Personal Loan Alternatives in India: 8 Smarter Options

Vinod needed ₹6 Lakh to expand his grocery store. A Personal Loan would only cover ₹5 Lakh at 18% p.a. His father’s gold jewellery, valued at ₹8 Lakh, had been untouched for a decade. A gold loan gave Vinod ₹6 Lakh at 11% p.a. in four hours no CIBIL check, no ITR, no branch visit. Two months later, when his business income had stabilised, he closed the gold loan and took a Personal Loan at a competitive rate. Right tool, right moment.

Personal Loans are versatile and fast but understanding the full range of alternatives helps you borrow smarter. This guide covers eight practical alternatives, with a clear comparison of when each makes sense.

Why Consider Personal Loan Alternatives?

| Situation | Better Alternative |

| You have gold to pledge and need funds fast | Gold Loan lower rate, no CIBIL check |

| You own property and need a large amount | Loan Against Property 70–80% of value at lower rates |

| You have an FD you don’t want to break | FD Loan borrow up to 90% at FD rate + 1 - 2% |

| You have an existing home loan | Top-Up Home Loan: lowest rate, minimal documentation |

| You need business cash flow support | Overdraft on current account: pay only on what you use |

| Your employer allows it | Salary advance: zero interest cost |

| You need a small amount quickly | P2P lending: fast, fully digital |

| You want maximum flexibility | Personal Loan: unsecured, no usage restriction |

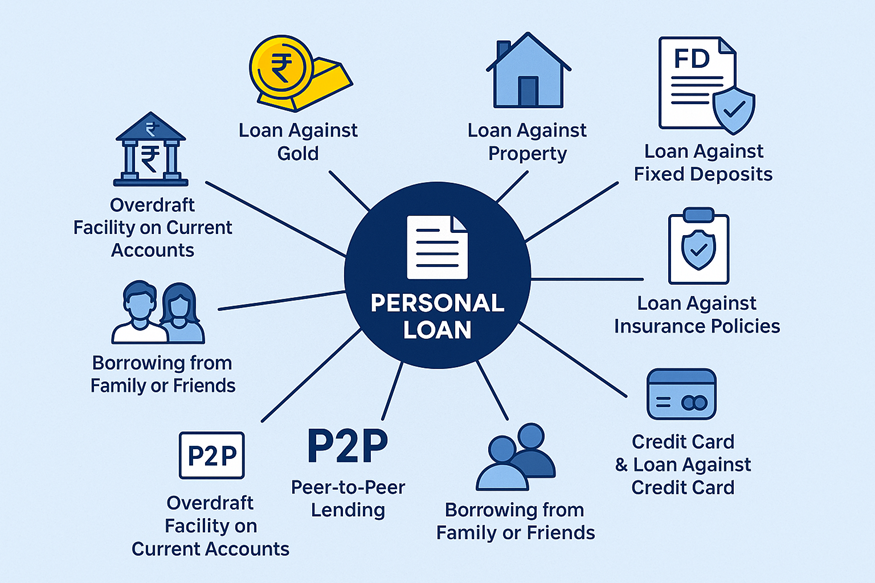

8 Practical Personal Loan Alternatives

1. Loan Against Gold (Gold Loan)

Pledge gold jewellery or coins and receive up to 75% of the gold’s market value. Rates: 8–14% p.a. No CIBIL check. Funds disbursed within hours. The primary risk: defaulting means forfeiture of pledged gold.

Also Read: Gold Loan Vs Personal Loan: Which one is better

2. Loan Against Property (LAP)

Borrow 60 - 80% of your residential or commercial property’s market value. Rates: 8–17% p.a. Processing takes 2 - 4 weeks for valuation and legal checks. Best for large, planned expenses.

3. Loan Against Fixed Deposit

Borrow up to 90% of the FD value at the FD rate + 1 - 2%. The FD continues earning interest. Ideal for short-term liquidity without breaking the deposit.

4. Top-Up Loan on Existing Home Loan

Available to existing home loan borrowers with a clean repayment track record. Rate is at or just above your home loan rate, the lowest available unsecured rate for eligible borrowers. Minimal fresh documentation required.

5. Peer-to-Peer (P2P) Lending

RBI-regulated platforms connect borrowers with individual investors. Rates: 12–28% p.a. 100% digital. Suitable for non-standard credit profiles. Late repayment is penalised and affects CIBIL.

Also Read: Small Personal Loan or Mini Loan: How Are They Different?

6. Overdraft on Salary or Current Account

Pre-approved overdraft facilities on salary or current accounts. Interest charged only on the outstanding amount. Most cost-effective for managing cash flow gaps.

7. Credit Card Loan Against Limit

Loans against existing credit card limits at rates lower than revolving credit (36% p.a.). Pre-approved based on card history. Useful for amounts below ₹2 Lakh where speed is the priority.

8. Salary Advance from Employer

Interest-free short-term advance recovered from future salary credits. Most cost-effective option available. Availability depends entirely on employer policy.

Comparison: Personal Loan vs Key Alternatives

| Product | Typical Rate | Collateral | Speed | Best For |

| Personal Loan | 18–30% p.a. | None | 24–48 hours | Any personal need, up to ₹5L |

| Gold Loan | 8–14% p.a. | Gold jewellery | Same day | Urgent, short-term, any amount |

| LAP | 8–14% p.a. | Property | 2–4 weeks | Large amounts, long tenure |

| FD Loan | FD rate + 1–2% | Fixed deposit | 1–3 days | When FD exists; preserve earnings |

| Top-Up Home Loan | Home loan rate + 0.5% | Existing pledge | 3–7 days | Existing home loan borrowers |

| P2P Lending | 12–28% p.a. | None | 2–5 days | Non-standard credit profiles |

| Overdraft | 12–20% p.a. | None | Pre-approved | Business cash flow management |

| Salary Advance | 0% | None | Same day | Short-term emergencies (employed) |

Also Read: Personal Loan Against Agricultural Land: A Complete Guide for Indian Farmers

When is a Personal Loan Still the Best Option?

- You need funds without pledging any asset, no gold, no property, no FD.

- Loan amount is between ₹50,000 and ₹5 Lakh.

- You prefer a fixed EMI with a defined repayment end date.

- You want no usage restrictions; funds go to your account for any legal purpose.

- Your CIBIL score is 725 or above and income meets the minimum threshold.

Also Read: Know Maximum Personal Loan Amount Limit in India

Frequently Asked Questions

What are the best alternatives to Personal Loans in India?

Loan Against Gold, LAP, and FD Loans are the most cost-effective alternatives. For those with an existing home loan, a top-up is often the cheapest option. For zero-cost short-term needs, a salary advance is unmatched.

Can I get an instant loan without collateral other than a Personal Loan?

Yes. P2P lending platforms and pre-approved credit card loans offer unsecured digital credit. However, Personal Loans from regulated NBFCs like Hero FinCorp remain the most structured, transparent option.

How does a Gold Loan differ from a Personal Loan?

A Gold Loan is secured by pledged jewellery, carries rates of 8–14% p.a., and requires no CIBIL check. A Personal Loan is unsecured, requires CIBIL 725+, and carries rates from 18% p.a. Gold Loans are better for low-cost, short-term needs. Personal Loans offer flexibility and no asset risk.

Can I switch from a Personal Loan to a secured alternative?

You cannot convert an existing Personal Loan to a secured product. However, you can take a secured loan and use those proceeds to prepay the Personal Loan. Confirm prepayment charges with your Personal Loan lender first.

How does my CIBIL score affect access to alternatives?

Gold Loans and FD Loans require no CIBIL check. P2P accepts lower scores at higher rates. Personal Loans and LAP from regulated NBFCs require 725+ for standard approval.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.