What is LTV Ratio?

- LTV Full Form in Banking

- How the LTV Ratio Works

- LTV Ratio Formula

- Importance of LTV Ratio in Home Loans

- RBI Guidelines on LTV Ratio

- Advantages and Disadvantages of LTV Ratio

- How LTV Influences Loan Interest and Tenure

- How to Improve Your LTV Ratio

- Variations in LTV Ratio Rules

- LTV vs Combined Loan to Value or CLTV

- Mortgage Example of LTV

- The Bottom Line

- LTV FAQs

Priya applied for a loan to purchase a house in Lucknow for ₹50 lakh. The bank, after assessing the property and Priya’s financial condition, agrees to provide a loan of ₹35 lakh, while Priya has to arrange the remaining ₹15 lakh as a down payment.

The decision of the bank is taken based on the LTV ratio.

The Loan to Value ratio, or the LTV ratio, is the proportion of the total property value that the bank is willing to provide as a loan. It helps lenders calculate risk while deciding loan eligibility.

LTV Full Form in Banking

The LTV full form in banking is Loan to Value.

The LTV meaning stands for a financial indicator that is used by banks to compare the amount of the loan and the value of the asset that is being financed, i.e., a property.

Banks and NBFCs use the ratio of LTV to determine:

- Loan amount

- Borrower’s eligibility

- Down payment to be made by the borrower.

- Risk associated with the loan.

Low LTV means that risk is also low; similarly, high LTV means that a larger amount of the asset is being financed by the borrower.

How the LTV Ratio Works

The role of the Loan to Value ratio is quite important when considering the structuring of the loan.

The lender compares the loan amount and the value of the property. If the value of the property is high and the borrower is making a bigger down payment, the LTV ratio is low, and approval chances are high.

LTV ratio also influences:

- Loan approval

- Interest rates

- Down payment requirement

- Loan tenure options

A borrower can get better loan terms if he makes a larger down payment.

If you are looking for financing options, check your eligibility through Hero FinCorp’s instant personal loan portal.

LTV Ratio Formula

The LTV ratio formula is - LTV Ratio = (Loan Amount ÷ Property Value) × 100

Example

| Value of Property (INR) | Loan Amount (INR) | LTV Ratio |

|---|---|---|

| 50,00,000 | 35,00,000 | 70% |

In this case, 70% of the property value is given as a loan, while 30% is given as a down payment by the borrower.

This formula helps lenders balance lending risk and borrower contribution.

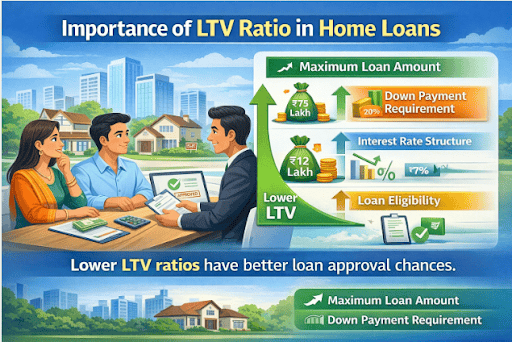

Importance of LTV Ratio in Home Loans

LTV ratio becomes important in the following ways when applying for a home loan:

- Maximum loan amount - Lenders determine how much they can finance based on the property’s value.

- Down payment requirement - A lower LTV means a higher borrower contribution.

- Interest rate structure - Loans with lower LTV ratios may attract comparatively favourable interest terms.

- Loan eligibility - Lower LTV ratios have better loan approval chances.

RBI Guidelines on LTV Ratio

RBI regulates LTV limits for housing loans to reduce risk and ensure responsible lending. Here are some guidelines:

| Value of Property (INR) | Maximum LTV |

|---|---|

| Up to 30 lakhs | Up to 90% |

| 30 lakhs - 75 lakhs | Up to 80% |

| Above 75 lakhs | Up to 75% |

Lenders can also apply stricter limits based on the borrower’s credit profile, type of property, etc.

Advantages and Disadvantages of LTV Ratio

| Advantages of LTV Ratio | Disadvantages of LTV Ratio |

|---|---|

| Helps lenders estimate risks | High LTV could mean higher interest |

| Encourages responsible borrowing | Borrowers need to make down payments |

| Determines loan size | Property value fluctuations may influence risk assessment |

| Improves financial discipline through down payments | LTV alone cannot consider credit behaviour |

How LTV Influences Loan Interest and Tenure

The LTV ratio can influence the overall cost of borrowing:

- A lower LTV ratio means lower risk for lenders

- A higher LTV ratio means a higher risk

- Loans with higher LTV ratios may have different interest structures or stricter lending terms.

- LTV can also influence loan tenure options. Borrowers making larger down payments can get flexible repayment periods.

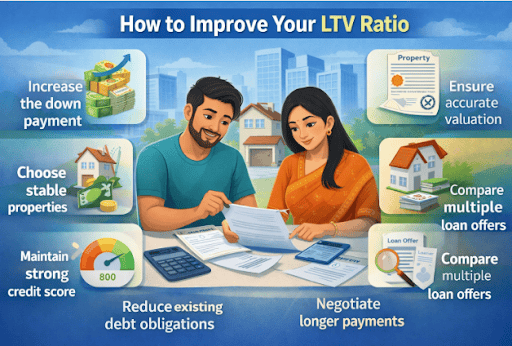

How to Improve Your LTV Ratio

Borrowers can take several steps to improve the LTV ratio when applying for a loan.

- Increase the down payment amount

- Choose properties with stable market valuations

- Maintain a strong credit score

- Reduce existing debt obligations

- Negotiate a longer payment period.

- Ensure property valuation documents are accurate

- Compare multiple loan offers before applying

You can also manage loan applications conveniently using the Hero Digital Lending App, available on Android and iOS.

Variations in LTV Ratio Rules

Different loan products may follow different LTV structures based on risk levels and regulatory norms. These values also depend on the lender’s internal policies and borrower profile.

| Loan Type | LTV Limit |

|---|---|

| Home Loans | Up to 75-90%, depending on property value |

| Loan Against Property | Around 50-70% |

| Plot Loans | Around 50-70% |

| Construction Loans | Around 70-80% |

LTV vs Combined Loan to Value or CLTV

| Feature | LTV | CLTV |

|---|---|---|

| Definition | Loan compared to property value | All loans compared to the property value |

| Loans considered | Primary mortgage only | Includes secondary loans |

| Risk evaluation | Basic risk indicator | More comprehensive risk measure |

| Usage | Standard loan approvals | Complex financing situations |

While LTV focuses on the primary loan, CLTV considers multiple loans secured against the same property.

Mortgage Example of LTV

Here is a simple scenario showing how a down payment affects the LTV ratio.

| Property Price (INR) | Down Payment (INR) | Loan Amount (INR) | LTV Ratio |

|---|---|---|---|

| 50 lakhs | 10 lakhs | 40 lakhs | 80% |

| 50 lakhs | 15 lakhs | 35 lakhs | 70% |

| 50 lakhs | 20 lakhs | 30 lakhs | 60% |

The Bottom Line

Understanding LTV ratio is essential when applying for a home loan/property-based finance option.

When borrowers make a higher down payment, the LTV ratio is reduced, which means they can increase the chances of getting a loan and reduce the borrowing risk.

If you want to finance your future expenses or financial goals, check your eligibility instantly through Hero FinCorp’s personal loans section.

LTV FAQs

What is the Loan to Value ratio in banking?

The LTV ratio is the percentage of the value of the property that is financed through the loan.

How is the LTV ratio calculated for a Home Loan?

The LTV ratio formula is LTV Ratio = (Loan Amount ÷ Property Value) × 100.

Why is the LTV ratio significant for loan approval?

The LTV ratio helps the lender assess the risk and check loan eligibility.

What is a good LTV ratio?

The lower the LTV ratio, the better.

What is the maximum LTV permitted by RBI?

RBI permits 90% of the loan amount as LTV ratio for small property loans.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.