Difference Between Term Loan and Working Capital Loan

Pick the wrong loan for your business need and you pay for it, literally, for years.

A term loan and a working capital loan are both business credit products. That is roughly where the similarity ends. One funds what you are building. The other keeps operations from stalling while you build it. Getting the term loan vs working capital loan decision right from the start saves money, reduces repayment pressure, and keeps your credit profile clean.

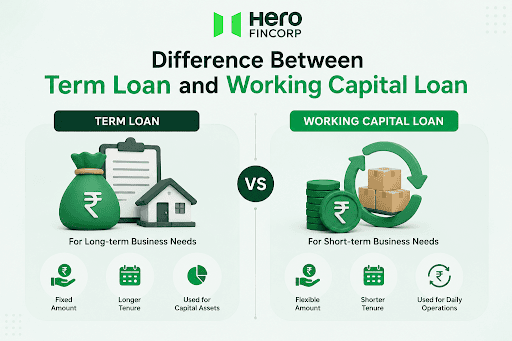

What is a Term Loan?

A term loan is borrowed once, for a defined purpose, repaid over a fixed schedule.

Businesses use it for things that stick around: factory equipment, commercial vehicles, office property, technology infrastructure. The full amount is disbursed upfront. Repayment runs in structured EMIs across an agreed tenure, usually one to ten years.

Because the repayment schedule is predictable, lenders price term loans lower than most other business credit products.

Key features:

- Fixed EMIs beginning shortly after disbursal

- Tenure of 1 to 10 years, depending on purpose and lender

- Higher loan amounts linked to the asset or project being funded

- Secured or unsecured based on loan size and borrower profile

- Lower interest rates relative to short-tenure products

Term loan vs working capital in one line: term loans fund assets. Not operational gaps.

Also Read: Business Loan vs Personal Loan: Which Is Best for Entrepreneurs?

What is a Working Capital Loan?

Supplier invoice due Friday. Client payment arriving in 45 days. Salaries going out Monday.

That gap, the one that exists in almost every business regardless of how well it is doing, is what a working capital loan addresses.

It is a short-tenure product built for operational continuity. Inventory purchase, utility bills, payroll in a slow collection month, rent when receivables are delayed. The term loan vs working capital loan split here is simple: term loans build the business, working capital loans keep it moving.

Key features:

- Short tenure, typically 6 months to 3 years

- Faster processing, particularly through digital lenders

- Flexible repayment on overdraft and credit line structures

- Higher interest rates than term loans given shorter tenure and unsecured nature of many products

- No end-use restriction on most working capital products

Also Read: What is the Structure of GST in India?

Term Loan vs Working Capital Loan: Comprehensive Comparison

| Factor | Term Loan | Working Capital Loan |

| Purpose | Capital expenditure, long-term assets | Operations, cash flow management |

| Tenure | 1 to 10 years | 6 months to 3 years |

| Repayment | Fixed monthly EMIs | Flexible, product-dependent |

| Loan Amount | Higher | Turnover-linked |

| Interest Rate | Lower | Higher |

| Collateral | Required for larger amounts | Both secured and unsecured options |

| Approval Speed | Slower, detailed assessment | Faster, digital-first options available |

| Best Used For | Equipment, property, expansion | Salaries, inventory, supplier payments |

| Disbursement | One-time, upfront | Lump sum or revolving credit line |

The difference between term loan and working capital goes well beyond tenure.

A term loan lives inside an asset. The machinery, the property, the vehicle it funded keeps generating value across the repayment period. A working capital loan moves through the business cycle, recovered through sales and collections, closed out once the operational gap resolves.

Funding a two-month cash flow gap through a five-year term loan means paying interest long after the problem closed. Funding a three-year asset purchase through a six-month working capital product creates repayment pressure before the asset generates a single rupee in return. The difference between term loan and working capital is not just structural. It is financial common sense.

Also Read: Working Capital Management: Meaning, Types & Objectives Explained

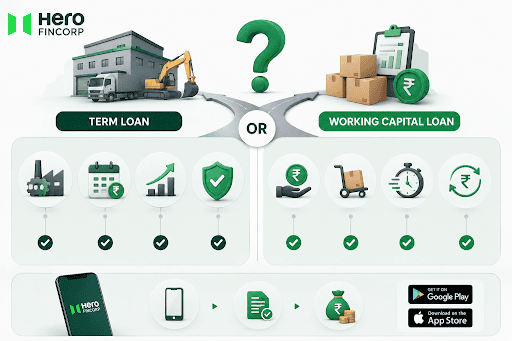

How to Choose: Term Loan or Working Capital Loan?

One question worth asking before anything else: will this money still be working inside the business three years from now?

If yes, a term loan fits. If it solves something that closes within weeks or a few months, working capital is the right call.

A term loan works better when:

- The fund requirement is for equipment, property, or vehicles with multi-year utility

- Fixed monthly repayments are manageable within current cash flow

- The goal is expansion or capacity addition, not operational survival

- Collateral is available, which brings down rate and improves eligibility

A working capital loan works better when:

- Business revenue is consistent but collections are delayed and expenses cannot wait

- Inventory or raw materials need purchasing ahead of the next payment cycle

- Speed of disbursal is more critical than the length of the repayment window

- Repayment flexibility tied to actual receivable cycles is preferable to fixed EMIs

Apply for a Hero FinCorp loan and get funds structured around your actual business requirement. The entire process can be managed from your phone via the Hero Digital Lending & UPI App, available on Google Play and the App Store.

Frequently Asked Questions

Can term loans be used for working capital needs?

You could. But here is the problem. Say your client payment got delayed by 60 days. You take a term loan to cover salaries and supplier dues in the meantime. The client pays. The gap closes. But your EMIs keep coming for the next three years on money you needed for two months. Working capital products exist precisely for this. They close when the need closes. Term loans do not.

What are the average interest rates for term loans vs working capital loans in India?

No fixed number applies universally here. That said, most term loans for businesses in India fall somewhere between 10 and 18% annually. Working capital facilities tend to run between 12 and 24%. Why the difference? Shorter tenure, less predictable repayment, and frequently no collateral. Lenders price all three of those into the rate. Your actual number shifts depending on how long the business has been running, what your credit score looks like, annual turnover, and whether anything is being pledged.

What is the difference between secured and unsecured working capital loans?

Secured means something is pledged. Property, stock, outstanding receivables. The lender has a fallback, so the rate comes down and the sanctioned limit goes up. Unsecured means the approval rests on your financials and credit history alone. Nothing is pledged, nothing is at seizure risk, but the interest rate reflects that the lender is carrying the full exposure. Faster to process, more expensive to service.

Are demand loans and working capital loans the same?

Not the same, though the terms get mixed up often. A demand loan gives the lender the right to recall the entire outstanding balance at short notice, no fixed repayment schedule involved. Certain working capital facilities, overdrafts being the most common, are structured this way. But not every working capital loan works on demand terms. Some have fixed tenures and standard repayment schedules. The facility document is the only place that tells you which one you are actually signing.

How does collateral affect the approval of term loans and working capital loans?

Three things change when collateral is on the table: approval likelihood goes up, sanctioned amount increases, interest rate drops. Without it, the lender works only from credit score and business financials. That shrinks what they are willing to offer and raises what they charge for it. On larger term loans particularly, most lenders will not sanction without some form of security. The asset being funded sometimes serves as the collateral itself, as with vehicle or equipment loans.

Can startups avail term loans or working capital loans?

Most banks and larger NBFCs want a minimum of 2 to 3 years of operating history before they will engage seriously. Audited financials, ITR filings, GST returns. Without these, the application rarely gets far. Earlier stage businesses have a few genuine options though. MUDRA loans under Pradhan Mantri MUDRA Yojana go up to Rs. 10 lakh without collateral. SIDBI runs schemes specifically for small and early-stage enterprises. Some NBFCs have built products around newer businesses with thinner documentation. One thing that consistently matters at this stage regardless of which route is taken: the promoter's personal CIBIL score.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Taking a personal loan is the easy part. Managing the EMIs, month after month, is where the real work begins.

You look at your bank balance in the middle of the month. You think about where your salary went. This happens to a lot of people. The 50/30/20 budget rule is a way to stop feeling bad about how you spend your salary.

Every month, a slice of your salary vanishes into something called “PF”. It’s easy to treat it as just another deduction, but that deduction is quietly building your retirement corpus, tax-free. Understanding PF in salary, such as what it means, how it’s calculated, and when you can withdraw it, helps put you in charge of your long-term financial health. Let’s decode it without the jargon.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.