What is the Minimum CIBIL Score Required for a Loan Against Property?

- Understanding the Minimum CIBIL Score for a Loan Against Property

- Why a Good CIBIL Score Matters for a Loan Against Property

- Key Factors That Influence Your CIBIL Score

- Loan Against Property with Low or No CIBIL Score: What You Need to Know

- Why Choose Hero FinCorp for Your Loan Against Property Needs?

- Apply with Better Preparation

- Frequently Asked Questions

You decide to take a Loan Against Property because you need funds for an important purpose. Since you already own a property, getting the loan seems straightforward. Then the lender asks for your CIBIL score, and suddenly you start wondering if that one number can affect your approval. Many borrowers have the same question. Understanding the minimum CIBIL score can help you apply with more confidence. This guide explains what lenders usually look for and what you can do if your score is lower than expected.

Understanding the Minimum CIBIL Score for a Loan Against Property

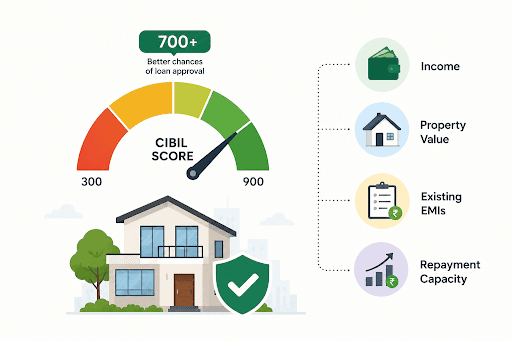

There is no fixed CIBIL score that guarantees a Loan Against Property. Lenders process loan applications more easily when the score is above 700. This is because it shows that you have repaid your previous loans and credit card bills on time.

That does not mean a lower score closes the door. Before making a decision, lenders also check your income, the value of your property, your existing EMIs, and whether you can comfortably repay the new loan.

Why a Good CIBIL Score Matters for a Loan Against Property

A Loan Against Property is usually a long-term financial commitment. Lenders want confidence that you can repay the loan without difficulty. This explains the benefits of the CIBIL score for a loan against property and why borrowers should check it before applying.

A healthy score can offer several benefits:

- Improves your chances of loan approval.

- May help you receive a better interest rate.

- Supports faster loan processing.

- Reflects responsible credit management.

- Can make future borrowing easier.

Key Factors That Influence Your CIBIL Score

Your CIBIL score changes over time based on how you manage credit. Understanding the factors that affect your CIBIL score helps you build a stronger financial profile before applying.

- Pay all EMIs and credit card bills on time.

- Keep your credit card usage within a reasonable limit.

- Avoid applying for multiple loans in a short period.

- Maintain a healthy mix of secured and unsecured credit.

- Check your credit report regularly and report any errors.

Loan Against Property with Low or No CIBIL Score: What You Need to Know

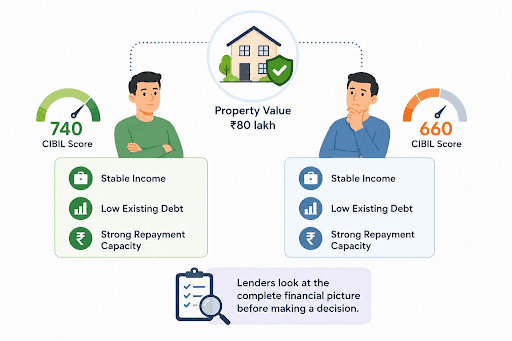

Many borrowers worry that a low score ends their chances of getting a loan. In reality, lenders often look at the complete financial picture before making a decision. If you apply for a loan against property with a low CIBIL score, factors such as stable income, valuable property, and a manageable debt level can strengthen your application.

For example, suppose two applicants offer properties worth ₹80 lakh. One has a CIBIL score of 740, while the other has 660. If the second applicant has a stable income, low existing debt, and strong repayment capacity, the lender may still consider the application after evaluating the overall profile.

Some borrowers also search for a loan against property without a CIBIL score. In practice, most regulated lenders review the credit history before approving a loan. Improving your score before applying usually increases your chances of getting favourable terms.

Why Choose Hero FinCorp for Your Loan Against Property Needs?

Choosing the right lender matters as much as maintaining a good credit score. Hero FinCorp offers a simple borrowing experience with transparent processes and digital support.

Key benefits include:

- Competitive loan amounts based on eligibility.

- Simple documentation and faster processing.

- Flexible repayment options.

- Easy digital application and loan tracking.

- Dedicated customer support throughout your loan journey.

Apply with Better Preparation

Your CIBIL score is important, but it is only one part of your Loan Against Property application. Checking your score early and keeping your documents ready can make the process smoother and help you apply with more confidence.

If you are planning to apply, start by checking your eligibility, reviewing the documents required, and using Hero FinCorp's Loan Against Property EMI Calculator to estimate your monthly repayments. A little preparation today can make your loan journey much simpler.

Frequently Asked Questions

Can I get a loan against property with a CIBIL score below 700?

Yes. You can get a loan against property with a CIBIL score below 700. However, the lender will check your income and overall financial profile.

How does Hero FinCorp evaluate loan applications with low CIBIL scores?

Hero FinCorp checks your credit profile, income, repayment ability, and property details to ensure that you are eligible for the loan.

Is collateral mandatory for a loan against property?

Yes, collateral is mandatory for a loan against property.

What happens if I miss EMI payments on my LAP?

If you miss EMI payments on your LAP, your CIBIL score will drop. This affects your future loan borrowing approvals.

Can self-employed individuals with irregular income get a loan against property?

Yes. Self-employed applicants can qualify if they meet the lender's eligibility criteria.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Rajesh retired a few years ago and now depends on his monthly pension. When his wife needed surgery, he had to arrange a large amount of money. He did not want to sell the family home that he had built over the years. Then, a friend suggested taking a loan against the property instead.

When in the capital city of Delhi and planning to buy a property, there are many financial and legal considerations. The key legal requirements include stamp duty and registration charges.

Imagine you have spent 15 years building a business from scratch. Your commercial property is now worth Rs 1.5 Crore, yet a sudden working capital crunch threatens to stall everything. You need Rs 80 Lakh quickly, affordably, and without disrupting operations. The answer is not always a personal loan or an overdraft. Often, it is a mortgage loan.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.