What is a UPI Payment Gateway and How Does it Work?

- Understanding UPI Payment Gateway

- How a UPI Payment Gateway Works: Step-by-Step Process

- Key Features of a Robust UPI Gateway

- UPI Payment Gateway Charges and MDR in India

- Types of UPI Integrations for Businesses

- Benefits of Using UPI Gateway for E-commerce

- Security Standards in UPI Transactions

- UPI Gateway vs. Traditional Payment Gateways

- How to Choose the Best UPI Payment Gateway for Your Business?

- Future Trends: UPI 2.0 and Beyond

- Why UPI Payment Gateways Matter for Modern Businesses?

- Frequently Asked Questions

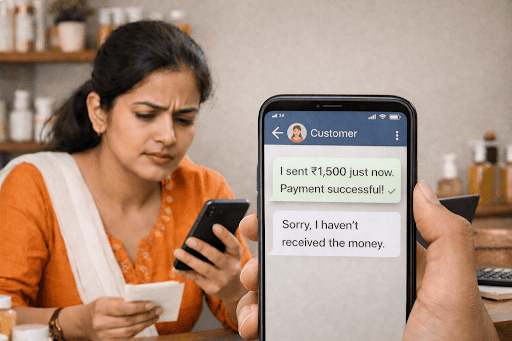

Neha sells homemade beauty products and accepts payment through UPI. When her customers pay through UPI, she receives the money within seconds.

One day, a payment is deducted from the customer's account, but it does not appear in her system. Neha tries to figure out what went wrong, but does not understand how the payment actually moves. This blog explains what a UPI payment gateway is, how it works, and how it manages every payment behind the scenes.

Understanding UPI Payment Gateway

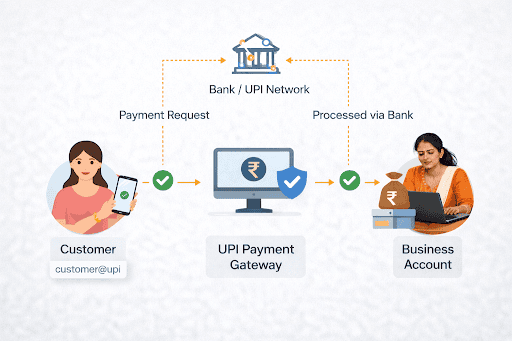

A UPI payment gateway helps a business receive money from customers through UPI. It connects the payer to the business account where the funds need to be deposited.

When a customer makes a payment using a UPI ID, the request goes through the gateway first. The gateway passes it to the bank, then returns the result. Both the customer and the business can see whether the payment went through. This is what keeps the whole process clear and easy to track.

How a UPI Payment Gateway Works: Step-by-Step Process

The UPI payments are instant, but there are a few things that make it work.

Step 1: The customer selects UPI at checkout and either selects an app or enters a VPA.

Step 2: The gateway creates a payment request and sends it to the UPI network

Step 3: The request appears in the customer’s UPI app. They approve it using their UPI PIN

Step 4: The bank checks the details and transfers the money to your account.

Step 5: The gateway sends confirmation back to both sides, almost immediately.

Key Features of a Robust UPI Gateway

Once you start handling regular payments, small details begin to matter a lot more than you expect.

- You can see transactions as they happen instead of waiting for updates

- Fewer payments fail during busy hours, which saves a lot of back and forth

- Integration does not turn into a long technical project

- Customers get options like scanning a QR code or switching apps

- Reports actually make sense when you need to check numbers

These are the things you notice only after you deal with real volume.

UPI Payment Gateway Charges and MDR in India

This is where most business owners lean in a bit more. Costs always matter. Right now, UPI uses a zero-MDR setup for most merchant transactions. You are not paying a cut on every payment that comes in. That is a big reason why adoption grew so quickly.

Some providers do charge for extras. Think better dashboards, faster settlements, or priority support.

A simple way to look at it:

If a customer pays ₹1,000

MDR stays at ₹0

If a service fee applies, say ₹10

You receive ₹990

There is no guesswork if you check this upfront.

Types of UPI Integrations for Businesses

Not every business collects payments the same way. The setup you choose should match how your customer actually pays.

- Intent Flow works well on mobile apps where users switch to their UPI app and come back

- Collect Flow fits websites where people enter a VPA and approve the request later

- Dynamic QR Codes work almost anywhere, especially when you want each payment to stay unique

Benefits of Using UPI Gateway for E-commerce

If you run an online store, you start noticing patterns very quickly.

- Fewer people leave midway through checkout

- Nobody wants to type card details every time

- Payments feel quick, which builds trust without saying much

- Orders move faster because confirmation is instant

It quietly removes friction you did not even realize existed.

Security Standards in UPI Transactions

People trust UPI because it feels simple, but security sits underneath that simplicity. Every payment needs a UPI PIN, which only the account holder knows. Data stays encrypted while it moves through the system.

The entire setup follows rules set by the National Payments Corporation of India and global standards. You do not see these layers, but they are always working.

Also Read: Are UPI PIN and ATM PIN the Same?

UPI Gateway vs. Traditional Payment Gateways

Businesses usually compare the two before deciding how to collect payments. The difference becomes clear when you look at a few basics.

| Factor | UPI Gateway | Traditional Gateway |

| Speed | Payment completes in seconds | Takes longer due to OTP and checks |

| Cost | Usually no MDR | Charges apply to each transaction |

| Process | Few steps, quick approval | More steps with card details |

| Use | Best for daily payments | Supports cards, wallets, and more |

UPI works well when you want quick and low-cost payments. Traditional gateways make more sense when you need more payment options.

How to Choose the Best UPI Payment Gateway for Your Business?

At some point, you stop looking at features and start thinking about reliability.

- How quickly does the money reach your account

- How often do payments fail

- Can you get support when something breaks

- Does integration feel simple or stretched

- Are charges clearly explained

These questions save more trouble than any feature list.

Future Trends: UPI 2.0 and Beyond

UPI is no longer just for sending or receiving money. It is slowly becoming part of how people handle regular payments as well.

Now, users can set up UPI Autopay for subscriptions, bills, or EMIs, so they do not have to approve each payment repeatedly. Another change is the use of credit on UPI, where people can pay using a credit line or card instead of only their bank balance. This provides greater flexibility for users and makes it easier for businesses to manage recurring payments.

Why UPI Payment Gateways Matter for Modern Businesses?

Once you understand how it works, UPI stops feeling like just another payment option. It becomes a part of how your business handles everyday transactions.

A smooth payment experience helps customers complete payments without delays and keeps your orders moving. While payment gateways manage transactions, businesses also need financial support to handle growth and manage expenses.

Hero FinCorp offers personal loans through an instant loan app that helps you access funds quickly and manage your cash flow when needed. Apply here.

Frequently Asked Questions

What is the difference between UPI and a UPI Payment Gateway?

UPI is the payment system. The gateway connects that system to your business.

Are there any hidden UPI payment gateway charges for merchants?

Most payments have zero MDR. Some providers charge for additional services.

Can I accept international payments through a UPI gateway?

UPI mainly supports domestic transactions, though expansion is ongoing.

How long does it take to settle UPI payments into a bank account?

Most payments reflect instantly or within a few hours.

Is it mandatory to have a GST number to use a UPI gateway

Small businesses may start without GST, but growing businesses usually require it.

What is the limit for a single UPI transaction on a merchant gateway?

There is no fixed limit for a single UPI transaction on a merchant gateway. However, many allow up to one lakh rupees per transaction.

How does a dynamic QR code differ from a static QR code in a gateway?

Dynamic QR codes change for every payment, while static QR codes do not.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.