What Is a Credit Utilisation Ratio? Meaning, Calculation and Impact on Credit Score

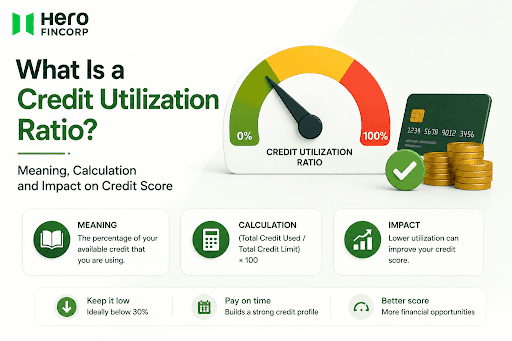

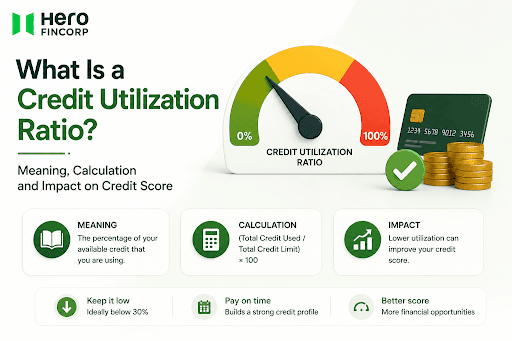

- What Is a Credit Utilisation Ratio?

- What Factors Affect Your Credit Utilisation Ratio?

- How to Calculate Your Credit Utilisation Ratio

- What Is a Good Credit Utilisation Ratio?

- How Credit Utilization Affects Your Credit Score

- How to Lower Your Credit Utilisation Ratio

- Common Credit Utilisation Mistakes to Avoid

- Conclusion

- Frequently Asked Questions

Picture this. Two years of paying every bill on time. Then the CIBIL score drops 35 points in a single month with nothing in the payment history to explain it.

Three credit cards used heavily during the wedding season is all it took. Credit utilisation is one of the biggest parts of your CIBIL score, second only to payment history in importance.

Keeping balances low matters just as much, and most people only find that out after the damage is already done.

What Is a Credit Utilisation Ratio?

The credit utilisation rate answers one question: out of all the credit available, how much is actually being used right now?

If a card has a Rs. 1,00,000 limit and Rs. 40,000 is outstanding, the ratio sits at 40%. Bring that balance down to Rs. 10,000, and it falls to 10%. That part is simple. Where most borrowers get caught out is when the same logic applies across three or four cards at the same time.

Why Credit Utilisation Matters

When a home loan or personal loan application goes in, underwriting systems pull the bureau report and flag high utilisation immediately.

A strong salary and clean payment history do not automatically override what the utilisation number says about spending behaviour. Lenders read the ratio as a signal of financial dependence, and a high one raises their risk assessment regardless of income.

What Factors Affect Your Credit Utilisation Ratio?

Credit Card Balance

The balance on the card when the statement is generated is what CIBIL sees. Card issuers report on the statement generation date, not the payment due date. A Rs. 1,50,000 purchase made five days before the statement cut shows up as high credit card utilisation that month, even if the full amount gets paid by the due date.

Most borrowers do not know this and pay their bills dutifully every month, wondering why the score keeps fluctuating.

Total Available Credit Limit

Most people focus on how much they spend. The credit limit underneath that spending matters just as much.

Take two people, both spending Rs. 30,000 in a month. One has a Rs. 50,000 limit card and ends up at 60% utilization. The other has a Rs. 1,50,000 limit and sits at 20%. Neither changed their spending. Neither missed a payment.

CIBIL reads their profiles completely differently because of a number printed on the back of the card.

Number of Active Credit Accounts

More active accounts with available limits and low balances help both the per-card and overall utilisation calculations. A second card sitting mostly unused is not a liability; it is quietly lowering the overall ratio every month.

How to Calculate Your Credit Utilisation Ratio

Credit Utilisation Formula

Credit Utilization Ratio = (Total Credit Used ÷ Total Credit Limit) × 100

Individual Account vs Total Credit Utilisation

Both per-card and overall utilisation matter. Maxing out one card while keeping another at zero still looks bad to CIBIL, Experian, and CRIF. The aggregate number can look fine while one specific card sitting at 90% pulls the score down independently.

Credit Utilisation Calculation Example

- Card A: Rs. 2,00,000 limit, Rs. 60,000 outstanding

- Card B: Rs. 1,00,000 limit, Rs. 30,000 outstanding

- Total balance: Rs. 90,000

- Total limit: Rs. 3,00,000

Overall credit card utilisation: 30%

Card A in this example has a per-card utilisation of 30%. If that same card had Rs. 1,60,000 outstanding instead, it sits at 80% per-card utilisation and creates a score problem regardless of what Card B shows.

Also Read: CRIF VS CIBIL: Learn Key Differences

What Is a Good Credit Utilisation Ratio?

Below 30% Utilization

Financial experts and credit advisors widely recommend keeping the credit utilisation ratio below 30% of total available credit. This benchmark signals responsible credit management to lenders and credit bureaus.

Below 10% Utilization

A ratio between 1% and 10% is where the highest CIBIL scores cluster. Anyone planning a major loan application in the next three to six months should aggressively target this range in the billing cycles immediately before applying.

How Credit Utilization Affects Your Credit Score

Impact on Creditworthiness

A high credit utilisation ratio signals financial strain. Lenders see it as potential over-reliance on credit and reduce the CIBIL score accordingly. The score drop is not punitive. It reflects how risk models genuinely interpret the data, and the data is telling lenders something worth paying attention to.

Effect on Loan and Credit Card Approvals

Most lenders in India require a minimum CIBIL score of 750. Credit score factors like utilisation directly determine whether that threshold gets crossed. A borrower with 70% utilization and a 710 CIBIL score might have cleared 750 comfortably if the ratio had been managed to 20%. Check your Hero FinCorp personal loan eligibility here to understand where the profile stands before applying anywhere.

Impact on Interest Rates

Lenders reserve competitive interest rates for the lowest-risk borrowers. A healthy credit utilisation rate and strong CIBIL score can save lakhs of rupees over a full loan tenure. The difference between 10.5% and 13% on a Rs. 20 lakh home loan over 20 years is significant enough that managing the utilisation ratio before applying is worth real effort.

How to Lower Your Credit Utilisation Ratio

Pay Outstanding Balances Early

Log in to the bank app a few days before the statement generation date and make a partial payment. This reduces the balance that gets reported to CIBIL and keeps credit card utilisation lower on the bureau report.

The bill can still be paid in full by the due date afterwards.

Request a Credit Limit Increase

After six or more months of clean payments, call the bank and request a higher credit limit. A higher limit against the same spending immediately lowers the credit usage ratio. Most banks consider this routinely for responsible customers, and some proactively offer it without being asked.

Avoid Closing Old Credit Cards

Every card closure reduces total available credit. With the same outstanding balances on other cards, the ratio climbs automatically. The reasons to keep old cards open:

- Total available credit stays higher

- Per-card and overall utilisation both stay lower

- Credit history length is preserved

- The credit utilisation ratio does not spike suddenly on the remaining cards

Spread Expenses Across Multiple Cards

Rs. 80,000 on one Rs. 1,00,000 limit card = 80% per-card utilisation. Rs. 40,000 each on two Rs. 1,00,000 limit cards = 40% per card. Distributing expenses keeps utilisation lower across all cards instead of concentrating damage on one.

Monitor Credit Usage Regularly

Tracking only the primary card misses problems on secondary cards. A borrower might have 10% on the main card but 90% on a secondary card that they check less often. CIBIL looks at aggregate utilisation across all accounts.

Download the instant loan app on Google Play to stay on top of loan eligibility as the credit profile improves.

Common Credit Utilisation Mistakes to Avoid

Maxing Out Credit Cards

Consistently exhausting credit cards causes the CIBIL score to drop. An occasional high month does not cause permanent damage, but sustained high credit card utilisation does.

Closing Unused Credit Cards

Closing accounts reduces total available credit and causes the credit utilisation ratio to rise immediately if balances exist elsewhere. The card being unused is irrelevant. The limit it represents is what matters.

Missing Payment Due Dates

Utilisation does not reset with payment in real-time on the CIBIL report. It updates when the issuer reports, typically once a month at statement generation. Missing due dates compounds the problem by adding a payment default on top of the already-high utilisation score.

Conclusion

The credit utilisation ratio responds faster than almost any other credit score factor. Pay before the statement date, keep balances across all cards below 30%, spread spending instead of concentrating it, and leave old accounts open. Changes made today reflect in the CIBIL report within a single billing cycle. Download the personal loan app on the App Store and apply for a loan once the ratio is in healthy territory.

Frequently Asked Questions

When Do Credit Card Issuers Report Balances to Credit Bureaus?

On the statement generation date, not the due date. Pay before the statement generates to reduce what CIBIL sees that month.

How Does Closing a Credit Card Affect My Credit Utilisation Ratio?

It raises it immediately. Less total credit available means existing balances represent a higher percentage of what is available.

Is 30% a Good Credit Utilisation Ratio?

The upper limit of acceptable. Between 1% and 10% is where the highest CIBIL scores actually sit.

How Long Can a High Credit Utilisation Ratio Affect My Credit Score?

Only as long as the ratio stays high. Pay balances down, and the score recovers within the next reporting cycle, usually within a month.

Can Credit Utilisation Affect Loan Approval?

Yes. A high credit utilisation ratio signals risk and can lead to rejection or higher interest rates, even with a high income.

Does Paying My Credit Card Before the Billing Date Improve My Utilisation Ratio?

Yes, this is the single fastest fix available. Paying before the statement date reduces the balance CIBIL sees that month.

What Happens If My Credit Utilization Exceeds 100%?

Over-limit usage gets flagged as a separate negative entry on the report, on top of the high utilisation. Both hit the score simultaneously.

How Often Should I Check My Credit Utilisation Ratio?

Monthly, a few days before each card's statement date. Anyone planning a loan application soon should check every two weeks. Check your Hero FinCorp personal loan eligibility here once the ratio is under control.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Freelancing and gig work are booming in India. In fact, the number has reached over 7.7 million according to NITI Aayog. 21. And that number is set to reach 23.5 million by 2030.

A friend tells you to check your credit report before applying for a loan. You expect everything to look normal, but an active loan appears that you do not recognize. You start panicking and overthinking about now what.

Applying for a personal loan today is much easier than it was a few years ago. You can check your eligibility, upload documents, and complete the application process without stepping into a branch.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.