What is Loan Underwriting?

A loan application may feel simple on the surface. The information is provided, and the income details are submitted; the application proceeds to the next stage. The next step is the loan underwriting process, in which lenders assess the likelihood of granting the loan and the terms under which it will be granted.

Loan underwriting enables lenders to assess risk and determine the interest rate to be charged and the loan amount to be granted.

Loan Underwriting Meaning

Loan underwriting is the process by which lenders determine whether a borrower can repay a loan. Financial information, including income, credit score, outstanding debts, and repayment behaviour, is examined in this phase.

This process is used for most types of loans, including personal, home, and business loans. Good financial records tend to ease the underwriting process, whereas higher-risk areas might attract more rigorous terms or greater scrutiny.

Also Read: CIBIL Score Range: Know Whether Your CIBIL Score is Good or Bad

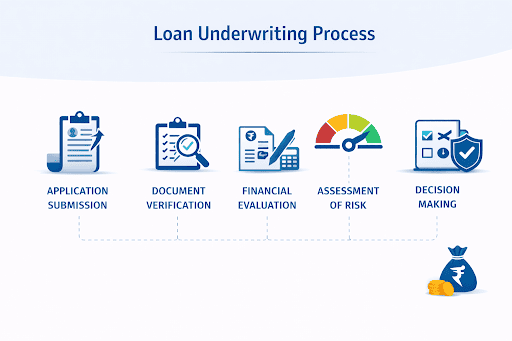

How Does Loan Underwriting Work?

Generally, several steps are involved in the loan underwriting process:

- Application submission

It starts with loan applications that require basic details of income, employment, and identification documents.

- Document verification

The lender reviews documents such as bank statements, salary slips, tax returns, and business records as evidence of financial details.

- Financial evaluation

An evaluation of income stability, monthly obligations, and repayment capacity is conducted to determine whether the loan can be serviced comfortably.

- Risk Assessment

Credit score, existing debts, and financial history are evaluated to assess the risk of approving the loan.

- Decision making

Once the evaluation is complete, the loan may be approved, declined, or subject to certain conditions, such as a lower loan amount.

- Loan disbursal

Once the underwriting stage is complete, the approved funds are disbursed in accordance with the loan agreement.

Types Of Loan Underwriting

Given below are the types of loan underwriting:

- Manual underwriting

In manual underwriting, a human underwriter evaluates financial documents and credit history in detail. This approach allows flexibility but may take longer.

- Automated underwriting

Automated systems use algorithms to analyse financial data quickly. This method speeds up approval decisions but relies heavily on predefined criteria.

- Hybrid underwriting

Many lenders combine automated analysis with human review. This approach balances speed with deeper evaluation of complex financial profiles.

Importance Of Underwriting To Borrowers

Loan underwriting is valuable not only to lenders but also to borrowers. Knowledge of the process helps develop better applications and prevent unwarranted delays.

Underwriting is easier when records are clear, credit history is stable, and approvals can be processed more quickly. It also helps borrowers understand why some loan terms are set, such as tenure limits or interest rates.

When considering loan options, getting eligibility information early can help avoid surprises during underwriting. The overall eligibility check through Hero FinCorp’s official journey can help one understand the loans one can qualify for before making any application.

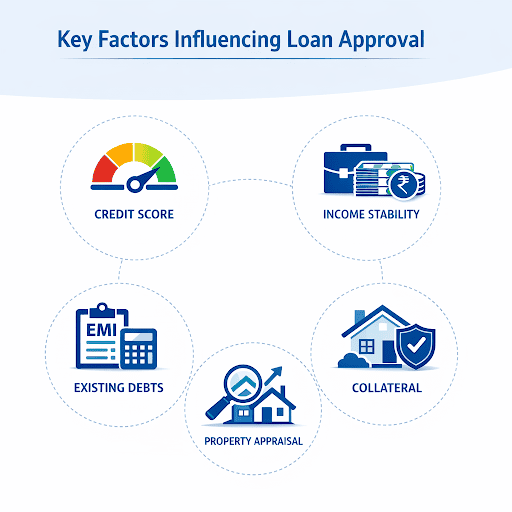

Factors Affecting Loan Underwriting

- Credit score

A higher credit score involves a responsible borrowing behaviour, which minimises perceived lending risk. For instance, a score of more than 750 could lead to faster approvals and lower interest rates, whereas more stringent conditions or additional checks could be imposed in the opposite scenario.

- Income stability

Consistent income will give lenders confidence in repayment. For instance, a person with a fixed monthly income is likely to be considered at a lower risk than one with unpredictable or variable earnings.

- Existing debts

Higher existing loan obligations can reduce the ability to manage additional repayments. If a large portion of income is already going towards EMIs, lenders may limit the new loan amount or adjust the terms.

- Collateral value

For secured loans, the value and quality of the pledged asset directly affect risk evaluation. A well-valued and easily saleable asset increases confidence in repayment security.

- Property appraisal

In property-backed loans, lenders would first evaluate property prices and market conditions.

Also Read: Debt-to-Income Ratio Meaning and Formula

Tips To Make The Underwriting Process Faster

- Keep documents organised The verification delays can be minimised by providing complete and accurate paperwork.

- Maintain income records Regular income documentation helps clearly demonstrate repayment capacity.

- Improve credit score Paying current EMIs and credit card payments on time improves the financial profile.

- Reduce outstanding debts Less debt will increase the probability of approval and more favourable loan terms.

- Respond quickly to lender queries Prompt responses during verification prevent unnecessary processing delays.

Conclusion

Loan underwriting is a process in which a lender determines not only whether a loan can be sanctioned, but also the terms under which it can be sanctioned. Understanding loan underwriting helps with better preparation, avoiding delays, and increasing the scope of approvals.

Frequently Asked Questions

1. What is loan underwriting?

The process by which lenders assess a borrower's financial profile and determine whether to approve a loan is known as loan underwriting.

2. Does underwriting apply to instant loans?

Yes. Even instant loans use automated underwriting systems that can quickly evaluate risk based on financial data.

3. What is the time required for underwriting?

Automated systems can speed up evaluations; manual scrutiny might take longer. However, it depends on the lender and the loan type.

4. What documents must be provided for underwriting?

Identity proof, income records, bank statements, tax returns, and collateral details are the usual ones needed for secured loans.

5. How can someone speed up approval?

The likelihood of getting approval faster depends on a good credit score, stable income, and proper documentation.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.