Structure of GST in India: Types, Components and Tax Framework Explained

- What Is the Structure of GST in India?

- Why India Adopted a Unified GST System

- Overview of the Dual GST Model in India

- Components of GST in India

- Difference Between CGST, SGST, IGST and UTGST

- GST Tax Slabs and Rate Structure in India

- How GST Is Applied on Intra-State and Inter-State Transactions

- Input Tax Credit (ITC) and Its Role in GST Structure

- Role of GST Council in Managing GST Structure

- Benefits of the GST Structure in India

- Challenges and Limitations of the GST Structure

- Recent Developments and Future of GST Structure in India

- Conclusion

- Frequently Asked Questions

Walk into any shop, hire any service, move any goods across a state border, and GST is already in the transaction.

Over 1.5 crore businesses actively file under the system, and collections crossed Rs. 22 lakh crore in FY 2024-25.

Despite that scale, the GST structure in India still trips people up, particularly when CGST, SGST, and IGST appear on the same invoice with no explanation of why.

Here is how it all fits together

What Is the Structure of GST in India?

The structure of GST is a destination-based indirect tax: every point in the supply chain collects it, but only the final consumer actually pays.

An invoice-linked credit system handles the difference at each stage.

Explaining the structure of GST in India comes down to two questions on any transaction: which of the four components applies, and at what rate. Where the goods go and what they are determine both answers.

Why India Adopted a Unified GST System

GST replaced 17 major taxes and 13 cesses that were in place simultaneously before 2017.

A business selling across states dealt with central excise at dispatch, state VAT at the destination, and entry taxes at every border crossing in between. GST collapsed that entire structure.

Key Objectives of GST

- Kill cascading tax through an invoice-linked credit mechanism

- Tear down state-level entry barriers fragmenting the national market

- Pull informal transactions into a traceable, document-based framework

Overview of the Dual GST Model in India

India's GST structure gives neither the Centre nor the states exclusive collection authority. Both are collected simultaneously on the same transaction, which is what makes it a dual model.

How the Dual GST Model Works

On intra-state sales, two taxes apply at once: one Centre, one state, both on the same transaction value.

In interstate sales, a single integrated tax replaces both, and the Centre shares the destination state's cut after collection.

Role of Central and State Governments

GST is destination-based, so consuming states receive the revenue rather than producing states. The Centre runs CGST and IGST.

Each state runs its own SGST. Rate changes need Council consensus, not unilateral action by either side.

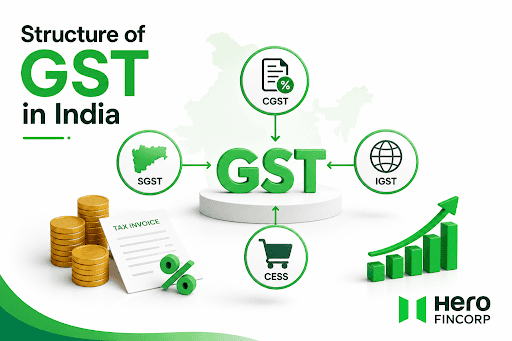

Components of GST in India

Four components make up the GST structure in India, each covering a specific transaction type.

CGST (Central Goods and Services Tax)

Whenever a sale occurs within a single state, the Central Government collects its share through CGST.

A printer supplier in Pune selling to a Pune-based firm pays CGST on that invoice. The money goes to the Centre, not the state.

SGST (State Goods and Services Tax)

The state collects SGST on that same transaction, at the same rate. Both CGST and SGST are recorded on a single invoice, calculated on the same value, but deposited into completely separate accounts. Maharashtra keeps its SGST.

The Centre keeps its CGST. Neither touches the other's share.

IGST (Integrated Goods and Services Tax)

Once goods or a service cross a state border, CGST and SGST drop off the invoice entirely. IGST replaces both, collected by the Centre at the combined rate.

A Pune supplier invoicing a Hyderabad buyer charges IGST only. The Centre later credits Telangana's portion through its settlement process.

UTGST (Union Territory Goods and Services Tax)

Territories like Chandigarh and Lakshadweep have no state government to collect SGST. UTGST fills that gap, same rate, same logic, just administered by the Centre on the territory's behalf instead.

Difference Between CGST, SGST, IGST and UTGST

| Component | Who Collects | Transaction Type | Revenue Destination |

| CGST | Central Government | Intra-state | Centre |

| SGST | State Government | Intra-state | State |

| IGST | Central Government | Inter-state, imports | Center then shared |

| UTGST | Centre for UT | Intra-UT | Union Territory |

GST Tax Slabs and Rate Structure in India

At the 56th GST Council meeting in September 2025, India overhauled its rate structure under GST 2.0. Four slabs became two. Here is what each category covers.

Nil-Rated and Exempt Supplies

Fresh vegetables, milk, eggs, education, and healthcare. These either attract no GST or fall entirely outside the tax net.

5% GST Slab

The merit rate. Daily essentials, agricultural goods, and healthcare equipment sit here to keep consumer costs down.

12% GST Slab

GST 2.0 eliminated this slab entirely. Items previously here have been shifted to either 5% or 18% based on classification.

18% GST Slab

The standard rate. Financial services, IT, telecom, restaurants, and most consumer goods fall under 18%.

28% GST Slab and Compensation Cess

A 40% rate now replaces the 28% slab for premium vehicles, tobacco, and aerated beverages. The compensation cess winds down as state transition guarantees expire.

Also Read: What is CGST & SGST? Key Differences Between Them

How GST Is Applied on Intra-State and Inter-State Transactions

One question drives everything about GST structure in practice: does the supply stay within one state or cross a border?

Intra-State Supply (CGST + SGST)

Both CGST and SGST apply equally. A Rs. 10,000 sale in Mumbai at 18% GST results in Rs. 900 CGST being paid to the Centre and Rs. 900 SGST to Maharashtra.

Inter-State Supply (IGST)

Only IGST appears on the invoice. The Centre collects everything, then credits the destination state's portion through settlement.

Real-Life GST Transaction Example

A Surat fabric trader sells Rs. 50,000 of material to a Bengaluru manufacturer at 5%. The Centre collects IGST of Rs. 2,500 and credits Karnataka's share.

Had the buyer been in Surat, CGST and SGST of Rs. 1,250 each would have applied instead.

Input Tax Credit (ITC) and Its Role in GST Structure

Remove ITC from the GST structure, and the whole system becomes a turnover tax, taxing prices that already carry embedded tax from the previous stage.

What Is Input Tax Credit?

When a business pays GST on purchases, that amount becomes a credit. The business offsets it against the GST it collects on sales and only deposits the difference.

How ITC Prevents Cascading Taxation

A manufacturer pays 18% GST on raw materials. Without ITC, that tax is embedded in the product price. The next buyer pays 18% again on a price that already carries the first 18%. ITC removes that overlap entirely.

Benefits of ITC for Businesses

- Cuts net tax deposits for businesses with high input costs

- Pushes buyers toward GST-registered suppliers, widening the formal economy

- Reduces monthly cash pressure by lowering what actually leaves the account

Check your Hero FinCorp personal loan eligibility here if working capital gaps are putting pressure on operations.

Also Read: Working Capital Loan: Meaning, Eligibility and 2026 Application Guide

Role of GST Council in Managing GST Structure

The GST Council makes every significant call on the GST structure in India: rates, exemptions, thresholds, and compliance rules.

Composition of GST Council

The Union Finance Minister chairs it. Every state Finance Minister sits as a member. States hold two-thirds of the voting weight; the Centre holds one-third.

Functions and Responsibilities

- Sets rate slabs and decides what falls inside or outside the GST net

- Reviews thresholds, compliance rules, and filing requirements

- Has met over 56 times since 2017, with September 2025 delivering the biggest rate overhaul since launch

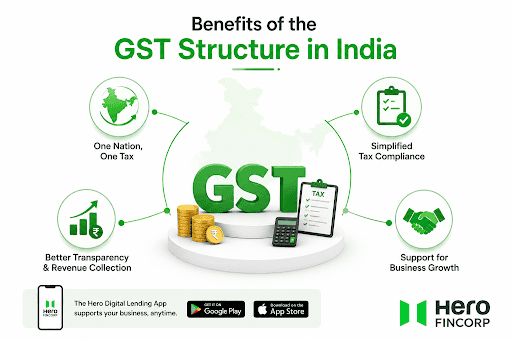

Benefits of the GST Structure in India

One Nation, One Tax

GST cut logistics costs across India by over 33% by removing state border checkpoints and the documentation burden that goods trucks faced at every crossing.

Simplified Tax Compliance

One portal replaced parallel VAT, excise, and service tax filings. By June 2025, 1.53 crore taxpayers were actively using the GST network, supported by e-invoicing and e-way bills.

Better Transparency and Revenue Collection

Every ITC claim links to a seller's outward supply declaration, so mismatches are automatically detected. GST collections peaked at Rs. 2.36 lakh crore in April 2025, the highest monthly figure ever recorded.

Support for Business Growth

Exports attract zero GST with ITC refunds on inputs. The Hero Digital Lending & UPI App on Google Play and the App Store supports businesses that need quick funds while meeting GST obligations.

Challenges and Limitations of the GST Structure

Multiple Tax Slabs

Classification disputes between slabs continue to generate litigation and compliance uncertainty, especially for products near category boundaries.

Compliance Burden for Small Businesses

Small businesses feel GST compliance differently from large ones. The compliance design has not caught up with the reality of who is actually doing the filing.

Frequent Regulatory Updates

Each Council meeting can change rates or compliance rules on short notice. Businesses across multiple product categories incur real, ongoing costs to track and implement every update.

Recent Developments and Future of GST Structure in India

GST Rationalisation Efforts

The August 2025 reform announcement focused on three areas: structural reform, rate rationalisation, and ease of doing business. Removing the 12% and 28% slabs and introducing the 40% demerit rate was the biggest single change to the GST structure in India since 2017.

Future Reforms and Digital Tax Administration

The administration is pushing pre-filled returns, AI reconciliation tools, faster refund cycles, and stricter e-invoicing thresholds forward simultaneously.

On the dispute side, the GST Appellate Tribunal finally gives taxpayers somewhere to take a grievance that is not immediately a high court petition, which, for most businesses, was simply not a realistic option cost-wise

Conclusion

GST is not a simple tax, and anyone who tells you otherwise has probably never filed a return or disputed a classification.

The structure of GST in India comprises four components: handling different transaction types, a credit mechanism that prevents tax from stacking at every stage, and a Council that negotiates every rate change through weighted consensus.

GST 2.0 trimmed the slabs. Digital tools are chipping away at the paperwork. It is still not perfect, but understanding how the pieces connect makes navigating it considerably less painful.

Frequently Asked Questions

What is the structure of GST in India?

The structure of GST in India is a dual indirect tax system where the Centre and states both collect on the same intra-state transaction simultaneously.

What are the four components of GST?

CGST is what the Centre collects on intra-state supplies. SGST is what the state collects on those same transactions. IGST is what the Centre collects on inter-state sales and imports before sharing the destination state's cut. UTGST mirrors SGST but covers union territories that lack their own legislature.

How does CGST differ from SGST?

Both apply to the same intra-state transaction at identical rates. The difference is where the money lands. CGST revenue accrues to the Centre; SGST accrues to the state. On an 18% invoice, the 9% CGST and 9% SGST appear as separate line items but the buyer pays both at the point of sale.

When is IGST applicable?

IGST applies to imports and interstate transactions. Whenever a supplier and a buyer sit in different states, IGST is the only GST on that invoice. The Centre collects everything and then credits the consuming state's portion through the settlement process.

What is the dual GST model in India?

The dual GST model gives both the Centre and the states the authority to levy and collect GST on the same supply at the same time. Within a state, CGST and SGST both appear. Across state lines, only IGST applies, and the Centre redistributes accordingly.

What are the GST tax slabs in India?

GST 2.0 set the two main slabs at 5% for essential goods and 18% for most goods and services. A 40% rate now covers luxury and sin goods, replacing the old 28% slab and compensation cess arrangement.

Why is the Input Tax Credit important in the GST structure?

ITC stops tax from compounding at every stage of the supply chain. Without it, each buyer pays GST on a price that already carries GST paid upstream, which is what the old regime produced. With ITC, each business deducts the amount it paid for inputs from the amount it collects on outputs. Only the net value added at each stage is taxed, keeping the actual burden on the final consumer rather than invisibly building through every production step.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.