What Is UPI 2.0? Features, Benefits

UPI 2.0 was officially launched by NPCI (National Payments Corporation of India) on August 16, 2018. This new version was equipped with numerous additional features to enhance the country's financial inclusivity.

In this post, we'll discuss UPI 2.0 in more detail, covering its features, a comparison with UPI 1.0, the future of UPI 2.0, and more. Read on!

UPI 2.0: A Quick Brief

UPI 2.0 is an advanced, upgraded version of the Unified Payments Interface (UPI 1.0). The version followed a significant evolution of UPI 1.0, introducing a range of new features, such as enhanced security and greater transaction flexibility.

UPI 2.0 is set to play a key role in shaping India's digital payment landscape by enhancing overall security, facilitating financial inclusion, and integrating advanced features such as virtual credit lines.

Also Read: How to Create Your UPI Number Using a Mobile Banking App

Top Features of UPI 2.0 Explained

Here are some of the key UPI 2.0 features:

- One-Time Mandate Payments: One of the key features of UPI 2.0 is a one-time mandate facility with pre-authorisation of transactions. It is ideal for cases where a commitment to a money transfer is made in advance.

- Signed Intent & QR for Security: Enhances security by verifying merchants' legitimacy via QR codes. This speeds up transactions and eliminates the need for a password for signed intent.

- Overdraft Linking: UPI 2.0 enables easy overdraft linking for instant transactions.

- Invoice in Collect Requests: UPI 2.0 allows the merchants to attach an invoice directly to a collect request. This means users can verify their bills before paying, thereby minimising the risk of incorrect or fraudulent requests.

- Enhanced Transaction Sharing: Another interesting feature of UPI 2 lets users securely share transaction details with merchants or service providers for after-sales support.

UPI 1.0 vs UPI 2.0 – A Detailed Comparison

Here's a detailed comparison of UPI 1 vs. UPI 2 differences:

| Features | UPI 1.0 | UPI 2.0 |

| Key Use | The primary focus of UPI 1 is on basic Person-2-Person (P2P) money transfers. | UPI 2 supports both Person-2-Person (P2P) and enhanced person-to-merchant (P2M) transfers. |

| Overdraft Facility | It is not available in UPI 1 | UPI 2 allows users to link their overdraft accounts for transactions. |

| One-Time Mandate | Not available in UPI 1 | UPI 2.0 enables pre-authorised, scheduled payments. |

| The invoice in the Inbox | Not available | Merchants can send digital invoices with payment requests, allowing users to verify details before paying. |

| Security | Basic security with UPI PIN | Enhanced security via Signed Intent & QR codes, which verify the merchant's authenticity and protect against fraud. |

| UPI Transaction Limit | Up to ₹1 lakh per transaction/day. | ₹1 lakh daily limit is maintained. Also allows higher-value transactions (e.g., up to ₹2 lakh) for specific features. |

On this note, if you ever find yourself short on funds, the Hero FinCorp's Instant Loan App can help you access quick, hassle-free personal loans right when you need them. Download it now!

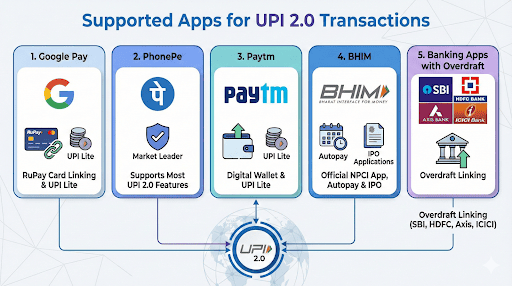

Supported Apps for UPI 2.0 Transactions

Major UPI applications such as PhonePe, Google Pay, and the government's BHIM app all support UPI 2.0 features.

Here are details of some of the major apps (and banks) in India that support UPI 2.0:

1. Google Pay

Google Pay is primarily known for reliability and a simple user interface. The app supports credit card linking (for RuPay cards) and UPI Lite as well.

2. PhonePe

PhonePe is the market leader in UPI payments and supports most UPI 2.0 features.

3. Paytm

Paytm integrates UPI payments with a digital wallet and e-commerce services, offering various features like QR code payments and UPI Lite.

4. BHIM

BHIM is the official government-backed app from the NPCI that supports UPI Autopay (mandates) and IPO applications using a UPI ID.

5. Banking Apps Supporting Overdraft Linking

There are several banks that support UPI 2.0’s overdraft linking, including State Bank of India (SBI), HDFC Bank, Axis Bank, and ICICI Bank.

Also Read: How UPI Is Redefining Instant Loan Repayments in India

Transaction Limits, Caps, and Charges for UPI 2.0

As compared to UPI 1, the UPI 2.0 transaction limit has been raised for specific categories, with a ₹5 lakh per-transaction limit and a ₹10 lakh daily cap for P2M payments such as insurance, capital markets, government payments, and travel.

Further, daily caps continue to vary across banks, typically ranging between ₹1–2 lakh for most users, though some banks impose caps on the number of daily transactions (usually 10–20).

With UPI 2.0 features such as UPI mandates and invoice validation, banks may apply separate internal limits for automated or recurring payments.

Future Outlook: How UPI 2.0 Shapes India’s Digital Ecosystem

UPI 2.0 comes packed with various new features that can fast-track India’s digital transformation in the coming years.

The new UPI system is set to make instant loan disbursements and repayments much easier and faster by seamlessly integrating with lending platforms. Plus, UPI 2.0 also boasts features that support invoice financing.

This can provide small businesses with easy access to working capital for day-to-day operations. With more innovations in UPI 2.0, such as interoperable digital solutions and improved authentication measures, the system is poised to bolster India’s digital economy and drive greater financial inclusion for everyone.

If you're facing issues with your UPI app or dealing with a temporary financial shortfall, Hero FinCorp’s personal loan app can help you bridge the gap with quick, convenient access to funds.

So why wait? Explore our Hero FinCorp Instant Loan App today and get access to quick, secure, and hassle-free personal loans whenever you need them!

Frequently Asked Question

What distinguishes UPI 2.0 from UPI 1.0?

Improved security, overdraft protection, one-time mandates, and invoice-in-box are features that set UPI 2.0 apart from UPI 1.0.

Which apps support UPI 2.0?

All major UPI applications, including those offered by banks, such as BHIM, Google Pay, PhonePe, and Paytm, support the features introduced in UPI 2.0.

What is the maximum transaction limit in UPI 2.0?

The maximum daily transaction limit is ₹ 1 lakh.

How do mandates work?

Mandates work by allowing users to pre-authorise payments for future transactions.

Are there any charges for UPI 2.0 transactions?

No, UPI 2.0 transactions do not incur any charges.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.