PSU/MNC Employees Get Better Loans – Here’s Why and How to Improve Your Terms

Aryan and Abhishek are friends who work at an MNC and at a startup, respectively. Last week, they applied for a personal loan with the same bank.

While both of their applications were approved, Aryan received the loan at 19% p.a., whereas Abhishek got it at 24% p.a. The reason? Their company profiles.

Lenders often view PSU and top MNC employees as safer borrowers, so they get better terms. But does that mean others are at a disadvantage? Not necessarily.

This blog explores why lenders prioritise certain profiles and what you can do to improve your loan terms.

Do Lenders Check Employment When Evaluating Personal Loan Applications?

Just like in the case of Aryan and Abhishek, lenders assess every applicant's employment details to judge their personal loan eligibility and decide the terms and conditions. This includes:

- Employment Type - Are you salaried, self-employed, or on a contract?

- Employer Type - Where do you work? Is it a government organisation, PSU, MNC, private company, startup, or small business?

- Income Stability - How consistent is your income? Do you get a fixed salary, or does it fluctuate each month?

What's an Ideal Applicant Profile for Lenders?

From an employment perspective, it's someone with a stable, long-term job at a reputable organisation, backed by consistent monthly income and a clear track record of financial reliability. Someone like Aryan.

Which Loan Terms and Conditions Does Your Employment Affect?

Everyone knows it's important to have a good credit score for a personal loan. But your employment also influences various loan aspects, such as:

Interest Rate

Individuals who work with reputable companies are labelled as low-risk profiles. They tend to get loans at lower interest rates than others.

Loan Amount

Applicants who demonstrate stable employment often get their desired (or sometimes even higher) loan amounts sanctioned than those with unstable jobs.

Tenure Flexibility

Applicants with strong employment backgrounds are often offered longer loan repayment periods. Others usually have to pay back their loan within 12-18 months.

Approval Speed

Self-employed individuals often have to go through various stages of scrutiny and paperwork to get a personal loan. On the other hand, the loan approval for salaried employees is relatively quicker, especially if they're employed with a well-known company.

Want to check your personal loan eligibility? Hurry up and try our Personal Loan Eligibility Calculator now!

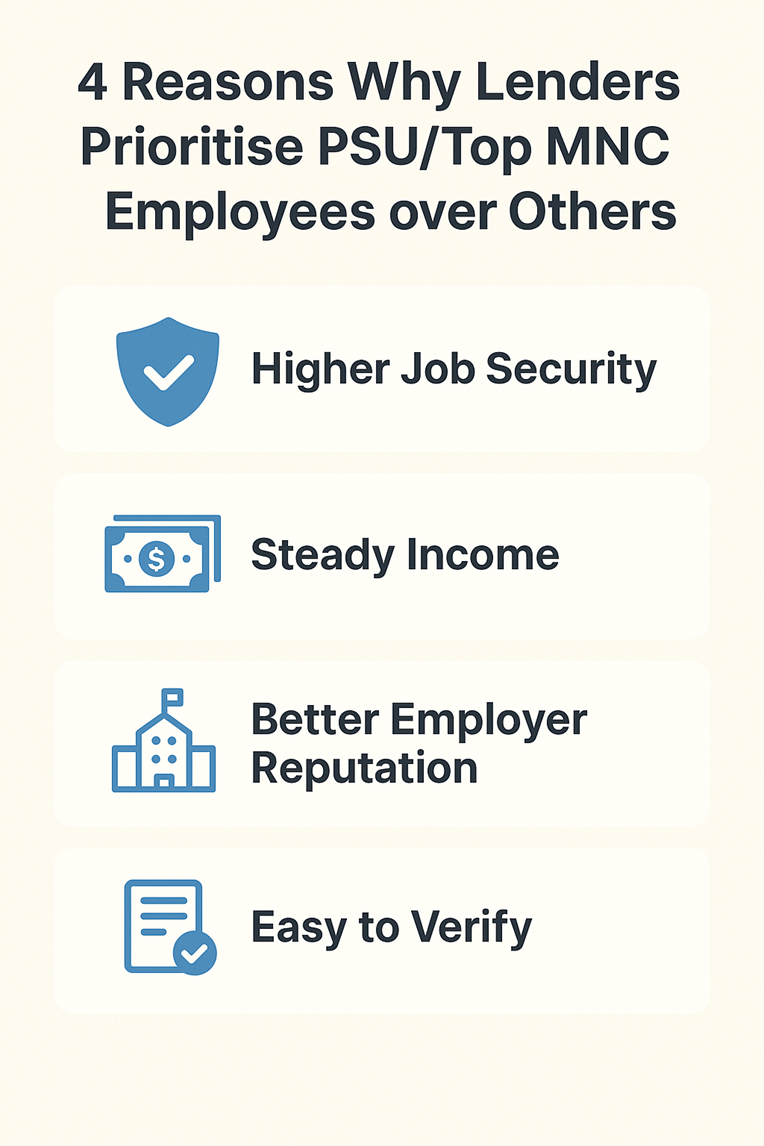

4 Reasons Why Lenders Prioritise PSU/Top MNC Employees over Others

PSU/top MNC employees are pretty much everything lenders look for in an ideal personal loan applicant. Here's why:

Higher Job Security

PSUs and MNCs usually pose lower layoff risks. So, their employees demonstrate greater job security. For lenders, this means a reduced risk of default.

Steady Income

These employees are on the company payroll and receive regular salaries. Such steadiness assures lenders of repayment capacity.

Better Employer Reputation

PSUs and MNCs are large and reputable, which boosts their credibility. This credibility benefits their employees, strengthening their loan applications.

Easy to Verify

These companies usually have detailed employee records. This allows lenders to confirm employment and process applications easily.

Want a personal loan quickly? Check out our Instant Loan App to avail a personal loan without hassle!

What Can You Do to Enhance Your Loan Terms and Conditions as a Non-PSU/Top MNC Employee?

Even if you don't work at a well-known PSU or MNC, you can still get a personal loan at better terms and conditions than your peers. Here's how:

Boost Your Credit Score

A credit score of 750 or higher shows you're responsible with debt. This can help offset concerns about your employer type and even qualify you for lower interest rates.

Reduce Your Debt Consumption

Nearly 50% of Indians use their personal loan for lifestyle expenses. However, reducing the overall amount of debt that you have can help you become more attractive to lenders.

Leverage Your Salary Account

Try applying for a personal loan with the same bank that your salary account is with. It simplifies verification and sometimes also gives you better terms.

Bring in a Guarantor

If your profile is a bit risky, ask a family member to be a guarantor. This can build your creditworthiness and help you get a higher loan amount or a lower rate.

Career and Credit Go Hand in Hand

Your employment profile is very important in how lenders evaluate you. This affects interest rates, loan amounts, and how fast your loan is approved.

PSU and MNC employees may enjoy certain benefits. However, others can still improve their terms by keeping a strong credit score, having a steady income, and building a solid repayment record.

So, what are you waiting for? Apply for a personal loan with Hero FinCorp today. Get up to ₹5 lakhs of instant loan, hassle-free credit in just 10 minutes!

Frequently Asked Questions

1. What's the minimum salary criteria for personal loans?

The minimum salary required to get a personal loan typically ranges between ₹15K to ₹30K. However, it may change depending on the lender's policies, your location, etc.

2. How much personal loan can I get on a ₹30,000 salary?

Banks might offer you a loan of ₹5 lakhs to ₹7 lakhs if you earn ₹30,000 a month. But it depends on your credit and how well you can repay.

3. How to get a low-interest loan?

The best way to get a low rate is to have a stable job at a respected company, like a PSU, MNC, or government job. However, a good credit score and low debt also play a role.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented Here is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.