Alternative Credit Scoring: Benefits, Features & CIBIL Alternatives

- Introduction to Alternative Credit Scoring

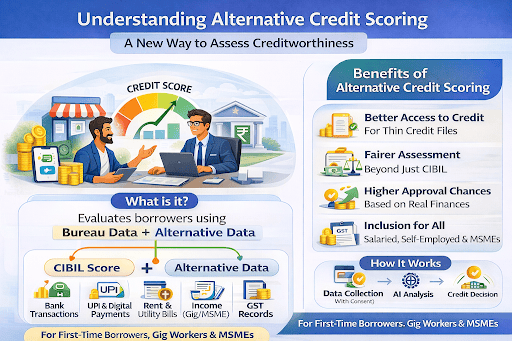

- What Is Alternative Data Credit Score?

- CIBIL Alternative and Its Role in Credit Assessment

- How Alternative Credit Scoring Works

- Benefits of Alternative Credit Scoring

- Key Considerations and Challenges in Using Alternative Data

- How Businesses Can Implement Alternative Credit Scoring

- Regulatory Environment for Alternative Credit Scoring

- Future Trends in Alternative Credit Scoring

- Frequently Asked Questions

- What is alternative credit scoring, and how does it differ from traditional scoring?

- How reliable is alternative data in credit decisions?

- Can alternative credit scoring improve the chances of loan approval?

- What types of alternative data are commonly used in scoring?

- What benefits does a CIBIL alternative credit score offer?

- How is privacy protected when alternative data is used?

Aarav runs a small online business and sees steady monthly inflows into his bank account. Rent and utility bills are paid on time, but formal loans have never been taken out before. When a loan application is rejected due to a thin credit file, it can feel unfair because financial discipline exists, just not reflected on a credit report.

This is where alternative credit scoring changes the picture. Lenders can assess repayment behaviour beyond traditional CIBIL-only models by using broader financial signals.

Introduction to Alternative Credit Scoring

In India, traditional credit assessment relies heavily on bureau data from agencies such as CIBIL. This works well for borrowers with long credit histories. However, many first-time borrowers, gig workers, and MSMEs may have invisible credit.

Alternative credit scoring expands assessment by adding alternative data to understand cash flow stability and payment discipline. This improves financial inclusion while helping lenders reduce false rejections.

Also Read: Personal Loan Without Credit Check: How It Works and Who Can Apply

What Is Alternative Data Credit Score?

An alternative data credit score uses non-traditional ways to evaluate your repayment capacity. They reflect your everyday financial behaviour that does not appear on bureau reports.

Common alternative data used in India:

- Bank transactions: Salary credits, average monthly balance, and inflow consistency

- UPI and digital payments: Frequency and regularity of transactions

- Rent and utility payments: On-time payments

- Gig and freelance income: Marketplace payouts and cash flow seasons

- GST data for MSMEs: Filings and turnover consistency

For example, a regular monthly salary credit of ₹45,000, consistent UPI inflows, and on-time electricity payments over 12 months can indicate stable repayment capacity, even with a limited credit history.

CIBIL Alternative and Its Role in Credit Assessment

An alternative CIBIL approach does not replace bureau scores. It complements them. Traditional CIBIL scoring captures past loans and cards. Alternative models add context using cash flow and payment behaviour.

The combined views help lenders approve deserving borrowers who would otherwise be declined due to thin files. This improves access to formal credit for borrowers without compromising risk controls.

A CIBIL alternative credit score is most effective when bureau data and alternative data are evaluated together.

Also Read: How to Generate Your CIBIL Score for First Time

How Alternative Credit Scoring Works

Alternative credit scoring uses AI and machine learning to assess repayment behaviour and combines it with bureau data. It forms a complete risk profile without relying just on past loans or credit cards.

Your credit assessment becomes strong with on-time bill payments, a stable monthly income, and account balances. Irregular flows or overdrafts may indicate a higher risk.

This approach improves decision-making by detecting fraud and expediting approvals. It also makes outcomes easier to explain in complex cases for review.

Also Read: How To Increase CIBIL Score: Smart Tips to Improve Your Creditworthiness!

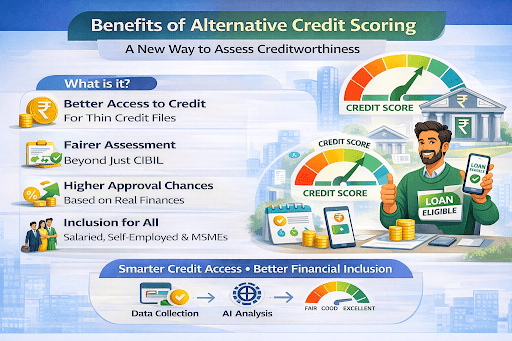

Benefits of Alternative Credit Scoring

- Access to credit becomes possible because borrowers receive fair consideration instead of being rejected due to limited bureau history or thin files.

- The risk profile takes your financial behaviour into account, such as your monthly income and bill payments. It does not rely on your past credits.

- The chances of approval are higher, as disciplined borrowers experience fewer false declines when alternative data strengthens risk assessment.

Also Read: ₹50,000 Personal Loan Without CIBIL Score

Key Considerations and Challenges in Using Alternative Data

- Credit assessment changes when feeds are incomplete or inconsistent, so data quality is critical.

- Privacy and consent are necessary at every stage of data collection, with explicit permission taken before using personal financial data.

- Regular model testing is required because models can unintentionally be biased on fairness.

How Businesses Can Implement Alternative Credit Scoring

- Define clear goals

Set clear approval and risk benchmarks by identifying first-time borrowers or gig workers with thin files.

- Choose reliable data partners

Work with compliant providers for bank, UPI, utility, and GST data, and ensure consent-based, secure data sharing.

- Blend bureau and alternative models

Combine traditional scores with alternative data to improve accuracy without weakening risk controls.

- Pilot and test outcomes

Run small pilots to track approvals and early delinquencies before scaling.

- Refine continuously

Update features and thresholds as borrower behaviour and data quality change.

If eligibility needs to be checked for personal credit, it can be done quickly through Hero FinCorp’s official journey.

Also Read: Business Credit Score vs Personal Credit Score

Regulatory Environment for Alternative Credit Scoring

Responsible use of alternative data requires data collection based on content, purpose, and limitations, as well as the secure handling of personal data. Being transparent about how data is used builds trust.

Governing the model, ensuring explainability, and addressing consumer grievances are important for achieving compliance in India.

Future Trends in Alternative Credit Scoring

The future looks promising, with wider use of real-time bank data, deeper insights into UPI, and better fraud detection using device signals.

You will notice it more across MSME and gig workers as the frameworks for consent mature. However, the focus will be on explainable AI and privacy-focused designs.

Also Read: CIC Full Form in Banking - Complete Guide by Hero FinCorp

Frequently Asked Questions

What is alternative credit scoring, and how does it differ from traditional scoring?

It uses everyday financial behaviour and bureau history. Traditional scoring relies on past loans and cards.

How reliable is alternative data in credit decisions?

Reliability improves when high-quality, consented data is blended with bureau inputs and supported by explainable models.

Can alternative credit scoring improve the chances of loan approval?

Stable bank inflows, regular UPI activity, and timely bill payments can strengthen assessment for thin-file borrowers.

What types of alternative data are commonly used in scoring?

Bank transactions, UPI patterns, rent and utilities, gig income, and GST data for MSMEs.

What benefits does a CIBIL alternative credit score offer?

It reduces false declines and improves risk profiling when combined with bureau scores.

How is privacy protected when alternative data is used?

Data is used with explicit consent, secured storage, limited purpose, and clear disclosures.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

A credit score can seem like a number that has a lot of control over your money. When you learn about the CIBIL score range, you will see how it can help you get loan deals and have your loans approved faster.

You’ve checked your CIBIL score, then glanced at an Experian report, and the numbers don’t match. That confusion is common. Both are RBI-licensed credit bureaus that measure your creditworthiness, but they do it differently. Knowing the CIBIL and Experian difference puts you in control when a lender says they checked one over the other. Here’s exactly how they compare and why both matter.

A CIBIL score is a three-digit number ranging from 300 to 900 that summarises your credit history, repayment behaviour, outstanding debt, and credit mix. It is calculated by CIBIL (Credit Information Bureau India Limited), one of four RBI-approved credit bureaus in India alongside Experian, Equifax, and Highmark.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.