Interest Rate vs APR - Differences and Which Is Better

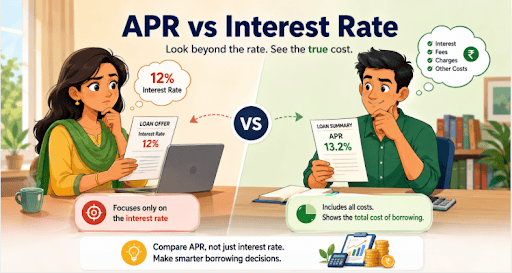

While applying for a personal loan, Sunaina considered only the 12% interest rate offered by a financial institution. On the other hand, Arvind took APR into consideration - the total cost of borrowing.

While Sunaina's loan seemed to be more affordable, in the end, the APR vs interest rates provided Arvind with better insight into the total cost of the loan.

The difference between an interest rate and APR is often misunderstood by many people in India while choosing a personal loan online.

What is an Interest Rate?

The interest rate is the rate of interest paid on the loan amount. For example, taking a loan amount of ₹5 lakh at an annual interest rate of 11.

Interest rate depends on:

- Credit score

- Consistency of income

- Loan duration

- Other liabilities

- Type of loan

What is APR?

APR or Annual Percentage Rate is not only the interest rate but also some other expenses related to borrowing. Annual percentage rate implies the total cost of borrowing annually.

APR includes:

- Interest costs

- Fee processing expenses

- Administrative expenses

- Some documentation costs

Difference Between Interest Rate and APR

The difference between interest rate and APR is best explained by the following comparison:

| Parameter | Interest Rate | APR |

| Meaning | Cost applicable to the principal amount | Total annual borrowing cost |

| Other Fees and Charges | Not included | Included |

| Loan Comparison | Limited | Comprehensive |

| EMI Impact | Affects EMI | Reflects total expense |

| Transparency | Low | High |

| Purpose | Shows the borrowing rate | Shows the cost of the loan |

The difference between interest rate and annual percentage rate lies in transparency. APR gives borrowers a fuller financial picture.

How Are Interest Rates & APR Calculated?

Interest Rate Calculation

Interest is calculated using this formula:

- Interest=P×R×T/100

Where:

- P = Principal amount

- R = Interest rate

- T = Time period

APR Calculation

APR includes interest cost and other charges and fees incurred over a year.

- APR=[(Total Interest + Fees)/Loan Amount]×100

APR vs Interest Rate Example

Let us understand the difference between interest rate and annual percentage rate with an example:

Suppose Arvind takes a personal loan of ₹4 lakh for 3 years.

Loan Offer A

- Interest rate - 11.5%

- Processing fee - ₹14,000

Loan Offer B

- Interest rate - 12%

- Processing fee - ₹4,000

Loan Offer A could appear cheaper due to its lower interest rate. But, after the processing fee and other loan charges are added, the APR of Loan A becomes higher than that of Loan Offer B.

This is why borrowers must compare the APR rather than focus only on the interest rate.

Also Read: What is a Loan Interest Rate? Meaning, Types & How It Works in India

Tips for Comparing Interest Rates and APRs

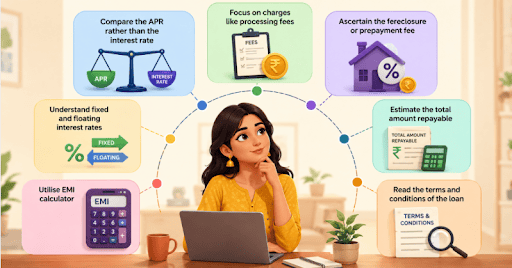

Before you compare interest rates and APR, make a note of these helpful loan comparison tips:

- Compare the APR rather than the interest rate

- Focus on charges like processing fees

- Ascertain the foreclosure or prepayment fee

- Understand fixed and floating interest rates

- Estimate the total amount repayable

- Utilise Hero FinCorp EMI calculator

- Read the terms and conditions of the loan

Loan application can also be managed electronically by using Hero FinCorp loan application - Android/iOS.

Interest Rate or APR: Which is Better?

The answer to 'which is better, APR or interest rate', is based on what you want to measure.

For measuring your monthly EMI affordability, the interest rate is enough. But for comparing borrowing costs, APR is better.

APR vs interest rate has been compared time and again, and APR has the edge due to its greater clarity and other factors.

You must review both before making any loan decision.

Making Loan Interest-Related Informed Decisions

Evaluating the difference between APR and interest rate helps borrowers understand the cost of borrowing. Interest rates are the cost of borrowing, while APR gives a broader picture by including additional costs.

It is important to consider both before choosing a loan. With this useful information, you can make an informed decision about the right loan type.

For more options, consider Hero FinCorp's personal loan web journey and check your eligibility today.

Frequently Asked Questions

Which is better - APR vs interest rate?

Both have their advantages. The interest rate can be used to assess EMIs, while the APR can help assess the total borrowing cost.

What is the difference between interest rate and annual percentage rate?

The interest rate applies to the loan amount, which is the rate at which interest is charged. APR includes the interest rate, other fees, and loan charges.

Is the processing fee included in the APR calculations?

Yes. The processing fee is included in the APR calculations.

Can two loans have the same interest rate but different APRs?

Yes. This happens when the processing fees or other factors, such as tenure or loan type, differ between loans.

What would be a reasonable APR for Indian loans?

This is subjective, as it depends on factors such as the type of loan, its duration, and market conditions.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Taking a personal loan is the easy part. Managing the EMIs, month after month, is where the real work begins.

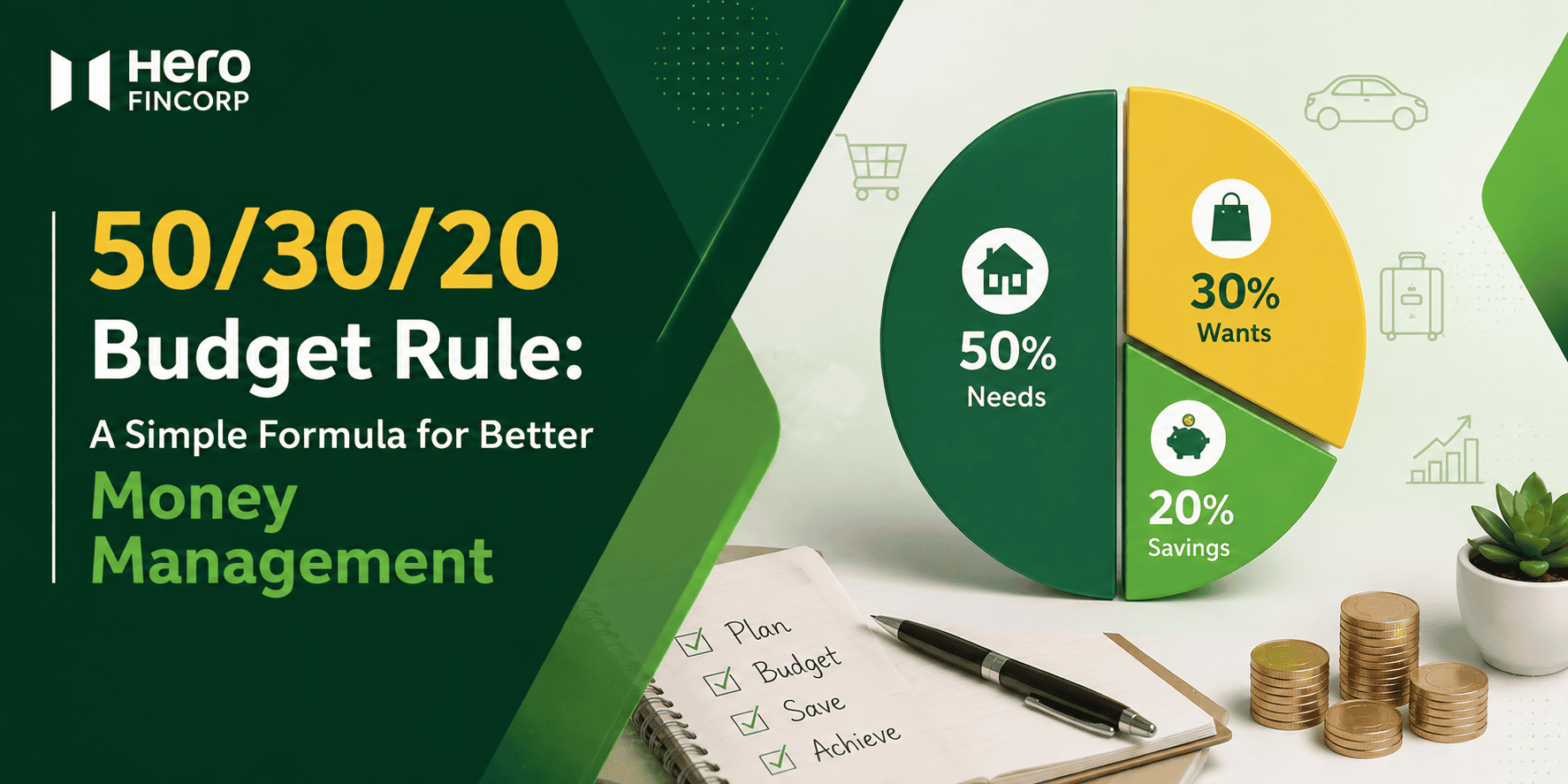

You look at your bank balance in the middle of the month. You think about where your salary went. This happens to a lot of people. The 50/30/20 budget rule is a way to stop feeling bad about how you spend your salary.

Every month, a slice of your salary vanishes into something called “PF”. It’s easy to treat it as just another deduction, but that deduction is quietly building your retirement corpus, tax-free. Understanding PF in salary, such as what it means, how it’s calculated, and when you can withdraw it, helps put you in charge of your long-term financial health. Let’s decode it without the jargon.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.