What Are the Pros and Cons of Taking Multiple Loans?

Your current loan is manageable, but suddenly an unexpected expense comes up. It could be a medical emergency, your child's education, or even a wedding. Your savings are not enough, so you start thinking about another loan.

But is taking multiple loans a smart financial decision? Or will another EMI put too much pressure on your monthly budget?

Many borrowers face this situation. While another loan can help you meet an urgent need, it also adds to your repayment responsibility. This blog will help you know when to borrow and when to wait, which can save you from financial stress.

Can You Legally Take Multiple Loans at the Same Time?

Many people believe they must repay one loan before applying for another. In reality, there is no such rule in India. You can take multiple loans if you meet the lender's eligibility requirements.

Lenders do not approve or reject an application based only on the number of active loans. They mainly check whether your income can support another EMI. They also review your credit score, existing repayments, and repayment history before making a decision.

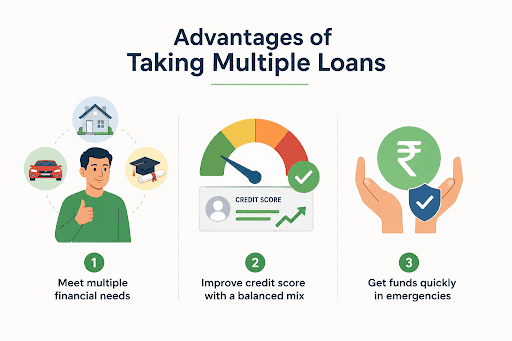

Advantages of Taking Multiple Loans

Taking another loan is not always a poor financial choice. If you borrow for the right reason and repay every EMI on time, multiple loans can help you manage important expenses without disturbing your long-term financial plans.

Meeting Diverse Financial Requirements Simultaneously

You may face another major expense while repaying an existing loan. A second loan can help you manage both without putting all the pressure on your savings.

Improving Credit Score Through a Balanced Credit Mix

Paying all your EMIs on time shows that you manage credit responsibly. This can improve your credit score over time and increase your chances of getting future loans.

Immediate Access to Funds During Emergency Contingencies

An emergency can put unexpected pressure on your finances. If your budget allows, another loan can give you quick access to funds when you need them most.

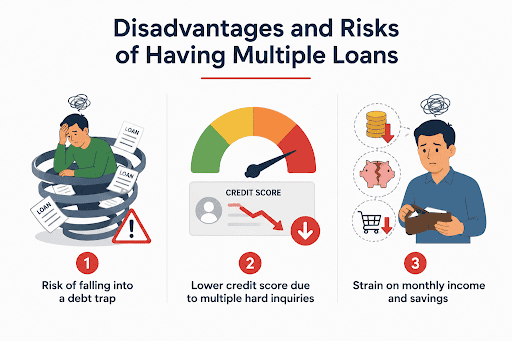

Disadvantages and Risks of Having Multiple Loans

The benefits may look attractive, but every new loan adds another monthly responsibility. Before you borrow again, understand how multiple EMIs can affect your finances in the long run.

High Risk of Falling into a Vicious Debt Trap

Another loan may seem like an easy solution today. But if you cannot manage all your EMIs, you may need another loan just to repay existing ones.

Negative Impact on Credit Score Due to Multiple Hard Inquiries

Applying for several loans at once can lower your credit score. Lenders may think you are under financial pressure, which can make it harder to get your loan approved.

Severe Strain on Monthly Disposable Income and Savings

Before taking another loan, calculate how much money will remain after paying all your EMIs.

Example:

Monthly income = ₹80,000

Existing EMIs = ₹25,000

New loan EMI = ₹15,000

Total EMIs = ₹40,000

Balance for household expenses and savings = ₹40,000

If the remaining amount is too low to comfortably cover your monthly needs, postponing another loan may be the wiser decision.

How Lenders Evaluate Multi-Loan Applications?

Lenders look at your overall financial situation before approving another loan. They check if your income can support all your existing and new EMIs.

Assessment of Fixed Obligation to Income Ratio (FOIR)

FOIR shows how much of your monthly income already goes towards fixed payments like EMIs. A lower FOIR tells lenders that you still have enough income to manage another loan.

Example:

Monthly income = ₹1,00,000

Total monthly EMIs = ₹40,000

FOIR = 40%

A lower FOIR generally improves your chances of getting another loan.

Evaluation of Debt-to-Income (DTI) Ratio and Credit History

Your income should be enough to manage all your EMIs. Lenders also check whether you have paid your previous loan EMIs on time.

Actionable Tips to Manage Multiple Loans Successfully

Managing multiple loans does not have to feel stressful. A few simple steps can help you stay on top of your EMIs and avoid repayment problems.

Prioritize High-Interest Debt Consolidation

If you are struggling to manage multiple EMIs, combining high-interest loans into one loan may make repayments easier and help you stay on track.

Leverage Automated Repayments and Budget Tracking Tools

Auto-debit helps you pay your EMIs on time. Reviewing your monthly budget also helps you control your spending and avoid repayment problems.

Should You Take Multiple Loans?

Taking multiple loans can work well when you borrow within your repayment capacity. Before applying, check if another EMI fits your monthly budget and long-term financial goals.

If you need funds, Hero FinCorp can help you make an informed decision. Use the Personal Loan Eligibility Checker and EMI Calculator to plan better, then apply easily through the Hero FinCorp Personal Loan App with a simple digital process.

Frequently Asked Questions

How many personal loans can a person have at one time?

There is no fixed legal limit for personal loan. Your eligibility depends on your income, existing EMIs, credit score, and the lender's policies.

Does having multiple loans reduce your CIBIL score?

No. Multiple loans alone do not reduce your CIBIL score. Missing EMIs, making late payments, or applying for many loans within a short time can affect it.

Is it wise to take out a new loan to pay off an existing one?

Yes. Taking a new loan for an emergency expense is a good option. Ensure that the interest amount is low and the EMIs are manageable after your monthly expenses.

What is the maximum Debt-to-Income (DTI) ratio allowed by lenders?

There is no fixed limit for all lenders. Many lenders prefer a lower DTI ratio because it indicates you have sufficient income to manage another loan.

Can I get two different types of loans from the same bank simultaneously?

Yes. If you meet the lender's eligibility criteria, you can take different loan products from the same lender at the same time.

What happens if I miss an EMI payment for one of my multiple loans?

When you miss an EMI payment for one of your multiple loans, the lender charges a late fee. Also, your credit score falls, and your chances of getting loans in the future decrease.

How long should I wait before applying for another loan?

There is no mandatory waiting period. Apply only when your income is stable, and you are confident that you can manage another EMI comfortably.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.