Payday Loans vs Personal Loans: Which is Better?

- What is a Personal Loan?

- What is the meaning of Payday Loan?

- Key Differences Between Payday Loans and Personal Loans

- Interest Rates Comparison Between Payday and Personal Loans

- How Does a Personal Loan Work?

- How Does a Payday Loan Work?

- Risks and Debt Cycle of Payday Loans

- Which Loan is Better?

- Choose a Loan That Fits Comfortably Into Your Monthly Budget

- Frequently Asked Questions

Most people do not spend much time comparing loan types until money suddenly feels tight. One option promises cash within hours. Another spreads repayment into smaller monthly EMIs. The difference may not seem important during approval, but it starts to matter as the repayment date approaches.

A short repayment window may work for some people. Others may prefer smaller monthly payments that leave more room in the budget later. This guide explains how these two options work and what people usually overlook before borrowing.

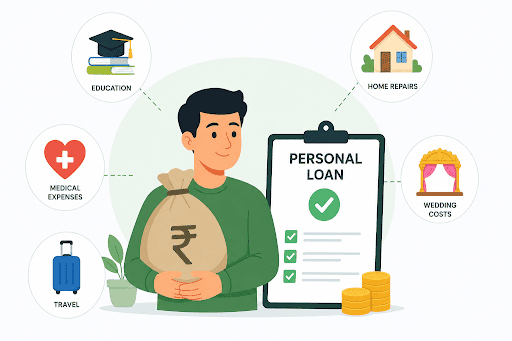

What is a Personal Loan?

A personal loan helps people manage bigger expenses without paying the entire amount immediately. Many people use it for medical treatment, education fees, travel plans, home repairs, or wedding costs.

The repayment usually happens through monthly EMIs spread across several months or years. Smaller monthly payments often feel easier to handle than paying one large amount at once.

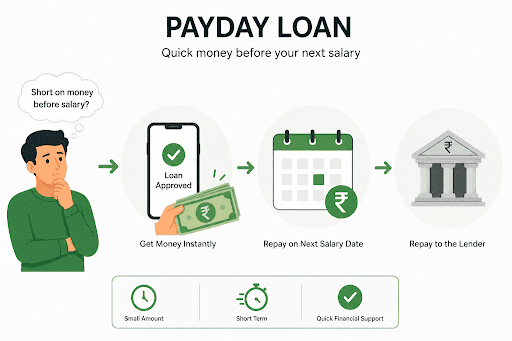

What is the meaning of Payday Loan?

A payday loan gives people quick access to money when the next salary still feels a few days away. The borrowed amount usually remains small, and people repay it quickly.

The fast approval attracts many people during urgent situations. The pressure usually starts later, especially when the repayment date arrives before the monthly expenses settle down again.

Key Differences Between Payday Loans and Personal Loans

The difference usually becomes clearer after the money is deposited into the account and repayment begins.

| Factor | Payday Loan | Personal Loan |

| Borrowing Amount | Smaller amounts | Higher amounts |

| Repayment Time | Few weeks | Several months or years |

| Interest Costs | Usually higher | Usually lower |

| EMI Facility | Rarely available | Commonly available |

| Approval Style | Very fast | Fast with checks |

| Suitable For | Immediate shortages | Bigger planned expenses |

Interest Rates Comparison Between Payday and Personal Loans

Many first-time applicants focus only on how quickly the money arrives. The repayment amount usually gets attention later.

Example:

₹10,000 payday borrowing → Full repayment due within weeks

₹10,000 personal borrowing → Repayment divided into EMIs

One large repayment can be difficult because daily household expenses consume most of the salary. Monthly installments usually feel more manageable because the amount is spread over time.

How Does a Personal Loan Work?

Most lenders now offer fully digital applications. People complete online verification, receive approval, and repay the amount over time through monthly EMIs.

Pros

- Higher borrowing limits

- Longer repayment periods

- Predictable monthly payments

- Lower rates compared to short-term borrowing

Cons

- Eligibility checks may feel stricter

- Approval may take slightly longer

People looking for a paperless borrowing experience can explore Hero FinCorp Personal Loan and apply digitally through the Android or iOS lending app.

How Does a Payday Loan Work?

This option mainly focuses on immediate access to money. Applicants usually receive approval quickly and repay the amount after their salary is credited.

Pros

- Faster approvals

- Minimal documentation

- Helpful during temporary shortages

Cons

- Higher borrowing costs

- Short repayment windows

- Greater chance of repeated borrowing

Many people only realise the pressure later when another unexpected expense appears before the next salary arrives.

Risks and Debt Cycle of Payday Loans

Short-term borrowing can quietly turn into a recurring cycle when repayments keep getting delayed. Some people take another loan simply to clear the previous one because most of their salary already goes towards regular monthly expenses.

Extra charges and penalties can rise quickly during delays. A small cash shortage can slowly become harder to manage month after month.

Which Loan is Better?

The better choice usually depends on how repayment feels later, not how quickly approval happens.

Choose a payday loan if:

- You need a small amount urgently

- Repayment within weeks feels realistic

- The expense cannot wait

Choose a personal loan if:

- You need a higher amount

- You want smaller monthly EMIs

- You need more repayment time

- You want less pressure after salary credit

Choose a Loan That Fits Comfortably Into Your Monthly Budget

Many people focus only on getting the loan approved quickly. The repayment side becomes more important as the due date approaches each month. Choosing the right option early usually makes borrowing feel much easier to manage later.

Need funds without lengthy paperwork or branch visits? Hero FinCorp Personal Loan lets people check eligibility online and apply through a simple digital process. People can also manage repayments easily through the Android and iOS lending app.

Frequently Asked Questions

Can I convert a payday loan into a personal loan?

Yes. Take a personal loan, clear your payday loan with it, and save big on interest.

Why do payday loans have higher interest rates than personal loans?

Short timelines, fast approvals, and no collateral make payday loans risky for lenders. Higher interest rates are how they cover that risk.

Do payday loans affect my credit score?

Yes. Miss a repayment, and your score takes a hit. Miss multiple and the damage is serious.

Can I prepay a personal loan without penalties?

Not always. Some lenders charge a prepayment fee, some don't. Check your loan agreement first.

What happens if I miss the payday loan repayment deadline?

Penalties pile on, and the debt grows fast. Call your lender immediately before it gets worse.

Is it possible to have both payday and personal loans simultaneously?

Yes. Just make sure the combined EMIs are something you can comfortably handle every month.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Two terms that sound almost identical but represent very different stages of the loan process. Mixing them up costs time, sometimes triggers an unnecessary hard enquiry on the credit report, and occasionally sets up expectations that the final application cannot meet.

Flight fares between Delhi and Goa have been known to double in a single week. Spotting a good deal is one thing. Having the full amount sitting in your account on the same day is a different problem entirely.

Seeing a three-digit number flash on your credit report can feel like opening a report card. But when that number reads credit score 777 is it good or bad? In short: it’s not just good, it’s excellent.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.