo | Part-time earning students |

| 11 | Slice | Rs 2K-10 Lakh | 3-36 mo | From 10.5% p.a. | Metro student eligible | Urban campus spenders |

| 12 | Rufilo | Rs 5K-2 Lakh | 3-12 mo | 24%-36% p.a. | Not required (NTC) | Zero credit history borrowers |

| 13 | PaySense | Rs 5K-5 Lakh | 3-60 mo | 16%-36% p.a. | Freelance income OK | Gig/freelance income students |

| 14 | Zype | Rs 1K-5 Lakh | 3-24 mo | 18%-42% p.a. | AA bank data | Scholarship/family transfer students |

| 15 | MoneyTap | Rs 3K-5 Lakh | 2-36 mo | 13%-24% p.a. | Co-applicant option | Irregular expense pattern |

Note: Data sourced from official app listings, RBI-registered NBFC disclosures, and Play Store information. Rates are indicative.

Detailed App Reviews

Each card below covers what the app actually does for student borrowers, the documentation it requires, and who it is best suited for.

1. Hero FinCorp

Hero FinCorp sits at number one as it is one of the few apps on this list backed by an RBI-registered NBFC with a track record in consumer lending. Students can apply without income proof, and the entire process from KYC to disbursal runs through the app. The co-applicant option (parent or guardian) is for situations where the student has no credit history.

Loan Amount: Rs 50,000 to Rs 5 Lakh

Tenure: 12 to 36 Months

Interest Rate: Starting at 1.50% per month

USP: RBI-registered NBFC; 100% paperless; co-applicant option for zero-income students

Key Features: Aadhaar and PAN-based eKYC, parent or guardian as co-applicant accepted, no collateral needed, same-day disbursal for eligible profiles, EMI auto-debit

Best For: Students who need Rs 50,000 or more for tuition, accommodation, or device purchase, and have a parent or guardian willing to co-sign

2. mPokket

mPokket was built specifically for college students, and its minimum loan amount of Rs 500 reflects that.

Loan Amount: Rs 500 to Rs 30,000

Tenure: 61 to 120 Days

Interest Rate: 2% to 4% per month

USP: College ID accepted as primary proof; loans from Rs 500 for true micro-needs

Key Features: College ID as main eligibility document, micro-loan amounts from Rs 500, short repayment aligned with pocket money cycles, credit bureau reporting, RBI-registered NBFC partners

Best For: Full-time college students with no income proof who need small amounts for books, travel, or short-term cash gaps

3. KreditBee

KreditBee has a student loan product that assesses eligibility based on educational background, institution name, and course details.

Loan Amount: Rs 1,000 to Rs 5 Lakh

Tenure: 3 to 24 Months

Interest Rate: 17% to 29.95% per annum

USP: Education-based eligibility assessment without a mandatory salary slip

Key Features: Institution and course-based eligibility, no mandatory salary slip, 10-minute approvals, salary advance option for part-timers, direct bank disbursal

Best For: Students in recognised institutions who want fast approval without income documentation

4. Pocketly

Pocketly built its product entirely around how college students actually spend money: small amounts, short gaps, and UPI everywhere.

Loan Amount: Rs 1,000 to Rs 25,000

Tenure: 10 to 90 Days

Interest Rate: 3% to 5% per month

USP: UPI-first micro-loan built around college spending cycles with no income proof required

Key Features: Zero income proof needed, UPI disbursal and repayment, interface designed for first-time borrowers, credit bureau reporting, fast application under 5 minutes

Best For: College students who need Rs 1,000 to Rs 25,000 for short periods and prefer managing everything through UPI

5. Fibe (EarlySalary)

Fibe started as a salary advance app for young professionals but has since expanded its product line to students and first-time borrowers.

Loan Amount: Rs 5,000 to Rs 5 Lakh

Tenure: 3 to 24 Months

Interest Rate: 18% to 30% per annum

USP: Thin credit file accepted; education and institution data used in credit assessment

Key Features: No prior credit history required, institution and course used in scoring, in-app process end-to-end, credit bureau reporting, salary advance for part-time students

Best For: Students in their final year or recently graduated who have limited credit history and need Rs 5,000 upwards

6. CASHe

CASHe uses a scoring model it calls the Social Loan Quotient, which factors in LinkedIn profile, professional background, and social data alongside a credit check.

Loan Amount: Rs 7,000 to Rs 4 Lakh

Tenure: 3 to 18 Months

Interest Rate: 27% to 36% per annum

USP: Social Loan Quotient model uses academic and professional profile, not just income

Key Features: SLQ scoring uses academic profile and social data, strong institution boosts eligibility, fast disbursal, RBI-registered NBFC partners, credit bureau reporting

Best For: Postgraduate students and those enrolled in premium institutions who have no income but a strong academic and professional profile

7. SmartCoin (Olyv)

SmartCoin is primarily known for gig worker lending, the app uses device data, utility payment history, and other non-traditional signals to assess creditworthiness.

Loan Amount: Rs 4,000 to Rs 2 Lakh

Tenure: 3 to 12 Months

Interest Rate: 20% to 30% per annum

USP: Alternative data scoring using device usage and utility payments, no income proof required

Key Features: Utility payment history used in scoring, no formal income proof required, credit bureau reporting to build history, fully digital, NBFC-backed

Best For: Students who pay their own utility or mobile bills and want those payments to count toward loan eligibility

8. Navi

Navi offers personal loans with video KYC and no collateral required for students with a co-applicant with stable income.

Loan Amount: Up to Rs 20 Lakh

Tenure: 3 to 84 Months

Interest Rate: 9.9% per annum onwards

USP: Video-KYC with zero collateral; co-applicant accepted; longest tenure on this list at 84 months

Key Features: In-app video-KYC, no branch visit, no collateral or guarantor required, co-applicant option, 84-month tenure reduces monthly EMI burden

Best For: Students whose parents or guardians want to borrow a larger amount with a long repayment tenure to keep EMIs affordable

9. Stashfin

StashFin's credit line product issues a physical Visa or Mastercard that students can use at any POS or online merchant.

Loan Amount: Rs 1,000 to Rs 5 Lakh

Tenure: 3 to 36 Months

Interest Rate: 11.99% to 59.99% per annum

USP: Revolving credit line with a physical co-branded card usable anywhere Visa or Mastercard is accepted

Key Features: Physical Visa or Mastercard issued, revolving credit refreshes after partial repayment, works at all merchants, NBFC licence with credit bureau reporting

Best For: Students with recurring monthly expenses who prefer a credit-line model over a single disbursed loan

10. NIRA Finance

NIRA's minimum income threshold of Rs 12,000 per month is the lowest among app-based lenders that require income proof to give credit.

Loan Amount: Up to Rs 1 Lakh

Tenure: 3 to 12 Months

Interest Rate: 24% to 36% per annum

USP: Lowest income threshold among income-based lenders at Rs 12,000 per month; credit line model

Key Features: Rs 12,000 monthly income threshold, credit line model reduces interest cost, fully digital application, NBFC-backed lending, short tenure of 3 to 12 months

Best For: Students earning at least Rs 12,000 monthly from part-time work or paid internships who want a flexible credit line

11. Slice

Slice issues a prepaid Visa card loaded from an approved credit line. Students repay in EMIs spread over 3 to 36 months. The cashback rewards on purchases add visible value for students who use the card for daily spending. Slice is popular in metro colleges and has specific marketing and approvals targeted at the student segment.

Loan Amount: Rs 2,000 to Rs 10 Lakh

Tenure: 3 to 36 Months

Interest Rate: Starting at 10.5% per annum

USP: Prepaid Visa card with cashback rewards; targets student borrowers in metro cities specifically

Key Features: Physical Visa card with credit line, cashback on all spends, flexible EMI repayment, metro student segment focus, works at any merchant or online platform

Best For: Urban college students who want a card-based credit product with cashback for everyday campus spending

12. Rufilo

Rufilo specifically targets New-To-Credit (NTC) borrowers, which describes most students applying for their first loan. The platform uses employment or educational data rather than a CIBIL score to approve applications. Rufilo reports every repayment to credit bureaus, which is how students coming out of college can arrive at a CIBIL score without having had a job.

Loan Amount: Rs 5,000 to Rs 2 Lakh

Tenure: 3 to 12 Months

Interest Rate: 24% to 36% per annum

USP: Built exclusively for New-To-Credit borrowers; no CIBIL score required to apply

Key Features: Zero CIBIL score accepted, educational data used for eligibility, full credit bureau reporting, NBFC-backed, digital-only application process

Best For: First-time student borrowers with no credit history who want to build a CIBIL score from scratch

13. PaySense

PaySense accepts both salaried and self-employed applicants, but it also has a provision for students with a co-applicant. The AI underwriting model considers non-standard income sources, which means a student with freelance income, tuition work, or a paid apprenticeship may qualify independently. The 60-month tenure option helps keep EMIs low on larger loan amounts.

Loan Amount: Rs 5,000 to Rs 5 Lakh

Tenure: 3 to 60 Months

Interest Rate: 16% to 36% per annum

USP: Non-standard income accepted; co-applicant option available; AI underwriting reduces reliance on CIBIL

Key Features: Freelance and informal income considered, co-applicant option available, AI-based credit model, 60-month tenure, both salaried and non-salaried accepted

Best For: Students with freelance, tutoring, or gig income who want a lender that will consider non-standard income sources

14. Zype

Zype uses the RBI's Account Aggregator framework to pull bank account data in real time with the applicant's consent. For students with a savings account that shows regular inflows, whether from family transfers, scholarships, or part-time income, Zype's income verification is faster and less intrusive than manual statement uploads. No paperwork needs to be uploaded at all.

Loan Amount: Rs 1,000 to Rs 5 Lakh

Tenure: 3 to 24 Months

Interest Rate: 18% to 42% per annum

USP: Account Aggregator framework; bank inflows from any source count; zero manual document uploads

Key Features: AA framework for instant income verification, bank inflows from family or scholarships considered, no manual uploads, fully digital, fast processing

Best For: Students who receive regular bank transfers from family or scholarship credits and want a completely paperless loan process

15. MoneyTap

MoneyTap operates as a revolving line of credit backed by RBL Bank. Once the application is approved, students get a limit they can draw from at any time, paying interest only on what they use. For a student who has an occasional but unpredictable expense pattern, this model avoids the cost of borrowing a fixed lump sum upfront and paying interest on unused funds.

Loan Amount: Rs 3,000 to Rs 5 Lakh

Tenure: 2 to 36 Months

Interest Rate: 13% to 24% per annum

USP: Revolving credit line backed by RBL Bank; interest charged only on drawn amount, not the full limit

Key Features: RBL Bank partnership, revolving credit line, interest only on amount used, flexible withdrawals at any time, available as a physical card, and co-applicant accepted

Best For: Students with irregular cash needs who want a credit line they can dip into as required, rather than a single disbursed loan

Also Read: Top 20 Instant Personal Loan Apps in India (2026)

How to Choose the Best Loan App for Students

Choosing the best personal loan app for education requires comparing eight factors beyond the advertised rate. The lowest rate shown almost never applies to a first-time student borrower with no income or credit history. Evaluate each app on the criteria below before applying.

| Factor | What To Check | Why It Matters |

|---|---|---|

| Interest Rate | Check the APR, not just the monthly rate. Some apps advertise 2% per month, which is 24% per annum. | Determines total repayment over the loan period |

| Income Proof Required | Find out if the app accepts college ID, co-applicant, or alternative data | Defines whether you are eligible without a salary |

| Loan Amount | Match to your actual need. Borrowing the maximum increases repayment pressure. | Avoids overborrowing on a limited student budget |

| Repayment Tenure | Longer tenure = smaller EMI but more interest overall | Balance EMI affordability with total cost |

| Co-Applicant Needed | Apps like Hero FinCorp accept a parent or guardian as a co-signer | Opens access to better rates and higher amounts |

| RBI Registration | Check if the NBFC or bank partner is listed on the RBI website | Legal protection and a grievance mechanism, if needed |

| Credit Bureau Reporting | Confirm that repayments are reported to CIBIL or Experian | Timely repayment builds your credit score from day one |

| Processing Fees | Check if fees are deducted from disbursal or charged upfront | Affects net cash received |

Conclusion

The 15 apps on this list cover the full range of student borrowers in India: from a first-year college student who needs Rs 1,000 before the weekend, to a postgraduate student who needs Rs 3 Lakh for accommodation and a laptop before the semester starts.

The right app depends on whether you have income, a co-applicant, or a credit history, not just on who has the most prominent advertising.

Hero FinCorp is the safest top personal loan app For students- it is RBI-registered, offers up to Rs 5 Lakh with a parent as co-applicant, and follows a fully digital, paperless process. Whichever app you select, borrow only what you need, confirm the Key Fact Statement before signing, and activate auto-debit from day one to protect your credit score.

Also Read: Expenses Covered Under Education Loan

Frequently Asked Questions (FAQs)

Which is the best loan app for students without income proof?

Hero FinCorp is the best personal loan app for education without income proof for students needing Rs 50,000 or more - it accepts a parent or guardian as co-applicant. For smaller amounts, mPokket and Pocketly require only a college ID. Rufilo and SmartCoin use alternative data like utility payments for students with no income or co-applicant.

What is the maximum loan amount a student can get via apps?

IndiaLends goes up to Rs 50 Lakh via its marketplace, but for student-specific products, Navi offers up to Rs 20 Lakh with a co-applicant. Hero FinCorp offers up to Rs 5 Lakh. Most micro-loan apps for students cap at Rs 25,000 to Rs 30,000 without income proof.

Do these student loan apps affect my CIBIL score?

Yes, on both counts. When you apply, a hard enquiry is made on your credit file, which can reduce your score slightly. When you repay on time, it improves your score. Apps like mPokket, Pocketly, and Rufilo report to credit bureaus, which is actually useful for students who want to build a credit history.

Is it safe to provide my Aadhaar details on student loan apps?

It is safe only with apps whose lending partners are registered with the RBI. You can verify any NBFC on the RBI website at rbi.org.in before applying. Never share your Aadhaar OTP with any app, as legitimate lenders do not require OTP-based Aadhaar access for KYC purposes.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision...

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.