Types of Loans in India: A Complete Guide

Loans confuse people. That is fair enough. Walk into a bank or open an app and you will meet a dozen products with names that barely explain themselves: home loan, gold loan, top-up, line of credit, on it goes. Strip away the jargon, though, and nearly every option in India boils down to a handful of types. Learn those few, and the whole decision feels far less daunting.

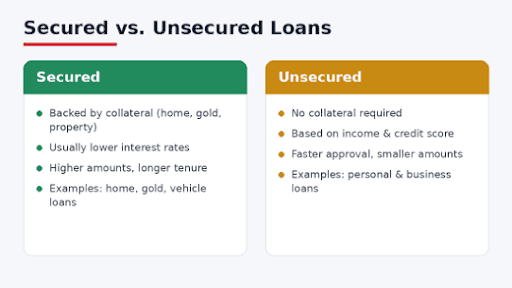

Secured vs. Unsecured Loans: Know the Difference First

One split explains most of it. A secured loan is tied to something you own. Pledge a house, your gold or a car, and the lender has a fallback if you stop paying. That is exactly why these loans tend to be cheaper and let you borrow more.

An unsecured loan flips that. No asset, no pledge. The lender bets on you instead, reading your income, your repayment record and your credit score before deciding. Quicker to get? Usually. Cheaper? Rarely. And since late 2023, when the RBI pushed the risk weight on unsecured consumer credit up to 125%, lenders have grown a lot fussier about who they say yes to.

Common Types of Loans in India

Personal Loan

Personal loan is the all-rounder. Unsecured, flexible, and yours to spend on whatever the moment throws at you: a hospital bill, a wedding, a leaking roof, or clearing a pricey credit card balance. Nobody asks you to justify the spend. The money tends to land fast too, and you can check your personal loan eligibility instantly online before you commit to anything.

Home Loan

Big purchase, long haul. A home loan pays for the flat, the plot or the renovation, with the property itself acting as security. It is the heavyweight of India's retail credit, runs for as long as 30 years, and carries tax breaks on both the interest and the principal under the Income Tax Act. For most families, it is the largest loan they will ever sign for.

Business Loan

A business loan does the heavy lifting when you need to restock, buy a machine or open a second outlet. Some are secured, some are not, and which one you get hangs on how much you want and how healthy your books look. Plenty of owners now skip the paperwork queue and run the whole thing from a Business Loan App, start to finish.

Gold Loan

Got gold sitting idle in a locker? Put it to work. A gold loan hands you cash against your jewellery or coins. It is secured, and it is fast, often sorted the same afternoon. Little surprise, then, that RBI figures showed gold lending climbing sharply through 2024. When cash is needed in a hurry and selling is off the table, this is where a lot of people turn.

Vehicle Loan

Buying a two-wheeler or a car? The vehicle doubles as the collateral, which keeps the rate lower than on unsecured borrowing. You repay it in equal monthly instalments across whatever term you pick.

Education Loan

Studying at home or heading abroad? An education loan covers tuition, living costs and the bits in between. Most come with a moratorium, so repayment waits until your course wraps up or you find a job, whichever your lender allows.

Loan Against Property and Securities

Already own assets? You can borrow against them without letting go. A loan against property leans on your real estate, while a loan against securities uses your shares or mutual funds. Either route unlocks a sizeable sum at a sensible rate, and you keep what you pledged.

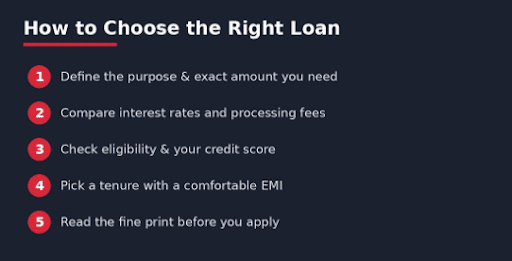

How to Choose the Right Loan for You

Start simple. What is the money for, and how much do you genuinely need? Then look past the headline rate to the processing fee and the tenure. Stretch the tenure and your monthly EMI shrinks, but the total interest you pay climbs, so there is always a trade-off. Run the figures through a personal loan EMI calculator first, and take a quick look at your credit score before you apply. Five minutes here saves a lot of second-guessing later.

Final Thoughts

There is no single best loan. There is only the one that fits your goal, your wallet and your timeline. Get the secured-versus-unsecured idea straight, match the type to the need, and you are the one calling the shots.

Need funds without the runaround? Apply for a Hero FinCorp personal loan and see your eligibility in minutes, with quick disbursal when it counts. Prefer to do it from your phone? Grab the Instant Loan App on Android or the Hero Digital Lending & UPI App on iOS.

Frequently Asked Questions

Which loan is the cheapest?

Usually a secured one. Home and gold loans charge less because the lender is holding something of yours as backup.

Do I need collateral for a personal loan?

No. It is unsecured, so it comes down to your income, your credit score and how well you have repaid in the past.

Does my credit score really matter?

For unsecured loans, a great deal. A strong score gets you approved faster and often at a friendlier rate.

Can I borrow entirely online?

Yes. With a fully digital lender you apply, finish your KYC and get the funds without setting foot in a branch, sometimes the very same day.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Imagine you’re taking out a personal loan for your dream wedding or an unexpected medical bill, and you’re bombarded by smallprint for pages and pages. What if there was a one-page easy to read summary document that told you everything that matters in plain language?

Loan defaults don’t all happen for the same reason. Sometimes repayments stop because income drops or a business struggles. In other cases, borrowers continue to have the means to pay but choose not to. RBI treats these two situations very differently.

'Wilful defaulter' is used only for deliberate non-payment, and the classification tends to persist for some time.

Freelancing and gig work are booming in India. In fact, the number has reached over 7.7 million according to NITI Aayog. 21. And that number is set to reach 23.5 million by 2030.