What is Remittance? Meaning and Importance in Banking

- What is Remittance?

- Remitter Meaning in Bank

- Remittance Amount Meaning

- What is Remittance in Banking?

- Types of Remittance

- Importance of Remittance

- How Does Remittance Work?

- Payment Methods for Remittance

- Remittance Transaction Limits

- Documents Required for Remittance

- Remittance Fees, Charges & Hidden Costs

- Benefits of Using Bank Remittance Services

- Things to Consider Before Making a Remittance

- Stay Clear Every Time You Send Money

- Frequently Asked Questions

Ravi does not think much when he sends money home. He opens his banking app, types the amount, and hits send. It has worked the same way for months. Then one evening, his mother calls and says the money has not come. His app shows “completed,” but nothing has reached her account.

That small gap is where confusion begins. If the bank shows success, where is the money stuck? To answer that, you need to understand what happens after you press send.

What is Remittance?

At its simplest, it is just money moving from you to someone else who is not in the same place. People send it to family, for rent, for fees, sometimes just to cover a sudden expense.

Nobody calls it “remittance” in daily life. You just say you sent money. The term appears in banking systems, where every transfer requires a label and a trail.

Remitter Meaning in Bank

Every remittance involves a sender and a receiver. The person who sends the money is called the remitter in banking terms. If Ravi sends money to his family, he becomes the remitter. Banks use this term to identify the transaction initiator and properly track the flow of funds. Knowing this role helps you understand your responsibility in a transfer.

Remittance Amount Meaning

The amount you send may not match what the receiver receives. Charges and rate differences can reduce the final credit.

Example:

You send ₹50,000

The bank takes ₹400 as a fee

Exchange rate adjustment takes another ₹900

What reaches the other side: ₹48,700

That missing ₹1,300 is not random. It comes from charges that sit quietly in the process.

What is Remittance in Banking?

From the outside, it feels instant. Inside, it is not.

Banks pass your request through a chain of command. They check your details, route the money through their network, sometimes through another bank in between, and then finally settle it in the receiver’s account.

Most days, you do not notice any of this. You only start thinking about it when something feels off.

Types of Remittance

Remittances can be grouped by the direction of money flow.

Inward remittance

Money received from another country into India is considered an inward remittance. Families often depend on this for regular support.

Outward remittance

Money sent from India to another country is called an outward remittance. Students paying fees abroad often use this type.

Importance of Remittance

Remittance plays a key role in both personal and economic stability. It supports families and keeps financial commitments on track.

- It helps families manage daily expenses

- It supports education and medical needs

- It contributes to the country’s foreign exchange inflow

- It builds financial connections across borders

How Does Remittance Work?

You see one step. The system handles the rest.

Step 1: You enter details and confirm the transfer

Step 2: The bank checks who you are and why you are sending money

Step 3: The amount moves through banking channels

Step 4: If needed, the currency gets converted

Step 5: The receiving bank credits the account

If any detail is wrong, even slightly, the process slows down.

Payment Methods for Remittance

People use whatever feels easiest.

- Direct bank transfer

- Online transfer platforms

- Wire transfers for international payments

- Demand drafts, though they are less common now

- The method changes, but the idea stays the same.

Remittance Transaction Limits

You cannot send unlimited money whenever you want. Rules exist for a reason

Type | Limit |

Outward remittance | Up to USD 250,000 per year |

Inward remittance | No fixed cap, depends on the source |

Most people never hit these limits, but it helps to know they exist.

Documents Required for Remittance

Banks will not process a transfer without basic checks.

- Identity proof

- PAN card

- Address proof

- Bank details

- Reason for sending money

It may feel repetitive, but it helps keep the system under control.

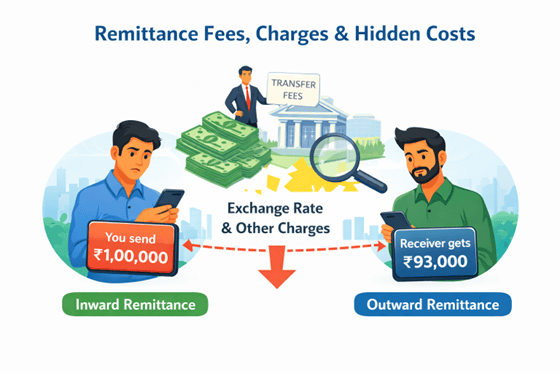

Remittance Fees, Charges & Hidden Costs

The fee you see is only one part of the total cost.

Banks usually charge a transfer fee to process the payment. Additionally, they adjust the exchange rate slightly rather than using the market rate. This difference reduces the final amount the receiver receives, even though it may not be apparent.

In some cases, other banks involved in the transfer may also deduct small charges before the money reaches the final account. When you compare the amount sent with the amount received, these combined costs become visible.

Benefits of Using Bank Remittance Services

Banks do not make the process exciting. They make it dependable.

- Transfers stay secure

- You can track what happened

- Someone is available if things go wrong

- Everything follows clear rules

That consistency matters more than speed in most cases.

Things to Consider Before Making a Remittance

Most issues come from small mistakes.

- A wrong account number delays everything

- Ignoring charges leads to surprises

- Not checking timelines creates unnecessary panic

- Missing records make follow-ups harder

Taking two extra minutes before sending can save you a lot of back and forth later.

Also Read: What is a Bank Account Number and How to Check it Online?

Stay Clear Every Time You Send Money

Once you understand how remittance works, small delays or deductions will no longer feel confusing. You know what to check, where the money moves, and how to stay in control of every transfer. That clarity makes a real difference when you send money regularly.

Choosing the right financial partner helps you manage this better from the start. Hero FinCorp supports you with simple and structured digital tools that make it easier to track transactions and stay organised. With a reliable personal loan app, you can check eligibility, manage your finances, and apply here whenever you need additional support.

Frequently Asked Questions

What is the difference between inward and outward remittance?

One brings money into the country. The other sends it out.

Who is a remitter in a remittance transaction?

The person who sends the money.

What are the typical transaction limits for remittance in India?

Sending abroad is capped at USD 250,000 per year under current rules.

What documents are needed to send money abroad?

Identity proof, PAN card, address proof, bank details, and purpose of transfer.

How are remittance fees calculated, and what should I watch out for?

Fees include transfer charges and exchange rate differences. The final amount received tells the full story.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.