What Is The 50-30-20 Rule Of Budgeting?

It's the 1st of the month, the day you have anxiously been waiting for: the salary credit. Excitement peaks, you first pay off all your bills, indulge in a bit of retail therapy, and finally check out that new restaurant or cafe that's in the news.

Come the 15th, your bank balance is looking dangerously low. You're back to coffee and Maggie at home instead of dining out and deferring purchases till the next salary credit. Sound familiar?

If yes, it's most likely due to chaotic spending habits. Now, if you want to break this vicious cycle, one method you can use is the 50-30-20 rule for budgeting.

What Is the 50-30-20 Rule?

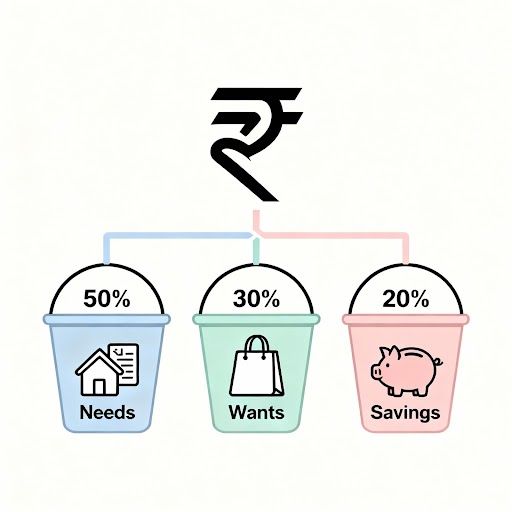

The 50-30-20 rule is a simple budgeting method in which you split your salary (what you get post taxes) into three simple buckets -

- 50% for needs

- 30% for wants

- 20% for savings

This rule was popularised in the book All Your Worth: The Ultimate Lifetime Money Plan, by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi. Its purpose was to make budgeting easy for everyone who is not an accountant.

This method works extremely well with Indians, particularly because it aligns with how we naturally categorise expenses. We already think in terms of "zaroorat" (needs), "shauk" (wants), and "bachana" (saving). The 50-30-20 rule just puts percentages to these instinctive categories.

How to Save Money From Salary Using the 50-30-20 Rule?

The process to save money with the 50-30-20 rule is simple. You start with your in-hand salary, that is, the exact amount that gets credited into your bank account.

Assume your in-hand salary is ₹50,000. Now,

- 50% for your needs equals ₹25,000

- 30% for your wants equals ₹15,000

- 20% for savings and investments equals ₹10,000

What Counts As a Need?

Every expense that is vital to your everyday living and well-being comes under the needs category. These include your rent/home loan payments, your utility bills, groceries, medical costs, insurance premiums, and travel and clothing expenses for work.

If you have kids, school fees, clothing needs, tuition fees, and expenses toward their extracurricular activities, also go into this bucket.

What Counts As a Want?

Any spending toward something that you "want" but is not vital to your survival falls under this category. These can include your impulse retail purchases, that latest gadget, OTT subscriptions, eating out at restaurants, and travel, to name a few.

The biggest advantage of the 50-30-20 rule is that it doesn't curtail your wants. You still get to do whatever you want to do (it's your hard-earned money after all), but within a fixed spending limit.

What Counts As a Saving?

Any money that you put towards your financial safety and security counts as savings. This should include an emergency fund, Systematic Investment Plans (SIPs), investments in Public Provident Fund (PPF), and in Fixed Deposits(FDs) or Recurring Deposits (RDs).

Personal Loan is Smarter Than Using Your Savings

This should include an emergency fund, Systematic Investment Plans (SIPs), investments in Public Provident Fund (PPF), and in Fixed Deposits(FDs) or Recurring Deposits (RDs).

Advantages of the 50 30 20 Rule for Indian Households

The 50-30-20 rule works great for Indian households due to the following reasons -

- It's deceivingly simple to implement.

- It addresses your critical expenses, allocates money for your financial security, and sets aside a fixed amount for guilt-free spending.

- This formula can easily scale with your income.

- Most importantly, it will save you from the stress and anxiety of not being in control of your expenses.

Bringing Balance Back to Your Money

The 50-30-20 rule is not a get-rich-quick scheme. It is a means to bring structure to your spending so that you don't end up wondering where all your money went by the middle of the month. That said, this rule is not for everyone and is not set in stone.

If your salary is not too high, these percentages may not work for you. If you live in a city with a high cost of living 50% may not be enough for your needs. If you are earning well, saving/investing only 20% of your income will not be able to sustain your lifestyle later on.

Alter the percentages to best fit your circumstances, but once you do, stick to the budget like your life depends on it.

If you need funds for a financial emergency, apply for a personal loan at Hero FinCorp. The process is paperless, the terms are transparent, and you can get an approval in minutes.

Frequently Asked Questions

Can the 50-30-20 rule work with irregular income?

It depends on how irregular the income is. If there is a slight variation, then yes. If the income varies drastically, recalculate the percentages every month.

How strict should I be with the percentages?

Ideally, the stricter you are, the better your budget will hold up. Being realistic, a 5% variation here and there between the needs and wants categories is okay.

What if my needs exceed 50% of my salary?

If your needs exceed 50%, adjust percentages to say 60-20-20. Such a scenario is common in cities with a high cost of living, specifically in terms of rent.

Should debt repayment be counted as needs?

Yes, all EMI payments go into needs (50%). You cannot compromise on this, as every delayed or missed payment can rack up additional charges and interest, which will throw your entire budget off balance.

How do families use this rule?

As a family with multiple incomes, calculate the total household income and then apply percentages accordingly.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.