End of Month Blues? Here’s How to Borrow Smart and Sleep Well

As the end of the month approaches, you worry about managing your finances till you get your paycheck for the next month.

Bills are due, and expenses keep piling up beyond what you had planned.

If you have ever found yourself staring at your bank account balance and wondering how you'll make it till payday, a personal loan is a great option to support you.

But before you pick a personal loan, you need to consider multiple factors.

Let's find out how a personal loan works and tips to borrow smartly.

Understanding the End-of-Month Financial Crunch

End-of-month blues are the stress you feel when your expenses outpace your income. Common reasons include:

- Unexpected emergencies (medical bills, repairs)

- Variable income cycles (freelancers, gig workers)

- Overspending earlier in the month

- Delayed payments or reimbursements

How does a Personal Loan work?

A personal loan is an unsecured borrowing. You do not need to provide collateral to obtain the loan. Mostly, the loan gets approved based on two factors: Income and credit score.

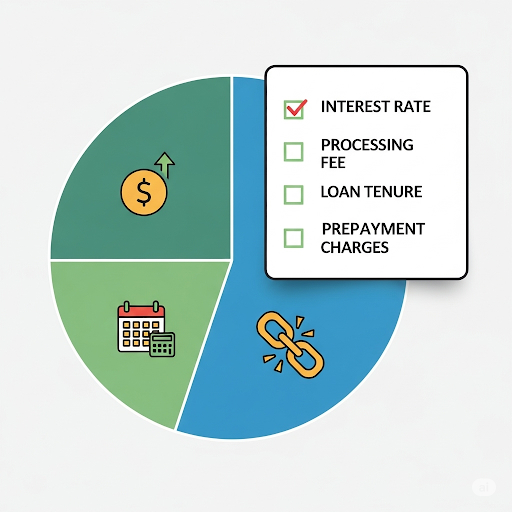

Let's find out the factors that decide the cost of a personal loan:

- The interest rate charged by the lender

- Processing fee charged to process the loan

- The repayment period of the personal loan

- Fees you pay when you pay off the loan before the tenure

Tips to Borrow Smartly

When you borrow a personal loan, a few tips can help you get the best deal.

Here's how to borrow smartly:

Maintain a High Credit Score

Keep a credit score of 750 or above. A higher credit score assures the lenders of your credibility and helps you get a loan at lower interest rates.

Here's how to increase your credit score:

- Pay credit card bills and EMIs on time

- Keep credit use low, preferably below 30% of your credit card limit

- Do not apply for multiple loans or credit cards at the same time

- Check your credit score regularly for errors and get them corrected

Also Read: Personal Loan Without Itr

Compare Multiple Options

Interest and loan terms vary across NBFCs. Don't pick the first offer you get. Compare multiple lenders to get the lowest rate.

Check the interest rate, processing fee, or other hidden charges before finalising the offer.

Apply via the instant loan app to ensure faster processing.

Go for A Shorter Loan Tenure

While you get lower EMIs on longer loan tenures, they increase the cost. With a shorter loan tenure, you save money.

Check For Special Offers

Many banks and NBFCs offer discounts and offers during festive seasons or based on employer tie-ups.

- Check seasonal discounts

- See if your salary account bank offers a lower interest rate

- If you work at a reputed firm, you may get lower interest rates due to company tie-ups

Consider Pre-approved Options

If you have a good repayment history, you may get pre-approved loans with:

- Lower interest rates

- Zero or minimal processing fees

- Instant disbursal of the loan amount

Avoid Unnecessary Add-Ons or Fees

Lenders may sell an insurance policy along with the loan. This increases the cost. While loan protection can help you, it also adds to the cost.

- Ask for a clear breakdown of the charges

- Decline any unnecessary add-ons

- Read the fine print to check hidden fees

Consider A Loan Against Fixed Deposits Or Other Assets

If you have fixed deposits or other assets, consider getting a loan against them. These help you:

- Get a low interest rate as they are secure loans

- Flexible repayment terms

- Fast approval with minimal documentation

Negotiate the Terms

If you have a good relationship with your lender or bank, or there is an existing loan that you paid on time, make sure to negotiate a bit.

Balance Transfer

If you already have a personal loan at a higher interest rate, transfer it to the one with a lower interest rate. This:

- Reduces EMI burden

- Lowers interest costs

Strategies for Repayment

Repaying the loan on time helps you maintain a good credit score. Here's what to do to ensure timely payments:

Automate Repayments

Set up auto-debit instructions or calendar reminders. This ensures you never miss a due date.

Monitor Your Debt

Track how much you owe, to whom, and when repayments are due. Use the personal loan app to check your loans and ensure easy planning.

Focus on Building Savings

Start an emergency fund. Even a small one can break the cycle of "end-of-month blues."

Conclusion

End-of-month blues can happen due to any situation, but you need to carefully assess your options. Compare different lenders, look into the details for hidden costs of add-ons, and create a plan for repayment. Plus, pay installments on time and maintain a good credit score.

This helps you get a loan at a lower interest rate and avoid any repayment stress.

And with Hero Fincorp, you get instant personal loan approval in just 10 minutes and quick disbursal. Plus, you get access to the quick loan app to manage your loan efficiently.

Frequently Asked Questions

1. What is the minimum CIBIL score to get a personal loan?

You should have a minimum CIBIL score of 750+ for quick approval and lower interest rates.

2. How to calculate personal loan EMI?

Use a personal loan EMI calculator to get an estimate of the EMIs and plan accordingly.

3. What is the minimum salary required to get a personal loan?

You need to have a minimum salary of Rs. 15000 to get a personal loan.

4. What documents are required to get a personal loan?

You need to provide KYC details (PAN card, Aadhaar card) and proof of income, such as salary slips or ITR, based on your type of employment, to apply for a personal loan.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented here is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.