How to Choose Your Financial Lender

Whether it is buying a home, purchasing a car or starting a business, finance is an integral part of the process. Rising consumerism, increasing disposable income and easy availability of credit contribute to the growth.

India has a positive orientation towards loans, and the existence of different types of loans like home loan, auto loan, and business loan prove the point. With so many different financing options to choose from, one would think it’s easy to get a loan. Well...that’s partially true.

How to choose the best lender?

With so many different types of loans and lender finance options, getting a loan is not difficult, but landing a good deal with the right lender is! Getting a loan is not just about the lowest interest rates. There’s more to it. It’s the entire process, from offer to closing, the terms & conditions, and the transparency, which matters. Your financial lender guides you through the entire process, helping you at every step.

You have to exercise proper care, planning and caution while choosing your financial partner. Here are some things you should keep in mind.

- Is your lender offering the right solution specific to your needs?

Every individual or business has distinct requirements. You may require a secured loan while there may be others looking for a more flexible option. That’s where the lender comes in. You lender should suggest the right solution, specific to your requirements. The one-size-fits-all approach is not applicable in finance.

- Research the different loan types

It’s essential that you do a bit of research from your end as well. Learn about the different types of loans available, secured or unsecured, the kind of collateral and documents required, and how interest rates vary etc. This way, you will know if the solution that the lender is offering is actually the best one for you. Compare interest rates, terms etc.. The knowledge will help you negotiate better with your lender.

- Don’t limit your search to a specific type of lender

There are different types of lending finance companies in India, from co-operative credit institutions to financial institutions. Now, fin-tech companies have joined in too. So, research your lenders well. Do not just settle for the first lender that offers the best loan with the lowest rate of interest. Mind you, there’s more to loans than interest rates. The right financial lender will understand your needs and be supportive throughout the loan journey. Customer experience is what matters.

- Assess the cost of loan correctly

When it comes to the cost of loan, interest rate is not the sole criteria for evaluation. Verification charges, processing fees, GST, penalty for late payment, penalty for pre-payment and other miscellaneous charges make up the total cost of the loan. These charges differ from lender to lender. So, make sure to check out all these charges.

- Dig deeper into interest rates

Getting a competitive deal as far as interest rates are concerned isn’t the end of it. You have to decide whether you want a fixed or variable interest rate, what is the total interest you have to pay on the principal amount over the entire tenure, and what are the other charges apart from interest rates (as mentioned above). Get your lender to answer these questions for you.

- Transparency matters

There should be no surprises along the way. The right lender will carefully explain all the terms and conditions, the charges involved, and the total cost of the loan etc. They will be forthcoming about all these aspects and will offer a solution when you get stuck. Also, you should ask the lender about their license and credibility. After all, you want to be sure that you’re working with a reliable and genuine entity.

Conclusion

To conclude, choosing the right financial lender is not always about competitive rates. It’s about asking the right questions and getting the right answers. Taking a loan is an important financial decision, and therefore, you need to apply due diligence and carefully pick the right financial lender who will help you consolidate your debt and achieve the much-needed financial stability.

Related Blogs

Taking a personal loan is the easy part. Managing the EMIs, month after month, is where the real work begins.

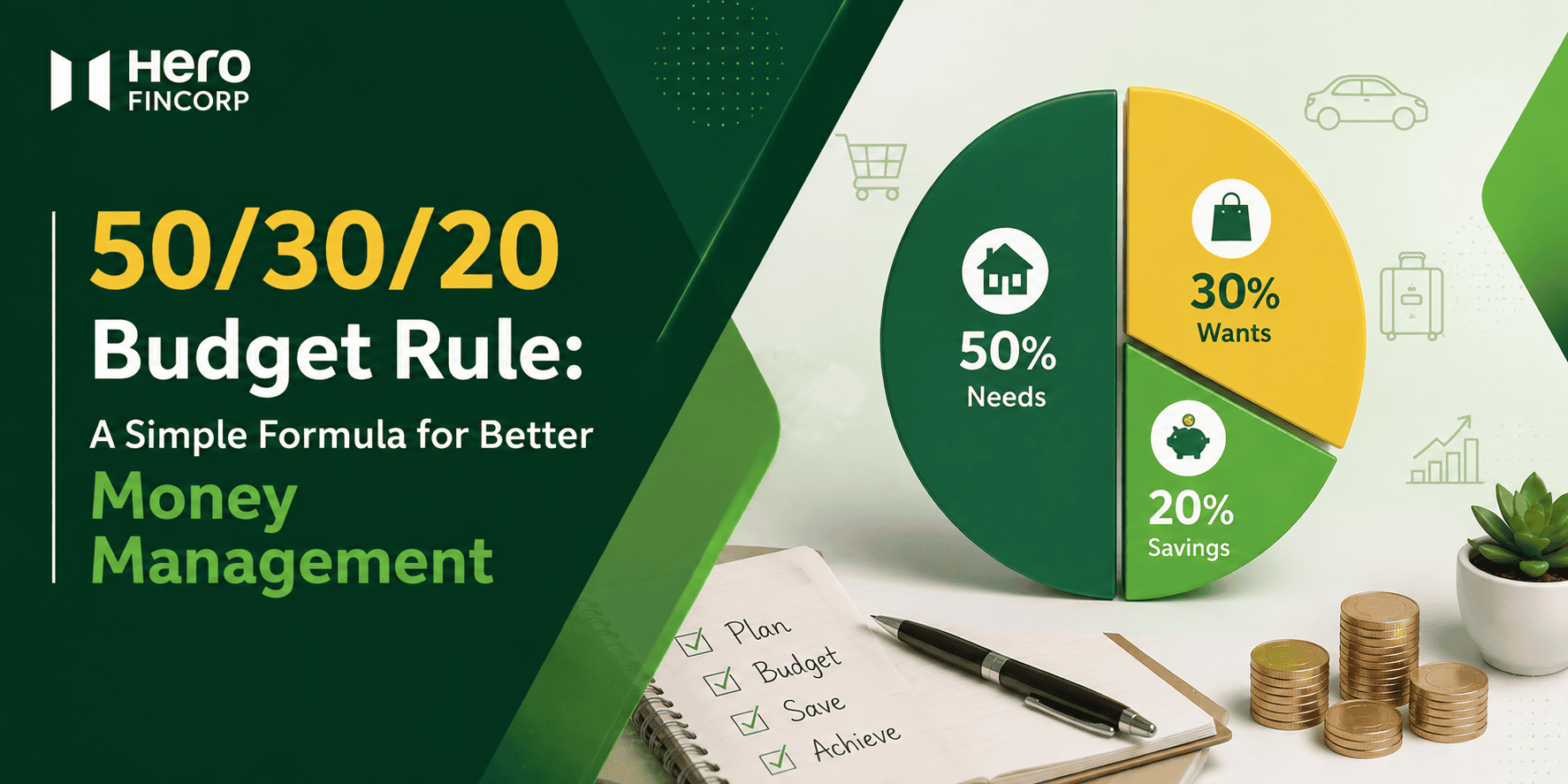

You look at your bank balance in the middle of the month. You think about where your salary went. This happens to a lot of people. The 50/30/20 budget rule is a way to stop feeling bad about how you spend your salary.

Every month, a slice of your salary vanishes into something called “PF”. It’s easy to treat it as just another deduction, but that deduction is quietly building your retirement corpus, tax-free. Understanding PF in salary, such as what it means, how it’s calculated, and when you can withdraw it, helps put you in charge of your long-term financial health. Let’s decode it without the jargon.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.