UPI for Current Account: Complete Guide for Businesses

- What is UPI for a Current Account?

- How to Register and Link UPI to Your Current Account Step by Step?

- Current Account UPI Transaction Limits

- Benefits of Using UPI for Current Accounts

- Ideal Users of UPI for Current Accounts

- How Does UPI Work With Current Accounts?

- Security and Best Practices for UPI Transactions

- Stay in Control of Your Business Payments

- Frequently Asked Questions

Amit runs a small wholesale business. Payments come in all day, but not in one simple way. One customer sends money on UPI, while another asks for bank details. Someone else still uses a manual transfer. Amit keeps checking his phone and bank app just to be sure about what he received.

This routine starts taking up more time than it should. He ends up sitting with his transactions just to match payments and clear doubts. That takes his focus away from actual work. He begins to look for a way to handle everything in one place. That is where linking UPI to a current account helps. In this guide, you will learn how it works, how to set it up, and what changes once you start using it.

What is UPI for a Current Account?

If you run a business, you already know how important it is to keep payments smooth. Delays or confusion can slow everything down.

UPI for a current account lets you send and receive money instantly using a UPI ID linked to your business account. Since current accounts are built for frequent transactions, this setup fits naturally. You no longer have to rely on multiple methods. Everything moves faster, and every payment leaves a clear record behind.

How to Register and Link UPI to Your Current Account Step by Step?

Getting started with UPI for business accounts involves a few clear steps. Once completed, you can manage payments without switching between systems.

Registration on a UPI app

Step 1: Download any trusted UPI app on your phone.

Step 2: Open it and enter the mobile number linked to your bank account.

Step 3: Complete the OTP verification that you receive.

Step 4: Allow the app to automatically fetch your bank details.

Step 5: Finish setting up your profile inside the app.

Linking your current account

Step 1: Go to the bank account section in the app.

Step 2: Select your current account from the available list.

Step 3: Create a UPI ID that suits your business.

Step 4: Enter your debit card details to set your UPI PIN.

Step 5: Confirm the PIN and complete the linking process.

Current Account UPI Transaction Limits

Limits often depend on the bank you use. They are there to keep transactions secure while still allowing flexibility.

In most cases, a single UPI transaction can go up to ₹1,00,000. Daily limits may be higher, up to ₹5,00,000 for business accounts. Some banks increase limits once your account is fully verified. It always helps to check this in advance so you do not run into issues during important payments.

Benefits of Using UPI for Current Accounts

When payments become easier to handle, daily operations also feel lighter. That is exactly where UPI makes a difference.

- Payments reach your account instantly without waiting

- Security stays strong with PIN-based verification

- Transaction costs remain low compared to other methods

- You can track every payment without confusion

- Daily operations become faster and more organized

Ideal Users of UPI for Current Accounts

Not every setup needs UPI, but for many businesses, it fits perfectly.

- Small and medium businesses handling regular payments

- Companies managing vendor or supplier transactions

- Freelancers working with multiple clients

- Retail shop owners dealing with daily customer payments

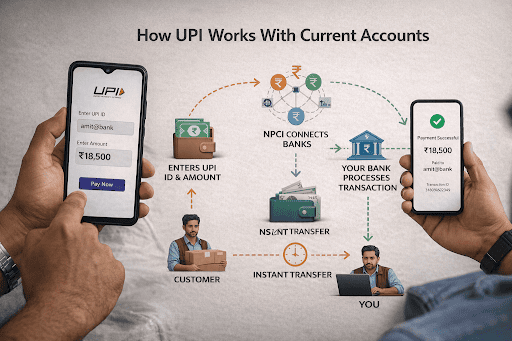

How Does UPI Work With Current Accounts?

Once you understand the flow, everything feels straightforward. The process happens in seconds, even though multiple systems work in the background.

A customer enters your UPI ID and the amount. After that, they confirm the payment using their PIN. The request is sent to the National Payments Corporation of India, which connects the two banks involved. Your bank processes the request and credits the money to your account. Both sides receive confirmation almost instantly.

Security and Best Practices for UPI Transactions

Small habits can make a big difference in keeping your account safe. Most issues happen only when basic precautions are ignored.

- Never share your UPI PIN with anyone

- Use phone lock or biometric security

- Check details before sending money

- Keep your app updated at all times

- Monitor transactions regularly for anything unusual

Stay in Control of Your Business Payments

Handling payments should not feel complicated. When you link your UPI to your current account, things become clearer and easier to manage. You know where your money is coming from and how it moves.

Hero FinCorp supports this journey with simple digital tools. You can explore their personal loan app, check eligibility, and apply here whenever your business needs quick financial support.

Frequently Asked Questions

Can I link my business current account to UPI?

Yes, most banks allow this after basic verification through a UPI app.

What documents are needed for linking?

You need your registered mobile number, debit card details, and a KYC-compliant account.

What is the typical UPI transaction limit for current accounts?

Usually, it starts from ₹1,00,000 per transaction and may increase depending on your bank.

Is UPI secure for business transactions?

Yes, transactions remain secure as long as you follow basic safety practices, such as protecting your PIN.

Can multiple current accounts be linked to one UPI ID?

Yes, you can link multiple current accounts to one UPI ID. While paying, you can choose which payment method to use.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.