RBI Guidelines for NBFC: Complete Regulatory Framework

- Understanding NBFCs and Their Regulatory Importance

- RBI Registration Process and Regulatory Framework for NBFCs

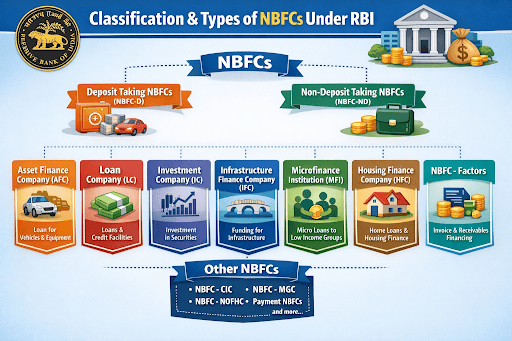

- Classification and Types of NBFCs under RBI

- Classification of NBFCs

- RBI’s Powers, Compliance Requirements, and Enforcement Actions

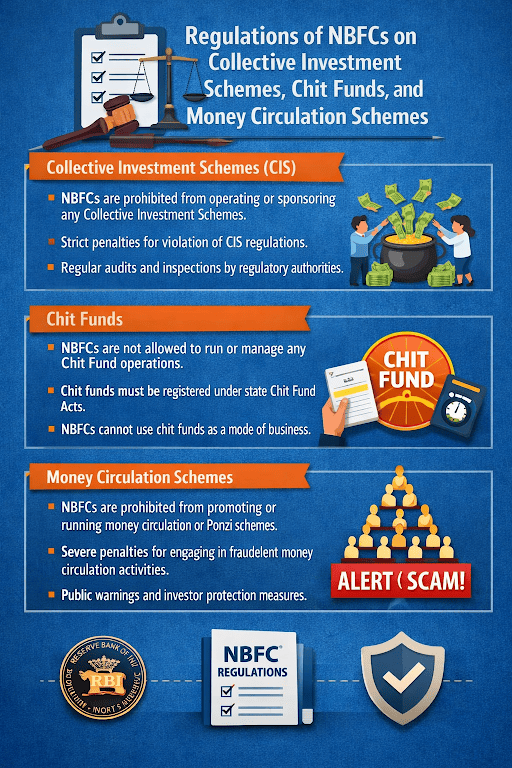

- Regulations on Collective Investment Schemes, Chit Funds, and Money Circulation Schemes

- Factoring Business and Other Specialised NBFC Guidelines

- What This Means for NBFCs

- Frequently Asked Questions

NBFCs (Non-Banking Financial Companies) are crucial entities that help in expanding credit access across sectors where traditional banks often fall short. Unlike banks, they offer easy credit to individuals and groups as and when required.

To ensure transparency and customer protection in these transactions, the Reserve Bank of India (RBI) has established a comprehensive regulatory framework governing NBFC operations. These guidelines include registration and capital requirements to prudential norms, governance standards, and risk management practices.

Read on to know more about what NBFCs are, along with key guidelines by RBI for their smooth operations. We will also discuss various services that these companies offer and how they make it easier for people to get credit.

Understanding NBFCs and Their Regulatory Importance

An NBFC is essentially a financial institution registered under the Companies Act. It offers loans, asset financing, and other investment services to people. However, unlike traditional banks, it does not hold a full banking license.

According to the most recent RBI rules for NBFCs, a company is categorised as NBFC if more than 50% of its total assets are financial assets and more than 50% of its income comes from these assets (also known as the principal business criteria).

RBI Registration Process and Regulatory Framework for NBFCs

The Reserve Bank of India mandate for any company that wants to be an NBFC get a Certificate of Registration under Section 45-IA of the RBI Act, 1934.

Further, the NBFC regulations for the RBI framework also mandate full governance, prudential norms, and periodic reporting.

Here is a stepwise registration process for NBFCs on the PRAVAAH portal-

- Incorporate the company (Companies Act)

- Ensure NOF compliance

- Apply on the PRAVAAH portal

- Upload documents & KYC

- RBI scrutiny & clarifications

Classification and Types of NBFCs under RBI

Under Reserve Bank of India guidelines, NBFCs are primarily classified based on deposit acceptance, size, and activity to ensure tighter risk-based supervision.

Classification of NBFCs

| Basis | Type | Description | Example |

|---|---|---|---|

| Deposit Acceptance | Deposit-Taking | Accept public deposits; stricter compliance norms | NBFCs offering fixed deposits |

| Non-Deposit Taking | Cannot accept public deposits; lighter regulation | Loan companies, fintech NBFCs | |

| Scale-Based Regulation | Base Layer (NBFC-BL) | Small NBFCs with lower risk exposure | Small loan providers |

| Middle Layer (NBFC-ML) | Larger, more regulated NBFCs | Housing finance companies | |

| Upper Layer (NBFC-UL) | Systemically important NBFCs | Large infrastructure lenders | |

| Top Layer (NBFC-TL) | Rare, highest risk entities (if identified) | Selected by RBI | |

| Activity-Based | Investment & Credit Company (ICC) | Loans and investments | Personal loan NBFCs |

| NBFC-MFI | Microfinance lending | Rural finance institutions | |

| NBFC-HFC | Housing finance | Home loan companies |

RBI’s Powers, Compliance Requirements, and Enforcement Actions

The RBI maintains full control over NBFCs to protect consumers and keep the economy stable.

Important Powers and Actions of RBI

- Section 45-IA gives or takes away NBFC registration

- Does inspections, audits, and surveillance from a distance

- Puts fines and limits on how businesses can operate

- Gives instructions on lending standards, governance, and capital adequacy

- Acts against NBFCs that aren't registered and fake deposit schemes

- Puts out warning lists to let people know about illegal businesses

Also Read: NBFC vs Bank: 7 Key Differences & Which is Better for Your Personal Loan?

Regulations on Collective Investment Schemes, Chit Funds, and Money Circulation Schemes

The Securities and Exchange Board of India (SEBI) regulates Collective Investment Schemes (CIS) to protect investors and keep things clear.

The Chit Funds Act of 1982 gives each State Government control over traditional chit funds in the same way. The Reserve Bank of India (RBI) also says that NBFCs can't run any chit fund activities or take deposits for them.

Also Read: What Is an NBFC Personal Loan? Benefits, Eligibility & How to Apply

Factoring Business and Other Specialised NBFC Guidelines

Factoring involves the purchase or financing of receivables under the Factoring Regulation Act 2011, which creates the legal foundation for factoring companies in India.

Below is a summary of the regulations, main features, and recent changes under this act-

- Certificate of Registration (CoR): The Reserve Bank of India (RBI) must issue a CoR to any organization that wants to participate in factoring.

- Minimum Net Owned Fund: This is typically ₹5 crore.

- Eligibility Requirements: The RBI has specified requirements that entities must fulfill.

Also Read: Loan Against Securities Vs Personal Loan

Current Regulations and Amendments

Participation in the factoring industry has increased thanks to the Registration of Factors Regulations of 2022. As long as they meet specific requirements and asset thresholds, NBFCs, including NBFC-Investment and Credit Companies (NBFC-ICCs), can now take part in factoring.

What This Means for NBFCs

The RBI’s regulatory framework for NBFCs is designed to enable growth while ensuring financial discipline. By enforcing strict compliance, risk controls, and governance standards, the RBI safeguards both the financial system and consumer interests.

As the NBFC sector continues to evolve, staying aligned with these guidelines has become a strategic necessity for long-term sustainability and trust.

If you are looking for a trusted NBFC for your financial needs, explore the Hero FinCorp personal loan app to experience a faster, paperless, and secure way to get the funds you need!

Frequently Asked Questions

1. How does the RBI categorise various types of NBFCs?

The Reserve Bank of India categorises NBFc based on factors such as their liabilities, the size or regulatory framework they operate under, and the main business activities they engage in.

2. Can NBFCs accept deposits?

Yes. A very small category (NBFC-D) can take deposits, but only under strict RBI guidelines.

3. How to apply for a loan from an NBFC?

It is very easy to get a loan from an NBFC on its official website or via a dedicated digital lending app.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.