Revolving Credit vs. Installment Credit

- What is Revolving Credit?

- What is Installment Credit?

- Instalment vs Revolving Credit: Key Differences Explained

- How Instalment and Revolving Credit Affect Your Credit Score in India

- Which Option is Better for You? Factors to Consider in India

- Build Your Life With the Right Credit

- Frequently Asked Questions

Rajat, a software engineer from Kolkata, had his eyes set on upgrading his workstation with a high-end processor, more RAM, the works. But he didn’t want to dip into his hard-earned savings all at once. One friend suggested using a credit card to spread out the payments. Another advised going for a personal loan with fixed EMIs.

Sound familiar? We’ve all been there! Trying to decide between what feels flexible and what feels stable.

That’s where understanding revolving credit vs installment credit becomes important. Knowing how each one works can help you choose the smarter way to borrow, one that fits your goals, spending style, and peace of mind.

Let’s break it down clearly so you can make a confident, stress-free choice.

What is Revolving Credit?

Revolving credit is a type of credit that allows borrowers to use funds up to a predetermined limit, repay, and borrow again. It is flexible and often used for short-term, recurring financial needs, like with credit cards.

What is Installment Credit?

Installment credit is a type of credit where you borrow a lump sum amount and repay it in fixed, scheduled payments, typically over months or years. This is commonly used for larger purchases, such as personal loans or mortgages.

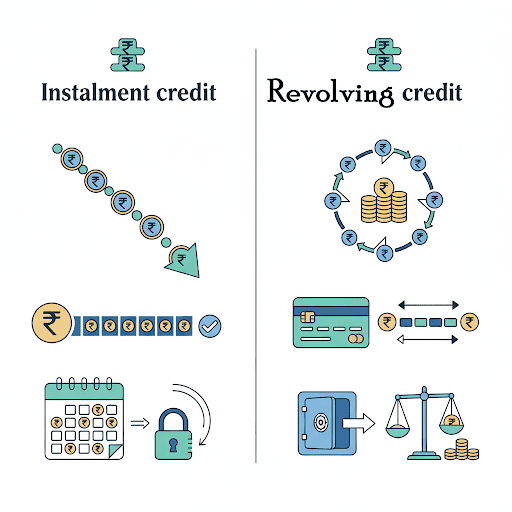

Instalment vs Revolving Credit: Key Differences Explained

Both these credit lines are great ways for you to borrow money, with major differences in repayment and reuse:

| Aspect | Revolving Credit | Installment Credit |

| Principal amount | Can borrow up to the credit limit | Lump sum payment of a fixed amount |

| Repayment | Minimum payment required every month, the remaining can be variable | Fixed monthly instalments |

| Interest rates | Relatively higher | Relatively lower |

| Credit limit access | Can be reused as you pay it off | One-time loan only, no reuse permitted |

| Borrowing method | Ongoing, flexible access | Single disbursement |

| Impact on credit score | Fluctuates with usage | Steady, predictable impact |

| Financial planning | Less predictable | More predictable |

How Instalment and Revolving Credit Affect Your Credit Score in India

Any type of credit you access is bound to affect your credit score. Both revolving and instalment credit hold sway on your score in different ways, such as -

- Instalment credit functions on fixed monthly payments. Therefore, being consistent in these payments helps you improve your credit score.

- Revolving credit functions on utilisation instead of repayment. So, high utilisation lowers your credit score, and low utilisation may improve it.

Ensure you keep your utilisation low and make repayments regularly to increase your credit score. Also, ensure a good credit mix to improve your creditworthiness by showing that you can handle different types of debts together.

Also Read - Credit Utilisation Ratio: Meaning, Calculation & How to Improve

Which Option is Better for You? Factors to Consider in India

Your financial priorities play a critical role when choosing between installment vs. revolving credit in India. If you have planned expenses, like building a house or renovating, or educational requirements, an installment credit is ideal. The fixed installments help you manage your finances for predictable budgeting.

Revolving credit, on the other hand, is better for short-term recurring financial needs. You get the flexibility to borrow funds when you need them repeatedly; however, the interest rates may be higher.

Evaluate these key deciding factors to make the best choice -

- Purpose - Long-term goals require installment credit, while short-term needs can be fulfilled with revolving credit.

- Predictability - Fixed EMIs are better suited for steady budgets, while variable payments are ideal for flexible income.

- Interest rate - Instalment credits come with lower, more stable interest rates as compared to revolving credits.

- Credit history and eligibility - A good mix of credits helps you establish a good trail of credit history for better loan eligibility in the future.

- Emergency vs planned use - Revolving credit is better suited for emergencies (ready access to funds), whereas instalment credits empower planned expenses.

The verdict - After calculating his total requirement of ₹2.5 lakhs, Rajat chose an instalment credit to upgrade his workstation with ease.

Build Your Life With the Right Credit

Access to credit allows you to take that leap of financial faith and invest in your dreams. Instalment credits offer you a structured way of paying back loans, giving wings to those aspirations when needed. If you face emergencies or immediate expenses, revolving credits give you ready access to funds.

However, it is very important that you are financially responsible to maintain your creditworthiness while borrowing, as both these tradelines impact your credit scores in different ways. Reputable lenders like Hero FinCorp take your credit score into consideration to make competitive loan offers, like 10-minute approvals and quick disbursements.

Begin your personal loan journey today with Hero FinCorp.

Frequently Asked Questions

Can I switch between installment credit and revolving credit?

No, they are separate credit types that need individual applications to access.

How does the interest rate differ between installment and revolving credit in India?

Instalment credits offer relatively lower interest rates that remain steady over the term. Revolving credits have higher and variable interest rates.

Which credit type is better for improving my CIBIL score?

Instalment credits with timely and consistent repayment are a better option to improve your CIBIL score.

Are personal loans in India always installment credit?

Yes, personal loans in India are typically installment credits with fixed EMIs.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.