What is an Overdue Loan? Meaning, Causes, and How to Avoid It

- What is an Overdue Loan?

- Understanding Overdue Amount in Personal Loan

- Overdue in Personal Loan: Key Differences

- When Does a Loan Become Overdue?

- Common Reasons for Loan Overdue Payment

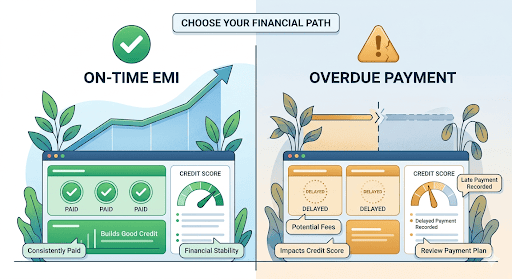

- Consequences of an Overdue Loan

- How to Prevent Loan Overdue Payment

- What to Do If Your Loan is Overdue

- Conclusion

- Frequently Asked Questions

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

What is an Overdue Loan?

An overdue loan is a loan where the borrower has not paid the required EMI or repayment amount by the scheduled due date. If your payment deadline has passed and the amount is still unpaid, the repayment becomes overdue.

For anyone searching what is overdue loan, it is important to know that a missed payment does not mean the loan disappears or gets cancelled. Instead, the unpaid amount remains pending until it is cleared as per the lender’s repayment terms.

Understanding Overdue Amount in Personal Loan

The overdue amount in loan refers to the total payment that remains unpaid after the due date. This may include the missed EMI amount along with applicable charges or additional interest, depending on the loan agreement.

Check your loan statement regularly to stay aware of any pending dues.

Overdue in Personal Loan: Key Differences

Many borrowers confuse a delayed payment with a long-term default. However, these situations can differ.

A regular EMI is paid within the agreed timeline. An overdue payment happens when the due date has passed, but the EMI remains unpaid.

When Does a Loan Become Overdue?

A loan generally becomes overdue when the repayment due date has passed without receiving the required payment. The exact timeline and treatment may depend on the lender’s policies and the terms agreed upon during borrowing.

Common Reasons for Loan Overdue Payment

An overdue loan can happen due to several practical reasons, including:

Financial Emergency or Hardship

Unexpected situations such as medical expenses, family emergencies, or sudden income changes can affect a person’s ability to make timely repayments.

Poor Financial Planning

Managing multiple expenses at once can sometimes make it difficult to keep track of upcoming EMIs. A clear monthly budget can help avoid repayment gaps.

Forgotten Payments

Busy schedules can sometimes lead to missed reminders. You can set alerts and also use available payment reminders to reduce the chances of missing a due date.

Changes in Payment Terms and/or Dates

Changes in repayment schedules or misunderstanding payment dates may result in delays.

Banking or Technical Issues

Failed transactions, account-related issues, technical problems, etc., may also delay payments.

Consequences of an Overdue Loan

Ignoring an overdue payment for a longer period can create challenges. Some possible overdue loan consequences include:

Late Fees and Penalty Interest

Depending on the loan terms, delayed payments may attract additional charges. Clearing dues early can help prevent the overdue amount from increasing further.

Credit Score Damage

Payment history plays an important role in credit records. Frequent delays may impact your credit profile and affect future borrowing decisions.

Collection Calls and Legal Action

For prolonged non-payment, lenders may follow their recovery process as per applicable rules. If your loan is overdue, stay in touch with the lender to understand available options.

Higher Interest Rate on Loan

A history of delayed repayments may influence how lenders assess future applications.

Future Borrowing Restrictions

An overdue repayment record may make it harder to access certain credit products in the future.

How to Prevent Loan Overdue Payment

You can take simple steps to avoid overdue loan situations:

- Use your phone or calendar to set up EMI reminders.

- Set aside money for future repayments.

- Examine your monthly spending on a regular basis.

- Track your loan details through digital tools.

- Understand repayment dates and terms before taking a loan.

Managing repayments becomes easier when you have quick access to your loan information through a digital platform.

What to Do If Your Loan is Overdue

If you already have an overdue loan, avoiding the issue usually makes it harder to resolve. Start by checking your pending overdue amount in loan and understanding what needs to be paid.

Some useful steps include:

- Examine your loan statement.

- Speak with your lender about the circumstances.

- Understand repayment options available.

- Make payments according to the agreed plan.

Conclusion

An overdue loan can put additional strain on finances, but prompt action can ease payments. To prevent overspending and maintain control, always keep an eye on your EMIs and budget your expenditures.

Need quick funds for planned expenses? Check your personal loan eligibility with the Hero FinCorp personal loan eligibility calculator and explore a suitable borrowing option.

Frequently Asked Questions

What is the grace period for an overdue loan?

The policies and loan agreement of the lender determine the grace period for an overdue debt. To understand the relevant deadlines, borrowers should review their repayment arrangements.

If my prior loan is overdue, can I still receive another one?

Repayment history, credit profile, income, and lender eligibility requirements are some of the variables that may affect your ability to obtain a new loan.

What is the duration of an overdue payment on my credit report?

The information provided by lenders and credit bureau procedures determines the reporting period. A better credit history can be developed by making on-time repayments.

Can the lender take legal action on an overdue loan?

In cases of prolonged non-payment, lenders may follow applicable recovery procedures. Contacting the lender early can help borrowers understand the next steps.

How is penalty interest calculated on overdue amounts?

The terms of the loan agreement and the lender determine the penalty costs. For detailed information, borrowers should go over their loan documentation.

Can I settle an overdue loan through negotiation with the lender?

To discuss their circumstances, borrowers might get in touch with their lender. The lender's policies and the borrower's repayment situation determine the available possibilities.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

A cancelled cheque is a common tool used in daily financial and banking processes.

It is required while applying for a loan, starting an SIP, and on several other occasions. It is an ordinary cheque, which is marked so it can’t be used for any payment.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.