What is CIBIL Score? Meaning, Full Form, Range, and Importance

- What is a CIBIL Score? Meaning and Full Form

- CIBIL Score Range: What Each Bracket Means

- What is a Good CIBIL Score?

- How is CIBIL Score Calculated?

- Key Update: Bi-Monthly Reporting

- Why is CIBIL Score Important?

- CIBIL Score Required for Different Loans

- How to Check Your CIBIL Score Online

- How to Improve Your CIBIL Score

- Factors That Can Hurt Your CIBIL Score

- CIBIL Score vs. CIBIL Report: What is the Difference?

- How Long Does a Low CIBIL Score Last?

- Checking Your Eligibility with Hero FinCorp

- Conclusion

- Frequently Asked Questions

Rahul, a 32-year-old IT professional in Bengaluru, applied for a Personal Loan to renovate his apartment. His salary was strong, his job was stable yet the application was rejected within hours. The reason? A CIBIL score of 620. He had missed two credit card payments eight months ago and assumed it would not matter. It did.

In India, your CIBIL score is often the first thing a lending institution checks before even looking at your income proof. It determines whether you get approved, what interest rate you are offered, and how much you can borrow. Whether you are applying for a Personal Loan, a car loan, or a credit card, your three-digit CIBIL score carries more weight than most people realise.

What is a CIBIL Score? Meaning and Full Form

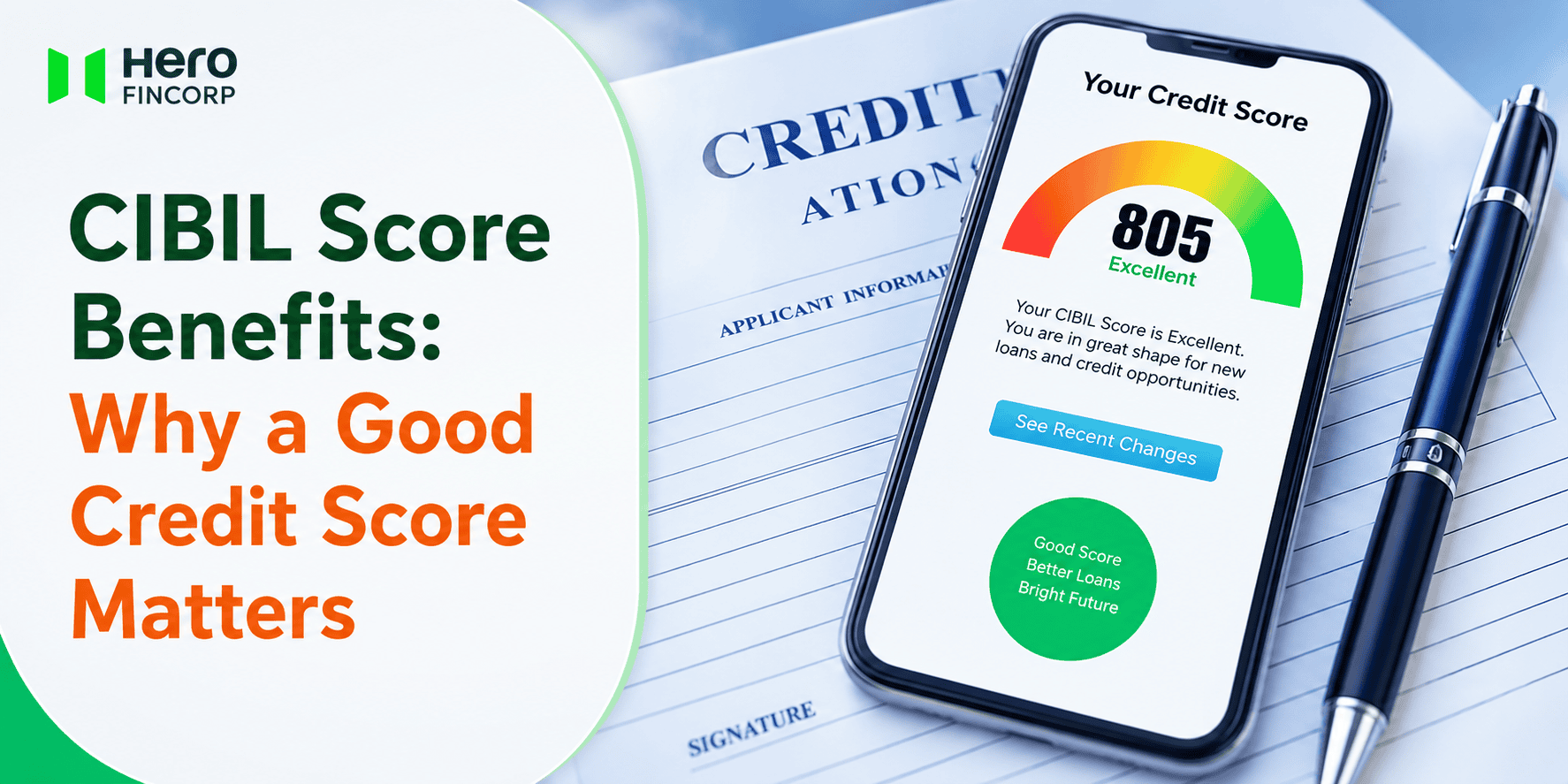

CIBIL stands for Credit Information Bureau (India) Limited now part of TransUnion CIBIL. Your CIBIL score is a three-digit number between 300 and 900 that represents your creditworthiness based on your borrowing and repayment history.

A score closer to 900 indicates strong credit discipline. A score below 650 signals risk to lenders. Lending institutions use this score as the primary filter when evaluating loan and credit card applications.

The score is generated from data reported by lending institutions, including payment history on EMIs, credit card bills, loan accounts, and credit enquiries. TransUnion CIBIL compiles this data into your CIBIL report, from which the score is derived.

CIBIL Score Range: What Each Bracket Means

| CIBIL Score Range | Rating | What It Means for You |

| 750 – 900 | Excellent | Fastest approvals, lowest interest rates, highest loan amounts |

| 700 – 749 | Good | Strong approval chances, competitive interest rates |

| 650 – 699 | Fair | Approval possible but with higher interest rates or stricter terms |

| 600 – 649 | Below Average | Limited options; may need collateral or a co-applicant |

| 300 – 599 | Poor | Most applications rejected; rebuilding credit is essential |

A score of –1 or 0 means you have no credit history (called “new to credit” or NH/NA). This is not the same as a poor score; it simply means there is no data for CIBIL to evaluate.

What is a Good CIBIL Score?

A CIBIL score of 750 and above is considered good by most lending institutions in India. At this level, you are likely to receive faster approvals, lower interest rates, and higher sanctioned amounts. Scores between 700 and 749 are also viewed favourably, though interest rates may be marginally higher.

The average CIBIL score in India falls in the 650 - 700 range. If your score is in this bracket, you can still qualify for loans from NBFCs and select lending institutions, though the terms may not be as competitive.

How is CIBIL Score Calculated?

TransUnion CIBIL uses a proprietary algorithm that weighs four key factors from your credit history. The weightage is as follows:

| Factor | Weightage | What It Covers |

| Repayment History | 35% | Whether EMIs and credit card bills are paid on time |

| Credit Utilisation Ratio | 30% | How much of your available credit limit you are using |

| Credit Mix & Duration | 25% | Balance of secured vs unsecured loans and length of credit history |

| Credit Enquiries | 10% | Number of hard enquiries from loan/credit card applications |

Also Read: Credit Utilisation Ratio: Meaning, Calculation & How To Improve

Key Update: Bi-Monthly Reporting

As per current regulatory guidelines, lending institutions now report repayment data to credit bureaus on the 15th and last day of each month. This means your CIBIL score updates more frequently than the earlier once-a-month cycle. Positive changes like clearing a credit card balance can reflect within 2 - 4 weeks.

Why is CIBIL Score Important?

- Loan Approval: Your CIBIL score is the first screening criterion. A score below the lender’s threshold means automatic rejection before income or employment is even reviewed.

- Interest Rate: Applicants with 750+ scores typically receive the most competitive rates. A lower score can add 2 - 4% to your interest rate, significantly increasing the total cost of borrowing.

- Loan Amount: A strong score signals repayment capacity, enabling lending institutions to sanction higher amounts with confidence.

- Faster Processing: High-score applicants often benefit from pre-approved offers and faster disbursal timelines.

- Negotiating Power: With an excellent score, you are in a position to negotiate better terms lower processing fees, flexible tenure, or waived charges.

Under RBI guidelines, if a lending institution rejects your application based on your credit score, they are required to provide the specific reason in writing.

CIBIL Score Required for Different Loans

| Loan Type | Preferred Score | Notes |

| Personal Loan | 725+ | NBFCs may consider 650+ with strong income proof |

| Car Loan | 700+ | Secured loan; lower scores may qualify with higher down payment |

| Business Loan | 750+ | Unsecured; lenders are stricter on credit profile |

| Loan Against Property | 650+ | Secured by property; credit score threshold is lower |

| Credit Card | 750+ | Premium cards require higher scores; basic cards may accept 700+ |

Hero FinCorp Personal Loans generally prefer a CIBIL score of 725+ along with a monthly income of Rs 15,000+ for salaried and self-employed individuals aged 21 - 58. Applicants with lower scores may still qualify if they demonstrate income stability and a strong employment record.

How to Check Your CIBIL Score Online

Under current regulations, every individual is entitled to one free credit report per year from each of the four bureaus: TransUnion CIBIL, Equifax, Experian, and CRIF High Mark.

Steps to Check Your CIBIL Score

- Visit the official TransUnion CIBIL website (cibil.com)

- Sign up or log in with your credentials

- Enter your PAN number and personal details

- Complete identity verification

- View your CIBIL score and detailed credit report

Checking your own score is a “soft enquiry” and does not affect your CIBIL score. Only “hard enquiries” triggered when a lending institution pulls your report during a loan application can impact your score.

Also Read: How to Check Your Current CIBIL Score by PAN Card Number?

How to Improve Your CIBIL Score

- Pay Every EMI and Bill on Time: Repayment history carries 35% weightage. Even one missed payment can drop your score by 50–100 points.

- Keep Credit Utilisation Below 30%: If your credit card limit is Rs 1 lakh, keep outstanding balances under Rs 30,000. High utilisation signals over-dependence on credit.

- Avoid Multiple Loan Applications: Each hard enquiry leaves a mark on your report. Space out applications by at least 3–6 months.

- Maintain a Healthy Credit Mix: A combination of secured (car loan, LAP) and unsecured (Personal Loan, credit card) accounts shows balanced credit management.

- Do Not Close Old Credit Accounts: Older accounts with clean repayment history lengthen your credit age, which positively impacts your score.

- Dispute Errors on Your Report: Incorrect entries wrong outstanding amounts, duplicate accounts, misreported defaults can drag your score down. RBI guidelines require bureaus to resolve disputes within 30 days.

- Reduce Outstanding Debt: Paying down existing balances, especially on credit cards, can show results within one billing cycle under the bi-monthly reporting system.

Factors That Can Hurt Your CIBIL Score

- Late or Missed Payments: The single biggest negative factor. Even 30 days past due gets reported.

- Loan Defaults or Settlements: Settling a loan for less than the full amount is recorded as “settled” not “closed” and stays on your report for up to 7 years.

- High Credit Utilisation: Consistently using more than 50% of your credit limit raises red flags.

- Too Many Hard Enquiries: Multiple loan applications within a short window suggest financial stress.

- Being a Loan Guarantor: If the primary borrower defaults, it reflects on your credit report as well.

CIBIL Score vs. CIBIL Report: What is the Difference?

| CIBIL Score | CIBIL Report | |

| Format | A single three-digit number (300–900) | A detailed multi-page document |

| Contains | Overall creditworthiness rating | Full account details, enquiry history, personal information, defaults |

| Used For | Quick eligibility screening | Detailed underwriting and risk assessment |

| Updated | Each time the report is updated | On the 15th and last day of each month |

Both are important. A lending institution first checks your score for a quick pass/fail decision, then reviews your full report before final approval.

How Long Does a Low CIBIL Score Last?

A low score is not permanent. Negative entries like missed payments, defaults, or settlements remain on your report for up to 7 years but their impact fades over time. With consistent repayment discipline, most borrowers see noticeable improvement within 12 - 18 months for minor issues (late payments) and 24 - 36 months for major ones (defaults, settlements).

Under the bi-monthly reporting cycle, positive behaviour reflects faster than before. Paying off a credit card balance or clearing an overdue EMI can begin to lift your score within weeks.

Checking Your Eligibility with Hero FinCorp

As a registered NBFC, Hero FinCorp evaluates your credit profile alongside income stability and employment history when processing loan applications. A CIBIL score of 725+ strengthens your application for a Personal Loan, though applicants with lower scores are considered on a case-by-case basis.

You can check your free credit score through Hero FinCorp’s online portal without affecting your CIBIL score. Knowing where you stand before applying helps you avoid unnecessary hard enquiries and plan your borrowing effectively.

Conclusion

Your CIBIL score is the gateway to credit in India. It determines approval, interest rates, and borrowing limits across Personal Loans, car loans, credit cards, and business financing. Maintaining a score of 750+ through timely repayments, low credit utilisation, and regular monitoring gives you the strongest position when you need funds. Check your score regularly, dispute any errors promptly, and build credit habits that compound over time.

Frequently Asked Questions

What is the full form of CIBIL?

CIBIL stands for Credit Information Bureau (India) Limited. It is now part of TransUnion CIBIL and operates as India’s primary credit information company, regulated under the Credit Information Companies (Regulation) Act, 2005.

What is a good CIBIL score for a Personal Loan?

A score of 750+ is considered ideal. Most NBFCs, including Hero FinCorp, prefer scores of 725 and above for Personal Loans. Scores between 650 and 724 may still qualify with strong income proof.

What is the minimum CIBIL score for a car loan?

Most lending institutions prefer a score of 700+ for car loans. Since car loans are secured against the vehicle, lenders may consider slightly lower scores with a higher down payment.

What does a CIBIL score of 1 or 0 mean?

A score of -1 or 0 indicates no credit history (often labelled NH or NA). It means the borrower is “new to credit” with no data available for scoring. This is different from a poor score.

How can I improve my CIBIL score quickly?

Pay off high credit card balances, rectify report errors, and ensure all EMIs are current. With bi-monthly reporting now active, improvements can reflect within 2 - 4 weeks.

Does checking my own CIBIL score lower it?

No. Checking your own score is a “soft enquiry” and has zero impact. Only “hard enquiries” by lending institutions during loan applications can affect your score.

What is the maximum CIBIL score?

The maximum CIBIL score is 900. Achieving a score in the 800 - 900 range places you in the top tier of creditworthiness in India.

What is the CIBIL score limit for loan eligibility?

There is no single legal limit. Each lending institution sets its own threshold based on risk appetite. Generally, 750+ qualifies for the widest range of products at the most competitive rates.

How often is my CIBIL score updated?

Lending institutions report data to CIBIL on the 15th and last day of each month. Your score updates accordingly, making it more dynamic than the earlier monthly cycle.

What is the difference between CIBIL score and credit score?

CIBIL score is a specific credit score generated by TransUnion CIBIL. India has four credit bureaus CIBIL, Equifax, Experian, and CRIF High Mark each generating its own score. CIBIL is the most widely referenced by lending institutions.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Somewhere behind every loan application sits a name most borrowers never bother to ask about. Nine times out of ten it's CRIF, licensed by the Reserve Bank of India alongside just three others. Whatever they report back can be the difference between a quick yes and a frustrating delay, which is reason enough to figure out what CRIF actually is and how it compares to CIBIL.

If you’ve been wondering why my credit score is decreasing, the answer is usually linked to recent changes in how you use credit, repay loans, or how lenders report your activity.

Nobody thinks about their CIBIL score until a loan application is in front of them. By that point, years of high credit card utilisation, a couple of missed EMIs, or just never having borrowed at all have already shaped the number sitting in the bureau's records.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.