Accrued Interest: Meaning, Types & Calculation

Interest calculations often look simple on paper. A rate. A tenure. A clear EMI. But many borrowers realise something is off when the payable amount is higher than expected. The reason is often accrued interest.

Interest does not wait for EMI dates or payout schedules. It builds up gradually. In this guide, we explain the meaning of accrued interest and how it works.

What Is Accrued Interest?

Interest gained or accrued on a loan or investment is referred to as accrued interest. But this interest hasn't been received or paid yet. Even if the payment is postponed, it accumulates over time.

For example, if interest on a loan is charged daily but EMIs are paid monthly, the interest that accumulates between two EMI dates is accrued interest. The same applies to investments like bonds or fixed deposits, where interest accrues daily but is credited periodically.

Also Read: How is Interest Calculated on Personal Loans?

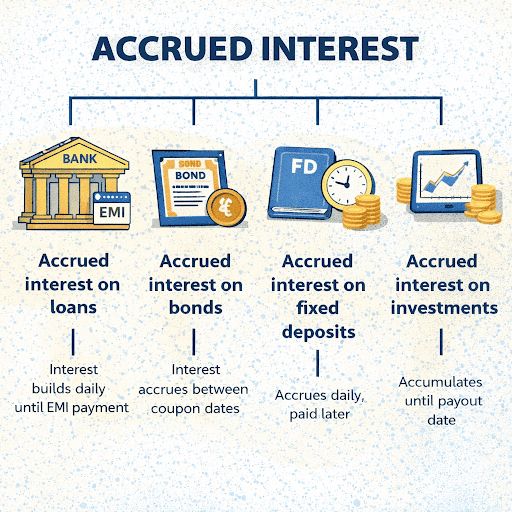

Types of Accrued Interest

Accrued interest applies differently depending on the financial product. Before looking at calculations, it helps to understand the major types of accrued interest.

| Type | What It Applies To | How It Works | Key Distinction |

|---|---|---|---|

| Accrued interest on loans | Personal loans, home loans, business loans | Interest accumulates daily until EMI payment | Increases outstanding balance |

| Accrued interest on bonds | Government and corporate bonds | Interest accrues between coupon payment dates | Paid to seller during bond purchase |

| Accrued interest on fixed deposits | FDs and term deposits | Interest accrues daily but is credited monthly or quarterly | Shown as earned but not yet paid |

| Accrued interest on investments | Mutual funds, debt instruments | Interest builds until NAV or payout date | Impacts valuation and reporting |

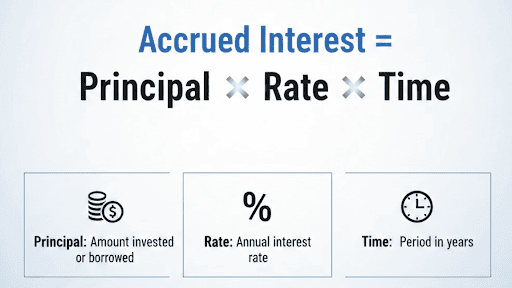

Accrued Interest Formula and How to Calculate It

At its core, the accrued interest formula is straightforward. It depends on three variables.

Accrued Interest = Principal × Rate × Time

Where,

- Principal is the amount invested or borrowed

- Rate is the annual interest rate

- Time is the period for which interest accrues, expressed in years

This formula helps explain how to calculate accrued interest in practical scenarios.

Example 1: Personal Loan

Let's say you take out a ₹200,000 personal loan with a 12% annual interest rate. Interest accrues every day even though you pay monthly EMIs.

- Annual interest rate = 12%

- Interest rate each day = 12% ÷ 365 = 0.0329%

- 15 days is the accrual period.

Interest Accrued = ₹200,000 × 0.0329% × 15

Accrued Interest = ₹987 (approximately)

This ₹987 is the interest that accrues between EMI dates and forms part of your total payable amount.

Also Read: Personal Loan Interest Rates (Latest)

Example 2: Fixed Deposit

You put ₹1,000,000 into a fixed deposit with an annual interest rate of 6%. Although it accrues daily, the interest is credited on a quarterly basis.

- 6% is the annual interest rate.

- Interest rate each day = 6% ÷ 365 = 0.0164%

- 30 days is the accrual period.

Accrued Interest = ₹1,00,000 × 0.0164% × 30

Accrued Interest = ₹493 (approximately)

Even though this amount is not yet credited to your account, it is already earned and reflected as accrued interest.

Example 3: Bonds

You buy a bond that has a ₹10,000 face value. The annual coupon rate is 8%. Every six months, interest is paid. Ninety days following the final interest payment, you purchase the bond.

- ₹10,000 × 8% = ₹800 is the annual interest.

- Interest rate per day = ₹800 ÷ 365 ≈ ₹2.19

- Accrual period = 90 days

Interest Accrued = ₹2.19 × 90

Accrued Interest = ₹197 (approximately)

This ₹197 is paid to the seller at purchase and later recovered by you when the next coupon payment is made.

Take Control of Your Interest Costs with Hero FinCorp

Accrued interest highlights an important truth. Interest is continuous. Not periodic. Knowing how it works helps you read loan statements, investment summaries, and foreclosure quotes with clarity.

At Hero FinCorp, transparency matters. To ensure that borrowers comprehend precisely how their loan expenses are determined, we take care to accurately explain topics like accrued interest.

So why wait? Explore our loan options and use our EMI calculator to plan your finances with confidence!

Frequently Asked Questions

How do I calculate accrued interest?

Use the formula Principal × Rate × Time to calculate accrued interest.

Is the interest that has accumulated taxable in India?

Indeed. Depending on the type of investment, accrued interest is taxable in the year it is generated, even if it hasn't been received yet.

Is the interest that has accumulated a debt or an asset?

Yes. It is an asset for the receiver and a liability for the payer.

Why does my NBFC lender charge accrued interest before the EMI due date?

Because interest accrues daily from the date funds are disbursed, not from the EMI date.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.