KYC Guidelines by RBI: Complete Rules, Documents & Process Guide

Know Your Customer (KYC) guidelines issued by the Reserve Bank of India form the basis of secure and compliant financial transactions in India. These rules ensure that banks and financial institutions verify customer identity, prevent fraud, and curb the instances of money laundering.

This guide helps you understand the complete KYC framework, covering key rules, required documents, and the step-by-step process in a simple, practical manner.

What is KYC and an Overview of KYC Guidelines by RBI

KYC is a mandatory process that every financial institution and business must conduct when opening or maintaining accounts for clients.

The Reserve Bank of India has established comprehensive KYC guidelines to strengthen the integrity of India’s financial system.

The key objectives of these RBI KYC rules are to enhance customer due diligence, promote financial inclusion, and ensure a risk-based approach to monitoring transactions.

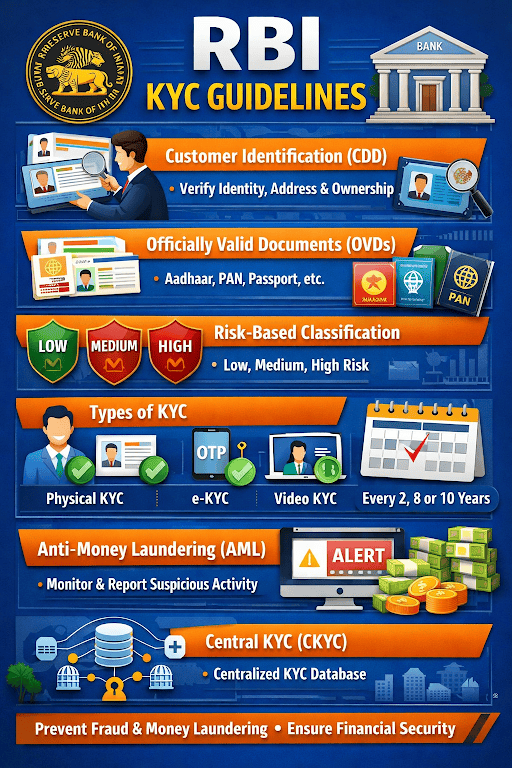

Types of KYC as per RBI

The Reserve Bank of India recognises multiple types of KYC to balance regulatory compliance with customer convenience.

Among these are-

- Physical KYC: This is the traditional method where customers submit physical copies of their identity and complete in-person verification at a branch.

- e-KYC (Aadhaar-based): This is a paperless, instant verification process that uses Aadhaar authentication.

- Video KYC (V-CIP): Video KYC (Video Customer Identification Process) enables live interaction between the customer and the banks for identity verification

e-KYC Process

The eKYC process in India primarily uses Aadhaar-based authentication to verify an individual's identity.

Video KYC (V-CIP)

Video KYC (V-CIP) involves a real-time video interaction between the customer and a bank official. The process includes geo-tagging, timestamping, and secure storage to meet compliance standards.

Documents Required for KYC

As per the Reserve Bank of India, customers must submit officially valid documents (OVDs) to complete KYC compliance. These are-

- Identity Proof (Primary OVDs): Includes

- Aadhaar card

- PAN card (mandatory for financial transactions)

- Passport

- Voter ID

- Driving licence

- Letter issued by the National Population Register

- Address Proof: Most OVDs listed above also serve as address proof if they contain current residential details. If the address differs, customers may provide additional documents such as utility bills, bank statements, or rent agreements.

- Recent RBI Updates: The RBI has enabled simplified KYC processes, including Aadhaar-based e-KYC and Video KYC, reducing reliance on physical paperwork.

RBI KYC Guidelines for Businesses

Under the Reserve Bank of India KYC framework, businesses must comply with structured due diligence norms to prevent fraud, money laundering, and identity misuse.

- Financial institutions are required to verify the business's legal existence.

- As per RBI norms, entities must disclose individuals who ultimately own or control the business.

- Key documents include the entity's PAN, proof of registered office address, and a board resolution or an authorization letter.

KYC Update and Re-KYC Process

As per the Reserve Bank of India, KYC information must be periodically updated to ensure customer records remain accurate and compliant with anti-money laundering norms.

- When is re-KYC required?: Re-KYC is triggered based on the customer’s risk category.

- Methods of updating KYC: Customers can complete the re-KYC process through multiple channels. These include visiting a branch with updated documents, or using Aadhaar-based e-KYC and Video KYC.

- RBI timelines for periodic updates: RBI prescribes different timelines. For instance, low-risk customers must update KYC every 10 years, medium-risk customers every 8 years, and high-risk customers every 2 years.

Latest Updates in RBI KYC Guidelines

Recent updates in KYC norms by the RBI highlight a shift toward digitisation and customer convenience. One key highlight here is the wider adoption of Video KYC.

Apart from this, the latest RBI KYC update also focuses on simplified processes, such as relaxed requirements for low-risk customers and easier periodic updates.

Another major development in India's new KYC rules is the push for digital onboarding. The aim is to encourage paperless verification through Aadhaar-based e-KYC and secure digital platforms.

Also Read: Digital Payment in India: Meaning, Types, & Benefits

Benefits of KYC Compliance

KYC compliance is crucial to the system. Some of the things about KYC compliance include:

- Fraud prevention: KYC compliance helps verify customer identities, reducing instances of financial fraud.

- Faster approvals: Pre-verified customer data speeds up loan approvals and the use of financial services.

- Regulatory trust: KYC helps financial institutions comply with the law, which builds trust with regulators.

- Enhanced security: KYC compliance protects customers' accounts and transactions by verifying their identities.

Conclusion

In summary, the KYC guidelines issued by the RBI provide a framework for verifying customer identity, assessing risk, and ensuring periodic updates. Following the RBI's KYC norms is not necessary for regulatory compliance, but it also helps to keep the financial system safe and secure.

Financial apps like Hero FinCorp personal loan app follow all the RBI norms and offer digital KYC solutions to make it easier for customers to comply with KYC regulations.

Frequently Asked Questions

1. What are the KYC guidelines by the RBI?

These are rules for verifying customers' identities and addresses to help prevent fraud and money laundering.

2. What documents are required for KYC in India?

Common KYC documents include PAN, Aadhaar, passport, voter ID, and other officially valid identity and address proofs.

3. Is KYC mandatory for bank accounts?

Yes, KYC is mandatory for opening and maintaining bank accounts as per RBI regulations.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.