What Are Non-Performing Assets (NPA) - Meaning and Types

Imagine you’ve lent ₹50,000 to a friend. The plan was they’d pay you back in monthly installments. But after three months, they stopped paying. For you, that loan just became risky.

In banking, when repayments slip for 90 days or more, the loan turns into a non-performing asset (NPA). Suddenly, the money you expected no longer flows. This matters a lot for all borrowers, including banks and NBFCs.

Let’s take a deeper look at what NPA really means and how it affects banking.

Understanding Non-Performing Assets (NPA)

For a bank or NBFC, any loan is considered an asset because the interest or EMI payments constitute income. When these payments stop, that asset stops performing.

Loans that the borrower has stopped making interest payments on for a predetermined amount of time are considered non-performing assets. According to rules issued by the Reserve Bank of India (RBI), a performing asset becomes an NPA when it is 90 days past due.

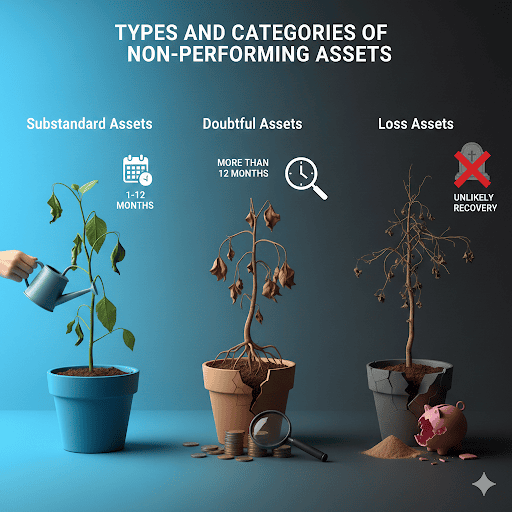

Types and Categories of Non-Performing Assets

NPAs are categorised by banks and NBFCs according to the duration of non-performing loans. The classification gets worse the longer it is past due.

The primary kinds are as follows:

Substandard Assets

These are loans overdue for up to 12 months. The lender sees higher risk, but recovery is still possible with follow-up and collection efforts.

Example: A personal loan where EMIs haven’t been paid for five months, but the borrower is still reachable and promises to regularise payments.

Doubtful Assets

Loans that have remained NPA for more than 12 months fall here. The chances of full recovery become slim, and lenders typically increase provisioning for potential losses.

Example: A business term loan overdue for 15 months, with irregular communication and partial, delayed payments.

Loss Assets

Loss assets are where recovery is considered highly unlikely or negligible, even if some legal action is still in progress. The bank writes off most of the outstanding amount as a loss.

Example: A loan secured against collateral that has lost most of its value, or where the borrower is insolvent, and the bank decides to write off the amount.

Need quick funds? Install our instant loan app and apply in just a few steps!

Impact of Non-Performing Assets on Banks and NBFCs

When loans become non-performing, the risks move from paper to reality. The financial health of lending institutions takes a direct hit:

- Loss of interest income reduces profitability and weakens quarterly performance

- Higher provisioning requirements eat into capital reserves, affecting Capital Adequacy Ratio (CAR)

- Lower capital limits fresh lending capacity, slowing credit growth across the economy

- Liquidity is strained as funds are locked in legal recovery instead of generating returns

- Cost of capital increases, making future lending more expensive for borrowers

- Confidence among investors and depositors declines, hurting market valuation and trust

- Increased regulatory scrutiny, including prompt corrective action in severe cases

- Reputation damage impacts the bank’s ability to attract high-quality customers

- Operational focus shifts from growth to recovery, delaying expansion plans

Calculating NPA Ratios: Formula and Explanation

Banks use NPA ratios to measure the quality of their loan book. Two key metrics:

| NPA Ratio | What it does | Formula |

|---|---|---|

| Gross NPA Ratio | Measures total bad loans without adjustments | (Gross NPAs ÷ Gross Advances) × 100 |

| Net NPA Ratio | Shows actual risk after deducting provisions made for bad loans | (Gross NPAs - Provisions) ÷ (Gross Advances - Provisions) × 100 |

Understanding Gross NPA vs. Net NPA: Suppose a bank has total advances of ₹1,000 crore. If ₹60 crore are bad loans (Gross NPAs), the Gross NPA Ratio = 6%. If the bank has already set aside ₹40 crore as provisions, Net NPA becomes ₹20 crore. Net NPA Ratio = 2%. This reveals how much actual risk remains after provisions.

Why NPAs Matter Today

NPA levels reflect not just individual loan behaviour but overall financial health. Lower NPAs, with strong provisioning and recovery efforts, indicate a robust lender. Higher NPAs warn of stress, tighter credit availability, and possible ripple effects across the economy.

At Hero FinCorp, we focus on responsible lending, robust credit assessment, and proactive portfolio monitoring to maintain long-term financial stability while continuing to support borrowers through transparent and structured credit solutions. Get in touch with us to learn more!

Frequently Asked Questions

What exactly is a Non-Performing Asset (NPA)?

NPA is a loan or advance where interest or principal repayment has been overdue for more than 90 days.

How much time does it take for a loan to turn into an NPA?

The RBI states that after 90 days of principal or interest not being paid, a loan is considered non-performing.

Is it possible to upgrade or regularize an NPA loan?

Indeed. The loan could be categorized as a standard-performing asset if the borrower pays off all outstanding balances.

What distinguishes net NPA from gross NPA?

The whole value of bad loans is known as gross non-performing assets (NPA); when reserves are taken into account, provisions are subtracted to reveal real risk exposure.

How does an NPA affect a bank’s profitability?

NPAs stop interest income, force higher provisioning, reduce net interest margin, hit profits, and constrain fresh lending.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.