Personal Loan is Smarter Than Using Your Savings

When planning a major expense to achieve your life goals, what is your first choice: using your savings or taking out a personal loan?

Most people instinctively reach for their savings, thinking it's the safest and most straightforward option. After all, it's money you've already set aside and have easy access to.

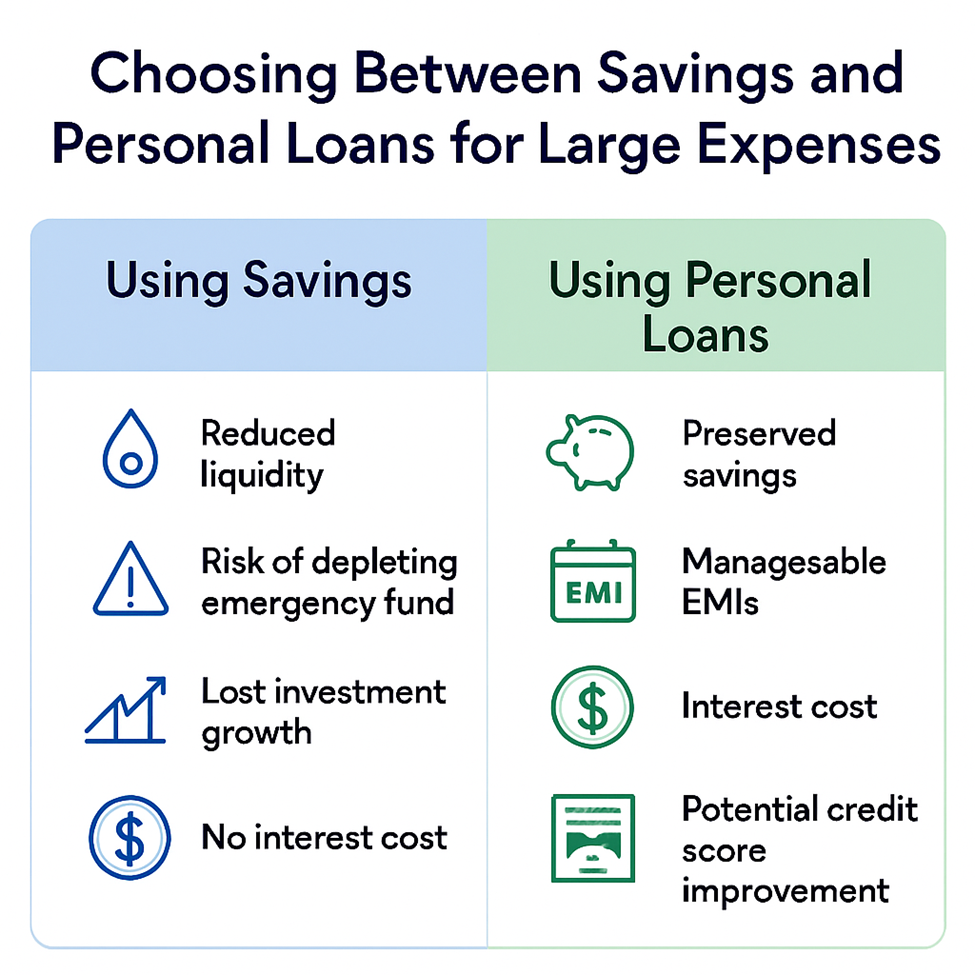

However, using savings isn't always the most strategic move. Draining your savings for a single expense can compromise your financial safety net and delay other goals. In such cases, a personal loan can provide the funds you need while keeping your savings intact and working for you.

Why People Default to Savings

For most people, savings are the go-to option when planning for a major expense.

This is due to a few natural causes:

- Accessibility: You don't need any papers or approvals to use your savings because they are already in your account.

- No Costs or Interest: By eliminating processing costs and loan interest, using your own money makes it an affordable option.

However, since withdrawn funds stop earning interest and compounding over time, depending only on savings could deplete your safety net and prevent you from building wealth.

Use Loans Without Touching Your Savings

A personal loan gives you immediate access to funds without touching your savings. The cost is limited to interest and repayment, which can be seen as a small "convenience expense" for preserving your financial cushion.

Key benefits of personal loans include:

- No need to deplete your financial safety net

- Flexible loan amounts tailored to your expenses

Thus, a personal loan is typically a better, more thoughtful choice, given that you can use your savings to pay for things like your child's education.

Need a quick loan for an emergency? Download our personal loan app and apply instantly!

Personal Loan vs Savings: The Showdown

The decision to obtain a personal loan or utilise your savings ultimately comes down to a few key factors. Say that you require ₹200,000 to pay for your child's college tuition.

Consider the following aspects to determine whether a personal loan or your savings are the better alternative:

1. The Expense

If your savings allow you to cover your child's college fee of ₹200,000 without compromising on your plans, then tapping into your savings may be a good choice. Please keep in mind that savings take a long time to replenish, so you will need to factor that into your calculations.

2. The Cost of a Loan

Suppose you need ₹2,00,000 for your child's college tuition. You decide to take a personal loan at 19% interest. Over the course of a year, you would pay around ₹38,000 in interest.

Now, imagine leaving the ₹2,00,000 in your savings account earning 6% interest. By the end of the year, it would generate ₹12,000 in interest.

By taking the loan, you keep your savings intact and earn ₹12,000, while paying only about ₹3,167 per month as loan EMI. Your savings keep increasing over time, so taking out a loan is a wise approach to cover the cost without depleting your financial cushion.

With our quick loan app, you can get an instant loan for any emergency—simply download our app and apply in minutes!

3. Consideration for Future Corpus

Using the same example, if you withdraw ₹2,00,000 from your savings, you not only lose the ₹12,000 interest it would have earned over a year but also reduce your principal, which could take considerable time to rebuild.

Over the long term, this interrupts the power of compounding and can result in greater financial loss.

On the other hand, the cost of a loan is easily recoverable through your earnings and balances out towards the end of the tenure. This is significantly more beneficial than breaking your savings.

The table below shows a clear comparison between taking a personal loan and using your savings for a major expense:

| Factor | Personal Loan | Savings |

|---|---|---|

| Impact on Financial Cushion | Keeps your savings intact, preserving your safety net | Reduces your financial buffer, leaving you vulnerable to emergencies |

| Flexibility | Loan amount can be tailored to your exact needs | Limited to the amount already saved |

| Opportunity Cost | Savings continue to earn interest and compound | Lost interest on withdrawn savings |

| Repayment | Structured EMIs make repayment manageable | No repayment needed, but future savings replenishment required |

| Long-Term Growth | Preserves the compounding power of savings | Interrupts compounding, potentially slowing wealth growth |

| Ease of Access | Quick approval and disbursal | Immediate access, but it reduces future financial stability |

Take Control of Your Finances with Flexible Personal Loans

When a financial crisis strikes, turning to savings is often the first instinct, but personal loans can offer a more reliable long-term solution. They let you cover big expenses while keeping your savings safe, making it easier to stick to your financial goals.

With Hero FinCorp, you can get instant personal loan approvals within 10 minutes and quick disbursement straight into your bank account. In fact, you get the flexibility to borrow up to ₹5,00,000 and a tenure of up to 36 months.

So why wait? Install our app and get started today to access fast, convenient, and flexible personal loans tailored to your needs!

Frequently Asked Questions

1. Can a personal loan improve my credit score?

Yes, ensuring you have no outstanding debts and paying all your EMIs on time will help improve your credit score.

2. When should I opt for a loan instead of savings?

A personal loan would be a better option if your savings are set aside for a particular objective.

3. What is the opportunity cost of using savings instead of a personal loan?

You can potentially lose the interest gains that your savings would earn over time if left untouched. It may also compromise your financial safety in the long run.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.