Penal Interest: A Comprehensive Guide

- What Is Penal Interest?

- Why Lenders Charge Penal Interest?

- How Is Penal Interest Calculated On Loans?

- How to Avoid Penal Interest on Loans?

- What If You Know You Are Going to Miss a Payment?

- What Is the Impact of Penal Interest on Your CIBIL Score and Future Borrowing?

- HeroFincorp’s Commitment to Transparent Lending Practices

- Frequently Asked Questions

When you compare the various options available to borrow funds, loans often stand out for several reasons. You get access to larger amounts, and interest rates are much lower than credit cards. However, chief among them is the predictable and systematic process of repayments.

That said, if for any reason there is a delay in a scheduled repayment, the amount you owe to the bank can quickly get out of hand. This is primarily due to penal interests. If you don't know what they are, you are in the right place. This post will tell you everything you need to know about them, from why they exist to how they are calculated and more.

What Is Penal Interest?

Penal Interest, as the name suggests, is a penalty in the form of added interest that is levied when an EMI payment has been missed or delayed. It is not a part of the interest component that you already pay as part of your EMI, but rather:

- Applies only when repayment terms are breached, i.e., an EMI payment is delayed or missed altogether.

- It is calculated on overdue amounts, not the total outstanding loan.

- It is time-bound and stops once the dues are cleared.

The penal interest is always mentioned in the loan agreement, so do go through the document carefully before you commit to a loan.

Why Lenders Charge Penal Interest?

Lenders charge penal interest for several reasons.

Lending comes with an element of risk. Delayed payments mean their cashflows are hampered. It also adds to their operational costs as it leads to follow-ups, system adjustments, and additional monitoring.

Penal interest helps offset these operational costs without increasing regular interest rates for compliant borrowers.

Most importantly, it encourages customers to prioritise EMI payments when they know that any delays will incur additional costs.

How Is Penal Interest Calculated On Loans?

Penal interest calculation depends on the terms mentioned in your loan agreement. In most cases:

- A fixed penal interest rate is applied.

- It is charged on the overdue EMI amount.

- It accrues for the number of days the payment is delayed.

However, the exact method may vary by lender and product.

For example, consider that your EMI amount is ₹10,000 per month and is due to be paid on the 5th of each month. Per your loan agreement, the lender will charge you a penalty interest of 2% per month.

If you say pay your EMI on the 15th instead of the 5th, then the penal interest works out to be: EMI × (2% / 30) × 10 days = ₹10,000 × 0.0006667 × 10 ~ ₹66.67

However, this is not the only additional charge you may encounter in the event of a delayed payment. Some lenders also levy a flat late payment fee and/or EMI bounce charges. Additionally, a 18% GST is applied to these extra payments.

Thankfully, the RBI enforces that penal charges are to be non-compounding and can only be levied on overdue amounts.

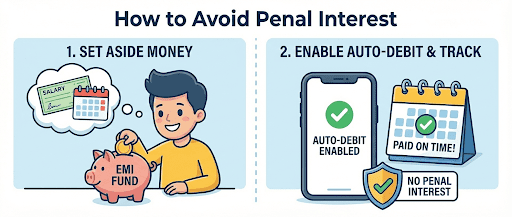

How to Avoid Penal Interest on Loans?

The only way to avoid paying penal interest is to clear your EMI due on time. To do this:

- Set money aside for your EMIs the moment your salary gets credited.

- If you do not have the auto-debit enabled, track your EMI dates carefully.

- If you do have auto-debit enabled, make sure that the account has a sufficient balance.

Most importantly, never over-borrow. Always ensure that your debt-to-income ratio, i.e., all your EMIs put together, is less than 30 to 35% of your take-home income.

What If You Know You Are Going to Miss a Payment?

If, for some reason, you know beforehand you may not be able to pay your EMI on time, get in touch with your lender. They may offer temporary solutions like loan restructuring or guidance, and in some cases, even defer penal charges for a grace period.

What Is the Impact of Penal Interest on Your CIBIL Score and Future Borrowing?

While penal interest itself does not directly lower your CIBIL score, the reason it's levied (the delayed or missed payment) does. Lenders are required by law to report delayed payments to credit bureaus, and each delayed payment drops your credit score by at least 50 points (more if the delay is more than 30 days).

The lower your credit score drops, the lower your access to credit and the possibility of future loans being approved.

Also Read: How to Generate Your CIBIL Score for First Time

HeroFincorp’s Commitment to Transparent Lending Practices

Paying penal interest is the worst-case scenario for anyone already burdened with EMIs. Not knowing about them is even worse. If you are in need of urgent funds, you can apply for a loan with Hero Fincorp.

The whole process is completely digital and completely transparent. You can easily apply for a loan through an instant loan web app or by using the mobile apps available for both Android and iOS.

Frequently Asked Questions

Is penal interest charged on the entire loan amount or only the overdue EMI?

Penal interest can only be charged on the overdue amount, not the full loan. This is enforced by the RBI.

Can the interest rates fluctuate during the loan tenure?

Rates are generally fixed as per the loan agreement, unless revised under disclosed terms.

Does HeroFincorp notify borrowers before applying penal interest?

HeroFincorp's loan terms clearly outline when the penalty interest applies. The notifications, however, may depend on product terms.

What’s the difference between penal interest and late payment fees?

Penal interest accrues over time, while the late fee is usually a one-time charge.

How can I check if I have pending penal interest charges?

You can review loan statements or contact the customer support of your lender.

Are there any waivers for penal interest in specific circumstances?

Waivers, if any, depend on your lender and each individual scenario.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.