Personal LINE Of Credit (Ploc) In India: Definition, Benefits and Types

- What Is a Personal Line of Credit (PLOC)?

- Key Characteristics of a Personal Line of Credit

- How Does a Personal Line of Credit Work in India?

- Draw Period vs. Repayment Period

- Types of Line of Credit Loans Available in India

- Common Uses for a Personal Line of Credit

- Personal Line of Credit vs Personal Loan vs Credit Card

- Pros and Cons of a Personal Line of Credit

- How to Apply for a Personal Line of Credit in India

- PLOC vs Personal Loan: Which Should You Choose?

- Frequently Asked Questions

Aman thought he needed money just once but his expenses kept coming in parts. First, there were medical bills, then costs for his freelance work, and later, gaps in his business cash flow. He took a personal loan, but the fixed amount didn’t really help it was either too much or not enough. Aman felt stuck managing it. Then he found a personal line of credit, which let him take money only when he needed it, making things much easier.

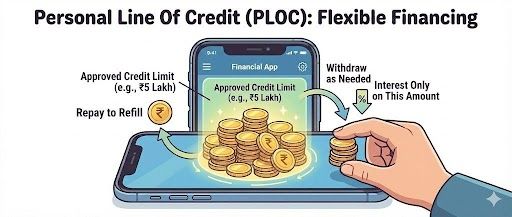

What Is a Personal Line of Credit (PLOC)?

A personal line of credit is a pre-approved, revolving credit facility where the lender approves a maximum credit limit. You draw from this limit as needed once, partially, or multiple times and pay interest only on the amount actually withdrawn, not on the total sanctioned limit.

Once you repay what you've used, the limit is restored and becomes available again. This is the defining feature of revolving credit: unlike a personal loan (where repayment reduces a fixed balance), a PLOC continuously replenishes.

Also Read: Personal Loan vs Line of Credit: Which Borrowing Option Is Right for You?

Key Characteristics of a Personal Line of Credit

- Flexible, On-Demand Withdrawals: Draw any amount up to your approved limit, as many times as needed during the draw period.

- Interest Only on Used Funds: Interest is calculated only on the withdrawn amount not the full sanctioned limit.

- Revolving Credit Limit: Repaid amounts become available again unlike a personal loan where the principal reduces permanently.

- Continuous Availability: Access funds throughout the approved tenure without submitting a fresh application each time.

- No Collateral for Unsecured Facilities: No requirement to pledge assets or property for unsecured PLOCs.

How Does a Personal Line of Credit Work in India?

- Approval: Lender evaluates income, credit score, and repayment history and approves a credit limit.

- Withdrawal: You withdraw funds partially or fully using a linked account or designated disbursement method.

- Interest Accrual: Interest accrues daily on the outstanding drawn balance.

- Repayment: You repay the drawn amount (minimum due or full outstanding) as per agreed schedule.

- Limit Restoration: Repaid amounts are restored to your available credit limit.

Draw Period vs. Repayment Period

PLOCs typically operate in two stages. During the draw period, you can withdraw funds up to the approved limit. Interest is charged on outstanding balances. During the repayment period (which begins when the draw period ends or the credit line is closed), no new withdrawals are permitted, and the outstanding balance must be repaid per the agreed schedule.

In India, many PLOC products offer perpetual flexibility: you can continue drawing as long as you meet minimum repayment criteria, without a formal end to the draw period.

Types of Line of Credit Loans Available in India

- Personal Line of Credit: For individual borrowers covering personal expenses, medical bills, education, or home repairs. Can be secured (backed by an asset) or unsecured.

- Business Line of Credit: For businesses managing working capital, inventory, or operational cash flow. Typically secured against receivables or business assets.

- Key distinction: Unsecured PLOCs require no collateral approval based on income, credit profile, and repayment history. Secured lines offer higher limits but introduce asset risk.

Common Uses for a Personal Line of Credit

- Medical treatment spread over multiple stages or visits

- Education expenses tuition instalments, certification fees, study materials

- Home renovation in phases not all at once

- Freelance or small business working capital needs

- Planned travel or lifestyle spending across multiple months

- Emergency buffer for unpredictable recurring expenses

Personal Line of Credit vs Personal Loan vs Credit Card

| Feature | Personal Line of Credit (PLOC) | Personal Loan | Credit Card |

| Best Suited For | Variable, recurring needs | One-time, lump-sum expenses | Small, frequent purchases |

| Fund Access | Draw as needed up to limit | Full amount upfront | Purchase or cash advance only |

| Repayment | Flexible minimum due or full outstanding | Fixed EMIs each month | Flexible min. due or full payment |

| Interest Charged On | Withdrawn amount only | Full loan amount | Outstanding balance |

| Revolving | Yes, limit restores on repayment | No, balance only reduces | Yes, limit restores on repayment |

Pros and Cons of a Personal Line of Credit

Advantages

- Pay interest only on what you draw not the full sanctioned limit

- Funds are reusable no fresh application needed each time

- Ideal for expenses spread over time, not a single event

- Avoids over-borrowing draw exactly what you need, when you need it

Disadvantages

- Interest rates on PLOCs are often variable your cost can change over time

- Maintenance or annual fees may apply even on unused limits

- Not cost-effective for one-time lump-sum needs (a personal loan is more efficient)

- Requires strict financial discipline interest accrues daily on outstanding drawn balances

How to Apply for a Personal Line of Credit in India

- Eligibility Check: Confirm you meet the eligibility criteria: age 21 - 58 years, minimum income Rs 15,000–30,000 per month, CIBIL score of 725 and above.

- Documentation: Prepare PAN Card, Aadhaar, bank statements (6 months), salary slips or ITR (3 months), and address proof digitally.

- Application: Submit your application via the lender's app or website with digital KYC.

- Activation: Post-approval (typically 2–7 business days), your credit line is activated and accessible.

PLOC vs Personal Loan: Which Should You Choose?

Choose a Personal Line of Credit if: your expenses are spread over time, unpredictable in quantum, and you need the flexibility to draw funds in multiple tranches without a fresh application.

Choose a Personal Loan if: you have a specific, defined one-time expense a medical bill, a purchase, a travel plan and want a fixed EMI repayment schedule with full amount disbursed upfront.

Hero FinCorp offers instant personal loans from Rs 50,000 to Rs 5 Lakh with approvals in under 10 minutes and same-day disbursal ideal for one-time emergency or planned needs. The application is fully digital via the website or app.

Frequently Asked Questions

What is a personal line of credit (PLOC) in India?

A personal line of credit is a pre-approved revolving credit facility where you draw funds as needed up to an approved limit and pay interest only on the withdrawn amount. The limit restores as you repay.

Is a PLOC better than a personal loan?

It depends on your needs. For recurring or phased expenses, a PLOC is more efficient you avoid paying interest on funds you haven't used. For a one-time lump-sum need with a clear repayment plan, a personal loan is simpler and typically more cost-effective.

What CIBIL score is required for a personal line of credit?

A CIBIL score of 725 and above significantly improves approval chances and terms. Scores below this threshold may still be considered depending on income, employment stability, and overall credit profile.

What is the minimum income required for a PLOC in India?

Most lenders require a minimum monthly income of Rs 15,000 to Rs 30,000 for personal line of credit products. Requirements vary by lender and credit limit sought.

What happens if I don't use my approved line of credit?

Interest is not charged on unused portions of your credit limit. However, some lenders may charge an annual maintenance or commitment fee on the sanctioned facility, regardless of utilisation.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Freelancing and gig work are booming in India. In fact, the number has reached over 7.7 million according to NITI Aayog. 21. And that number is set to reach 23.5 million by 2030.

A friend tells you to check your credit report before applying for a loan. You expect everything to look normal, but an active loan appears that you do not recognize. You start panicking and overthinking about now what.

Rohan cleared his credit card bill before applying for a personal loan. Even then, his credit report still showed the old balance, leaving him confused about his score.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.