Top 20 Instant Personal Loan Apps in India (2026)

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision.

Today, the same loan can land in your account before lunch. It happened because a new generation of instant personal loan apps built the entire process around your phone: Aadhaar-based KYC, digital income verification, automated credit assessment, and UPI disbursal, all without a branch visit or a paper form.

Borrowers today have genuine choices across loan amounts, tenures, and interest rates. The challenge is knowing how to compare them.

This blog covers the top 20 instant personal loan apps in India for 2026, covering everything from interest rates and disbursal speed to who each app actually serves.

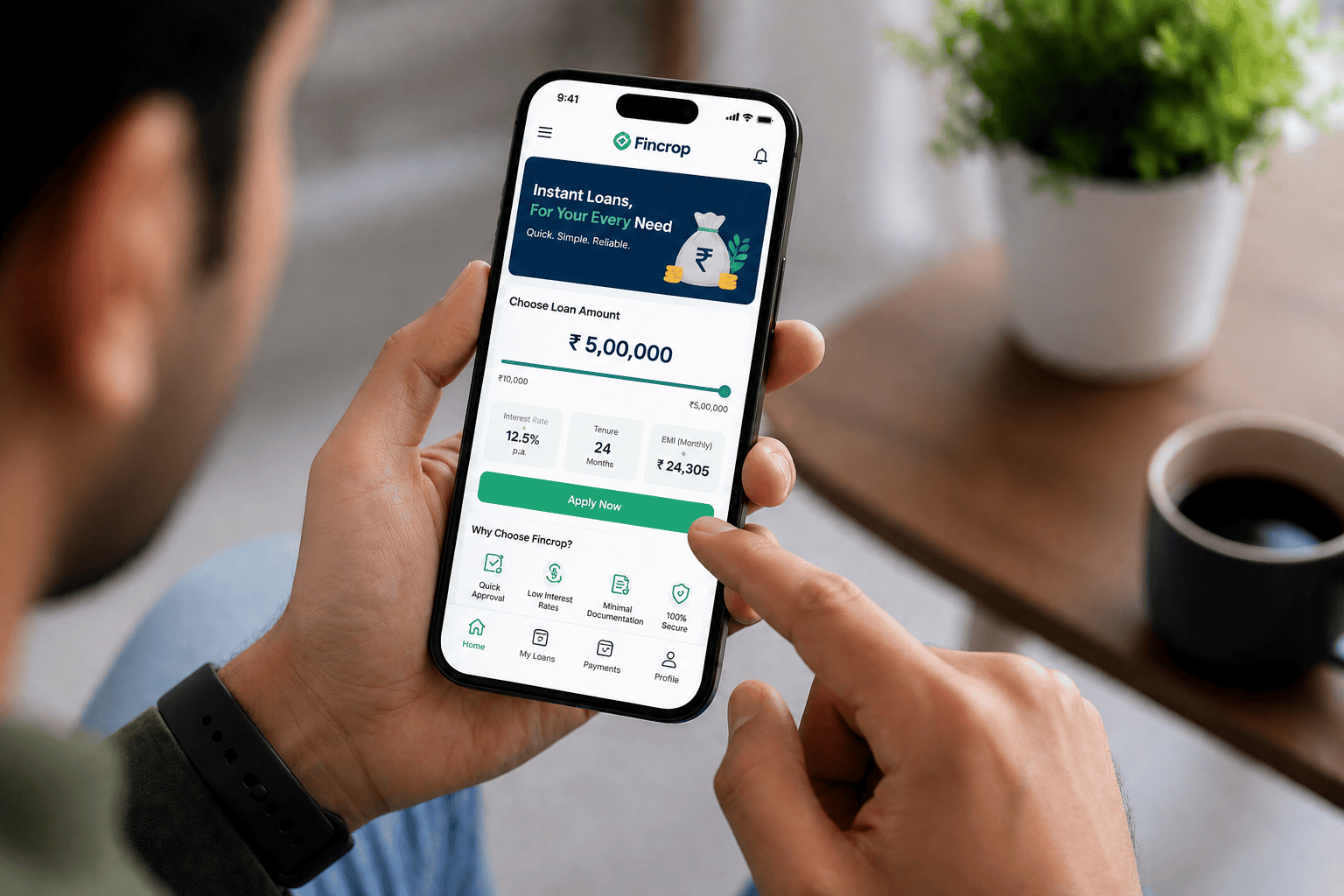

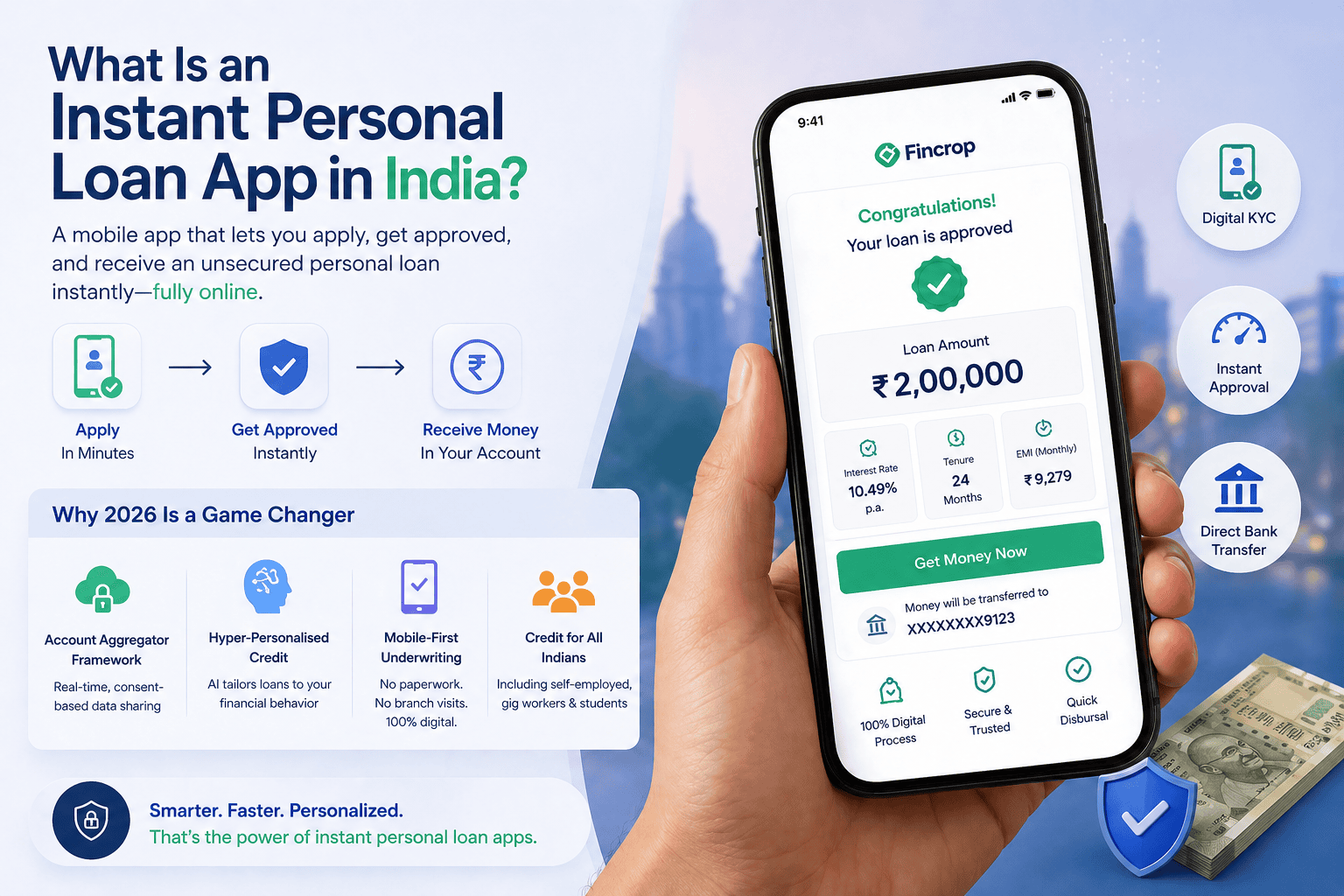

What Is an Instant Personal Loan App in India?

An instant personal loan app is a mobile application that lets you borrow an unsecured personal loan without visiting a bank or submitting physical documents.

What separates these apps from traditional personal loans is its architecture. Here is what has actually changed in the Indian lending market by 2026:

- Account Aggregator (AA) framework

- Hyper-personalised pricing

- Mobile-first underwriting

The result is a lending ecosystem where a salaried employee in a Tier-2 city has access to the same loan products as someone working in Mumbai or Bengaluru, and disbursements are measured in hours, not weeks.

Also Read: Top 15 Student Loan Apps in India for Instant Cash

Quick Comparison: Top 20 Instant Personal Loan Apps in India (2026)

The table below compares the top 20 apps across loan amount, tenure, interest rate, and key differentiators. Detailed write-ups for each app follow the table.

| App Name | Interest Rate | Loan Amount | Tenure | Key Feature / USP |

| Hero Digital Lending & UPI App | Starting 1.50%/mo | Up to Rs 5 Lakh | 12-36 months | RBI-registered NBFC; 100% digital; same-day disbursal |

| Navi | 9.9%+ p.a. | Up to Rs 20 Lakh | 3-84 months | Video-KYC; no collateral; large loan amounts |

| Bajaj Finserv | 11% p.a. onwards | Up to Rs 40 Lakh | 12-96 months | Flexi Loan; pre-approved offers; zero foreclosure charges |

| MoneyTap | 13%-24% p.a. | Rs 3,000-5 Lakh | 2-36 months | Pay interest only on amount used; RBL Bank backed |

| KreditBee | 12%-29.95% p.a. | Rs 1,000-5 Lakh | 3-24 months | 10-minute approvals; salary advance option |

| NIRA Finance | 24%-36% p.a. | Up to Rs 1 Lakh | 3-12 months | Rs 12K monthly income eligible; instant credit line |

| PaySense | 16%-36% p.a. | Rs 5,000-5 Lakh | 3-60 months | Salaried and self-employed; AI underwriting |

| Dhani | 13.99%-35.99% | Up to Rs 15 Lakh | 3-24 months | OPD healthcare bundled; subscription lending model |

| Fibe | 18%-30% p.a. | Rs 5,000-10 Lakh | 3-24 months | Salary advance in minutes; student-friendly |

| LazyPay | 15%-32% p.a. | Rs 10,000-5 Lakh | 3-24 months | BNPL integrated; instant checkout credit |

| mPokket | 2%-4%/month | Rs 500-30,000 | 61-120 days | Students and first-time borrowers |

| Slice | 10.5% p.a. onwards | Rs 2,000-10 Lakh | 3-36 months | Prepaid card with EMI and cashback rewards |

| SmartCoin (Olyv) | 20%-30% p.a. | Rs 4,000-5 Lakh | 3-12 months | Low CIBIL score accepted; gig worker focused |

| CASHe | 27%-36% p.a. | Rs 7,000-4 Lakh | 3-18 months | Proprietary Social Loan Quotient (SLQ) scoring |

| Pocketly | 3%-5%/month | Rs 1,000-50,000 | 10-90 days | College students; UPI-linked repayment |

| Stashfin | 11.99%-59.99% | Rs 1,000-5 Lakh | 3-36 months | Credit line with Visa/Mastercard physical card |

| Rufilo | 24%-36% p.a. | Rs 5,000-2 Lakh | 3-12 months | New-To-Credit (NTC) borrowers |

| Zype | 18%-42% p.a. | Rs 1,000-5 Lakh | 3-24 months | Account Aggregator framework; instant verification |

| Finnable | 16%-28% p.a. | Rs 50,000-10 Lakh | 6-48 months | 15-minute approval; dedicated loan manager |

| IndiaLends | 10.75% p.a. onwards | Rs 15,000-50 Lakh | 12-60 months | Marketplace: matches to 70+ lenders in one application |

Note: Data sourced from respective app listings, official websites, and public NBFC disclosures. Rates are indicative and subject to borrower profile.

Detailed App Reviews

The following write-ups cover each app in detail, including who it is best suited for, how the process works, and what to watch out for before applying.

1. Hero Digital Lending & UPI App

If you want a personal loan from a lender you can actually verify on the RBI website, Hero FinCorp is a strong starting point. The company has been in the consumer lending business for years and built its digital product specifically to cut out the branch visit. The app handles KYC, credit assessment, and agreement signing without a single paper form.

USP: 100% paperless processing by an RBI-registered NBFC with same-day disbursal

Best For: Salaried professionals and self-employed individuals looking for a regulated, fully digital lender with transparent pricing

2. Navi

Navi came to the lending market with serious capital and a clear goal: make large personal loans accessible through a phone. The loan ceiling of Rs 20 Lakh is unusually high for an app-first product, and the video-KYC process means you never need to step out to complete identity verification.

USP: Video-KYC enabled, zero collateral, one of the widest loan slabs among app-based lenders

Best For: Salaried professionals who need larger loan amounts and want a long repayment window to keep EMIs low

3. Bajaj Finserv

Bajaj Finserv has been around long enough that most salaried Indians have seen a pre-approved loan offer from them at some point. Through the app, existing customers can check their limit and disburse within minutes. The Flexi Loan feature, where you draw from an approved limit and pay interest only on what you use, is genuinely useful for people whose expenses do not arrive in a single lump sum.

USP: Flexi Loan withdrawal facility with zero foreclosure charges for existing customers

Best For: Existing Bajaj Finserv customers and borrowers who need above Rs 10 Lakh with long tenure flexibility

4. MoneyTap

MoneyTap was one of the first apps in India to bring the revolving credit line concept to retail borrowers. Once approved, you get a limit you can dip into whenever you need money, and you only pay interest on what you actually withdraw. That structure is genuinely different from a standard term loan and works well for people whose cash needs are unpredictable.

USP: Revolving credit line: interest charged only on the drawn amount, not the full approved limit

Best For: Consultants, freelancers, and commission-based professionals with variable monthly cash flow

5. KreditBee

KreditBee built its reputation on speed and has largely earned it. For most salaried applicants with a clean credit history and a valid salary slip, the 10-minute approval claim holds up in practice. The salary advance option covers short-term gaps before payday without requiring a full personal loan application.

USP: Approvals in under 10 minutes for salaried applicants, with a separate salary advance product

Best For: Young salaried professionals who need fast access to small or mid-size loan amounts without lengthy paperwork

6. NIRA Finance

NIRA fills a gap most lenders ignore: the salaried worker earning between Rs 12,000 and Rs 25,000 per month who cannot qualify for a bank personal loan. Rather than a lump-sum disbursement, NIRA gives you a credit line to draw from as needed, which keeps interest costs lower than borrowing the full amount upfront.

USP: Credit line accessible to salaried individuals earning as little as Rs 12,000 per month

Best For: Lower-income salaried workers in Tier-2 and Tier-3 cities who are excluded by traditional bank lending criteria

7. PaySense

Most instant loan apps quietly exclude self-employed applicants or make the process so cumbersome it barely works. PaySense takes a different approach and actively underwrites both salaried and self-employed borrowers. Its AI credit model looks at data points beyond the CIBIL score, which helps approve people newer to formal credit.

USP: Accepts both salaried and self-employed applicants using AI-based credit underwriting

Best For: Self-employed individuals and salaried borrowers with a limited credit history who need flexible tenure options

8. Dhani (Indiabulls)

Dhani is not a conventional loan app. It runs on a subscription model where a fixed monthly fee unlocks a personal loan limit alongside free OPD consultations. For families spending on both credit and healthcare regularly, the bundled proposition can make practical sense, though the subscription cost needs factoring into the total borrowing cost.

USP: Monthly subscription model that bundles personal credit with outpatient healthcare (OPD) benefits

Best For: Borrowers who want to consolidate their credit and basic healthcare costs into a single monthly payment

9. Fibe (EarlySalary)

Fibe, formerly EarlySalary, built its early user base among young IT and BPO employees who needed a few thousand rupees before the month-end. The rebranding did not change what works: salary advances that reach your account in minutes for verified applicants. The platform has since expanded to larger personal loans and accepts applicants with limited credit history.

USP: Salary advance disbursed within minutes, with an expanding personal loan product for first-time borrowers

Best For: Young salaried professionals and recent graduates applying for their first formal personal loan

10. LazyPay

LazyPay started as a checkout financing tool on platforms like Zomato and Swiggy and has grown into a personal loan product. If you have used LazyPay for purchases, your repayment behaviour on those transactions feeds directly into your personal loan eligibility. The integration with daily spending platforms gives it a behavioural data edge over purely income-based lenders.

USP: Buy-now-pay-later history influences personal loan eligibility; fast approvals for existing users

Best For: Regular users of LazyPay's BNPL service who want to convert their credit limit into a personal loan

11. mPokket

mPokket fills a very specific market gap. Banks will not lend Rs 2,000 to a second-year engineering student without a salary slip. mPokket will, provided the student has a valid college ID and basic KYC. Every repayment is reported to credit bureaus, which gives students a tangible financial head start before they enter the workforce.

USP: Microloans for college students with minimal income documentation

Best For: College students and individuals with no formal income who are entering the credit system for the first time

12. Slice

Slice gives you a prepaid Visa card loaded from an approved credit line, and you repay in flexible EMIs. The cashback on transactions adds real value for regular users. It is popular in metro cities among the 22 to 35 age group, who find traditional credit card applications too slow or rejection rates too high.

USP: Co-branded prepaid card with a credit line and cashback rewards on every transaction

Best For: Urban millennials who want an alternative to traditional credit cards with a faster approval process and in-built rewards

13. SmartCoin

SmartCoin is built around the reality that India's gig economy workers, delivery agents, and contractual employees often have irregular income and thin credit files. The app uses device-level data, utility payments, and employment patterns to build a credit profile that goes beyond a CIBIL number.

USP: Alternative credit scoring for gig workers and borrowers with low or no CIBIL score

Best For: Gig economy workers, delivery executives, and contractual employees with irregular income and limited formal credit history

14. CASHe

CASHe built its own credit scoring system, the Social Loan Quotient, which considers LinkedIn profile strength, professional history, and social credibility alongside standard credit bureau data. The idea is to give a more complete picture of a salaried borrower's creditworthiness than the CIBIL score alone can provide.

USP: The Proprietary Social Loan Quotient (SLQ) model uses professional network data alongside the credit bureau score

Best For: Young salaried professionals with limited credit history but strong, verifiable employment in established organisations

15. Pocketly

Pocketly is a narrow product with a clear audience: college students across India who need small amounts for a few weeks. The loan range and short repayment window are deliberately aligned with how students actually manage money. UPI integration for both disbursal and repayment makes the process frictionless for its digital-native user base.

USP: Short-term microloans built specifically for college students with UPI-based disbursal and repayment

Best For: College students who need small amounts for short periods and want to start building a credit history before graduation

16. Stashfin

Stashfin stands out because the credit line it approves comes with a physical card, not just an in-app wallet. You can use your approved limit at any POS terminal, online store, or ATM, similar to a credit card. Once you repay a portion of the drawn amount, the credit line refreshes for future use.

USP: Revolving credit line paired with a physical Visa or Mastercard usable at any merchant or ATM

Best For: Borrowers who want the flexibility of a credit card alongside the structure of a personal loan, without the full credit card application process

17. Rufilo

Rufilo's entire business model is built around one specific borrower: someone who has never borrowed from a bank or NBFC and has no CIBIL score. Rather than treating this as a disqualifier, Rufilo uses employment verification, income data, and mobile usage patterns to assess creditworthiness from scratch.

USP: Dedicated lender for New-To-Credit (NTC) borrowers with zero CIBIL score history

Best For: First-time borrowers who have never taken a formal loan and need a starting point to build their credit profile

18. Zype

Zype is one of a small number of loan apps actively using the RBI's Account Aggregator framework, which lets borrowers share verified bank data with a single tap and their own consent. This eliminates manual bank statement uploads entirely. Income verification happens in real time, which is why Zype can process applications significantly faster than apps still relying on physical document review.

USP: Account Aggregator framework integration for real-time, consent-based income verification without manual uploads

Best For: Tech-savvy borrowers who are comfortable with the AA data-sharing framework and want one of the fastest processing experiences available

19. Finnable

Finnable positions itself slightly above the micro-loan segment by setting a minimum loan amount of Rs 50,000. That tells you its target borrower: a salaried professional who needs a meaningful amount and prefers some hand-holding through the process. The 15-minute approval claim is backed by automated underwriting that checks employer stability, income, and existing debt.

USP: 15-minute approval with a dedicated loan manager assigned post-approval for queries and repayment support

Best For: Salaried professionals who need Rs 50,000 or more and prefer a lender that offers human support alongside a digital process

20. IndiaLends

IndiaLends does not lend from its own books. You fill out one application, and it goes simultaneously to over 70 banks and NBFCs. You then receive multiple offers and choose the best rate and terms for your profile. That competitive dynamic is why starting rates of 10.75% per annum are possible: lenders are competing for your business rather than quoting a take-it-or-leave-it rate.

USP: Single application submitted to 70-plus lenders simultaneously; borrower chooses the best offer received

Best For: Borrowers who have been rejected by one lender or want to compare the full market without damaging their credit score through multiple applications

How to Choose the Best Loan App for You

The number of loan apps in India makes comparison feel overwhelming. Most of them show you a low rate on the homepage and bury the processing fee and GST in the fine print.

Before you apply anywhere, work through these eight factors:

| Factor | What to Check | Why It Matters |

|---|---|---|

| Interest Rate | Flat vs reducing balance; compare the APR | Determines your actual total repayment cost |

| Loan Amount | Minimum and maximum on offer | Borrow only what you need, not the ceiling |

| Tenure Range | Short-term vs long-term options available | Directly affects your monthly EMI amount |

| Processing Fee | Upfront or deducted from the disbursal amount | Reduces the net cash you actually receive |

| Repayment Mode | Auto-debit, UPI, NEFT support | Affects how convenient monthly payments are |

| RBI Registration | NBFC or bank licence status | Legal protection if a dispute arises |

| App Reviews | Play Store and App Store ratings and comments | Real borrower experiences, not brand claims |

| Prepayment Terms | Nil charge or percentage of outstanding | Matters if you plan to close the loan early |

For most borrowers, the right app is the one offered by an RBI-registered entity, charges no hidden fees, and gives you a loan amount and tenure that fits your actual repayment capacity, not the maximum you qualify for.

Choosing the Personal Loan App

The Indian personal loan market in 2026 is genuinely competitive, and that is good news for borrowers.

You can compare lenders in the time it would have taken to fill out a single paper application five years ago. The risk, however, is picking an app based solely on speed, without checking whether the lender is regulated, what the actual APR is, or whether the loan amount fits your repayment budget.

Start with the comparison table, shortlist the best option based on your loan amount and income type, and check the KFS before you accept any offer.

Apply with Hero FinCorp, get an instant personal loan of up to Rs 5 Lakh with 100% paperless processing, starting at 1.50% per month. Download the Hero FinCorp Android app and check your eligibility in minutes.

Frequently Asked Questions

Which is the best instant personal loan app in India for low interest?

Hero FinCorp starts at 1.50% per month, which is among the lowest rates in the NBFC segment.

How much time does it take for the fastest instant loan app to disburse money?

With Hero FinCorp, approved loans can be disbursed on the same day after KYC verification.

Can I get a loan from an instant personal loan app with a low CIBIL score?

Yes, a score below 650 will typically attract a higher interest rate. Building your score through timely repayments improves your options over time.

Is it safe to share PAN and Aadhaar on the best instant loan app?

Yes, make sure the apps are lending partners are registered with the RBI.

What is the maximum loan amount I can get through an instant loan app?

Hero FinCorp offers up to Rs 5 Lakh with a fully paperless process, which suits most personal loan needs.

Are there any hidden charges in instant personal loan apps?

RBI-registered lenders are required to disclose all fees in a Key Fact Statement before disbursal. Watch for processing fees (typically 1% to 3%), GST, and prepayment charges. Always read the loan agreement before accepting.

Can self-employed individuals apply for the best personal loan app?

Yes. Hero FinCorp accepts self-employed applicants subject to income proof and KYC documents. GST returns, bank statements, or ITR filings are typically accepted as proof of income for self-employed borrowers.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

People in India, including those who reside outside of large cities, are finding it easier to obtain financial assistance. The best personal loans in rural areas can help borrowers handle budgeted spending, crises, education fees, or business demands without relying solely on traditional sources of credit, thanks to digital lending.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.