Write Off vs Waive Off: What Is the Actual Difference?

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

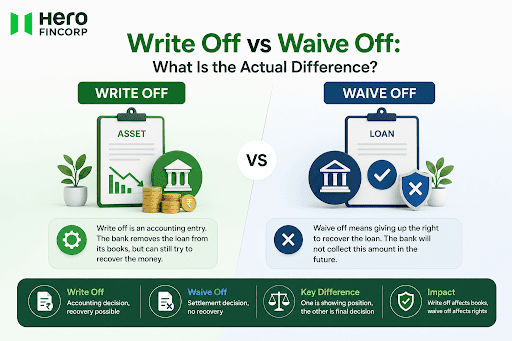

A write-off is just the bank removing the loan from its active books because recovery looks unlikely. The borrower still owes the money.

A waive-off is the one that actually cancels what you owe, and it works completely differently.

Mixing these two up is easy, and it is the kind of mistake that can leave someone thinking they are debt-free when they are not.

Introduction to Loan Write Off and Waive Off

Both terms show up constantly in news coverage of bank losses or farm relief packages.

A write-off happens when a bank removes bad debt from its balance sheet.

A waiver releases a specific group of borrowers from repayment entirely. Knowing the difference between write off and waive off stops you from assuming a debt has vanished when it has not.

What is a Loan Write-Off?

A bank decides recovery on a loan is unlikely and pulls it off the active books. This is an accounting action initiated by the lender. It does not benefit the borrower directly. The debt itself still exists legally.

What actually happens in a write-off:

- The loan moves to a separate non-performing account internally

- Recovery efforts continue, sometimes for years afterwards

- Indian banks wrote off Rs. 2.37 lakh crore of bad loans in FY20 alone

- Public sector banks collectively wrote off around Rs. 6.15 lakh crore between 2015 and 2020

- Banks recovered roughly 13% of those written-off loans, proof that recovery genuinely continues after the fact

What is a Loan Waive-Off?

A waive-off means complete debt cancellation. The borrower owes nothing further once it takes effect. This is real forgiveness, and it happens far less often than a write-off.

How a waive-off typically works:

- Usually, a government-approved relief measure during agricultural crises, natural disasters, or widespread economic distress

- A farmer whose crop failed in a flood might see loans up to a fixed amount cancelled under a state scheme

- The government either compensates the lender directly or absorbs the loss through budget allocations

- Individual borrowers rarely negotiate this on their own; it comes through policy, not personal appeal

Key Differences Between Write-Off and Waive-Off

| Factor | Write-Off | Waive-Off |

| Who Initiates | Bank or lender | Government or authorised authority (in exceptional cases) |

| Debt Status | Still legally payable by the borrower | Fully cancelled |

| Recovery Efforts | Continue, sometimes for years | Stop entirely |

| Purpose | Clean the balance sheet and manage NPAs | Provide relief to distressed borrowers |

| Who Benefits | Lender's financial records | Borrower directly |

| Typical Trigger | Loan overdue for 90+ days with low recovery prospects | Crop failure, natural disaster, or government relief scheme |

| Frequency | Routine banking practice | Rare and policy-driven |

| Legal Status | Accounting reclassification; repayment obligation continues | Legal forgiveness of the borrower's liability |

Waivers need legislative or executive government action.

Write-offs follow RBI's prudential norms for asset classification and provisioning. One is a bank tidying its records. The other is a government cancelling debt outright.

Impact of Loan Write-Off and Waive-Off Borrowers and Lenders

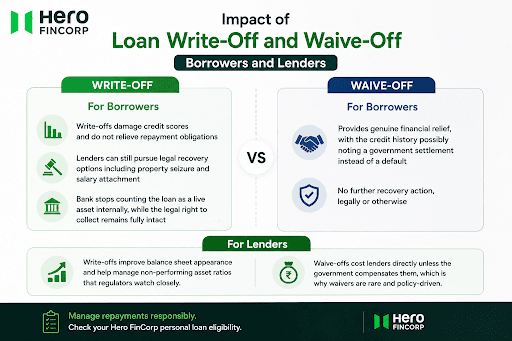

For the borrower, a write-off changes nothing about what is owed:

- Write-offs damage credit scores and do not relieve repayment obligations

- RBI's circular on write-off loans still allows lenders to pursue legal recovery options, including property seizure and salary attachment

- The bank stops counting the loan as a live asset internally, while the legal right to collect remains fully intact

A waive-off works in the opposite direction for the borrower:

- Provides genuine financial relief, with the credit history possibly noting a government settlement instead of a default

- No further recovery action, legally or otherwise

For lenders, the two serve different purposes entirely. Write-offs improve balance sheet appearance and help manage non-performing asset ratios that regulators watch closely. Waive-offs cost lenders directly unless the government compensates them, which is exactly why waivers stay rare and policy-driven rather than something a bank decides on its own.

If you are managing repayments responsibly and want financing that stays transparent from day one, check your Hero FinCorp personal loan eligibility here.

How Write-Off and Waive-Off Affect Credit Scores

Written-off loans appear as serious defaults on credit reports, dropping CIBIL scores by 100 to 150 points. This mark stays on the report for seven years.

What this means in practice:

- Settling outstanding dues still matters even after a write-off, since the underlying obligation has not disappeared

- Once dues are cleared, the lender updates the report to 'Post Write-Off Closed' under RBI's 2025 guidelines

- If the lender does not update it, you can dispute the entry on the CIBIL website with proof of payment

A waive-off behaves differently on a credit report. The debt is legally gone, though a record of government settlement may still appear, without the seven-year default damage a write-off carries. The write off vs waive off credit score gap is one of the clearest practical differences borrowers actually feel.

Process of Loan Write-Off and Waive-Off

A write-off starts internally once a loan crosses 90 days overdue and gets classified as a non-performing asset under RBI norms. It follows RBI's prudential norms for asset classification and provisioning, so the process stays procedural and does not need government involvement.

A waive-off follows a different path entirely:

- Requires a formal government policy or scheme, often announced during agricultural crises or natural disasters

- Eligible borrowers need to meet specific conditions first

- Conditions usually include overdue status, loan amount caps, and geographic or sector eligibility

- The waiver only applies to accounts that clear all these criteria

Conclusion

The difference between write off and waive off comes down to one fact worth remembering: a write-off does not cancel your debt, a waive-off does. Write off vs waive off is not just terminology.

It determines whether you still owe money, what shows up on your credit report, and whether recovery continues. Always confirm directly with your lender which one applies to your account.

Looking for a personal loan with clear, upfront terms? Download the instant loan app on Google Play or the personal loan app on the App Store.

Frequently Asked Questions

What happens to my credit score after a loan write-off?

It takes a real hit, anywhere from 100 to 150 points off your CIBIL score. And it does not bounce back quickly either. That default mark sits on your report for a full seven years, which makes getting approved for fresh credit during that stretch genuinely tough.

Can a lender waive off only part of the loan amount?

Yes, and this happens more often than a full waiver. Government relief schemes typically set a cap, say loans up to Rs. 1 lakh, and only that portion gets cancelled. Anything you owe above that cap stays your responsibility.

Is a loan waive-off available for all types of loans in India?

Not really. These schemes are usually aimed at farmers dealing with crop failure or natural disasters, not the average personal loan or credit card borrower. If you are hoping for a waiver on a personal loan, it is not the route that is typically available.

How does a write-off affect my future loan eligibility?

A write-off on your record can make future approvals more difficult. Lenders see a write-off and read it as serious default risk. The first real step toward rebuilding eligibility is clearing whatever you still owe and making sure your CIBIL report gets updated to reflect that settlement.

Can I negotiate a loan waive-off with my lender?

In most situations, you cannot get a loan waive-off by negotiating directly with your lender. Waivers come through government policy decisions, legislative or executive action, not a conversation between you and your bank's recovery team. If you are struggling to repay, a settlement or restructuring is the more realistic conversation to have.

Does loan write-off mean the debt is forgiven?

This is where most people get it wrong. A write-off just means the bank stopped counting the loan as an asset on its books. You still owe the money. The bank can, and often does, keep trying to recover it long after the write-off happens.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

A cancelled cheque is a common tool used in daily financial and banking processes.

It is required while applying for a loan, starting an SIP, and on several other occasions. It is an ordinary cheque, which is marked so it can’t be used for any payment.

Your current loan is manageable, but suddenly an unexpected expense comes up. It could be a medical emergency, your child's education, or even a wedding. Your savings are not enough, so you start thinking about another loan.

You've done it - you've paid off your loan in full. Congratulations!

But your financial responsibility doesn't end with the final EMI payment. There is only one critical piece of paper you must have: a NOC (No Objection Certificate).

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.