UPI vs IMPS – Which Is Better for Fast Transfers?

- IMPS vs UPI: Detailed Comparison

- Understanding These Differences

- What This Means for Everyday Use

- Benefits of UPI vs IMPS: When to Choose Which?

- UPI for Everyday, Quick, Small-Value Payments

- IMPS for High-Value and Traditional Banking Transfers

- Convenience, Bank Policies and Fees

- Step-by-Step Guide: How to Transfer Money Using IMPS and UPI

- Common Problems and Troubleshooting IMPS and UPI Transactions

- Wrapping Up

- Frequently Asked Questions

Digital payments in India are not limited to one method only; they come in various forms, from scanning QR codes to entering credit card details.

UPI and IMPS are the two major options that are widely used for instant money transfer. Even though both of them are capable of instantly sending funds, they differ in terms of the customer experience, limits, and use cases.

This guide explains how UPI compares with IMPS and when one may be more suitable than the other.

IMPS vs UPI: Detailed Comparison

This table gives a quick sense of how each option works in real, day-to-day use.

| Feature | IMPS (Immediate Payment Service) | UPI (Unified Payments Interface) |

| Transaction Process | Account number + IFSC, or MMID + mobile number | VPA or QR; no account details needed each time |

| Quickness and Dependability | Instant, 24×7 | Instant, 24×7 |

| User Experience | More steps; may need beneficiary setup | Simple, app-based, quick for repeat use |

| Transaction Limits | Higher limits, often up to ₹5 lakh/day (bank dependent) | Usually around ₹1 lakh/transfer for most users |

| Charges & Fees | Small bank fees may apply | Mostly free for personal transfers |

| Security | Standard bank authentication | UPI PIN; bank details stay hidden |

| Accessibility | Bank apps, net banking, SMS/USSD, some ATMs | UPI-enabled mobile apps |

| Additional Features | Primarily bank-to-bank transfers | Bill payments, merchant QR, peer transfers |

Understanding These Differences

IMPS is useful when you need to send a larger amount or prefer traditional bank channels. The process can feel more formal because you must enter full bank details or add a beneficiary first.

UPI is simpler. Once your account is linked, you can pay using a VPA, mobile number, or QR code. Transaction limits are lower than IMPS, but they are usually enough for daily use.

For situations where money transfers don’t cover the full requirement, platforms like Hero FinCorp can offer quick access to funds when needed. Install our instant loan app now!

What This Means for Everyday Use

For convenience, UPI is the smoother choice. It works well for bills, rent, and routine payments. IMPS is better for higher amounts or when you want a more traditional transfer method.

Benefits of UPI vs IMPS: When to Choose Which?

Knowing when to use UPI and when to pick IMPS makes transfers smoother.

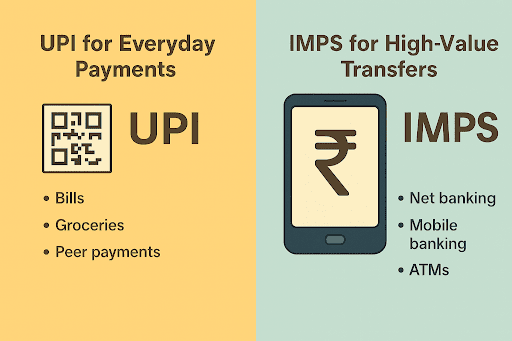

UPI for Everyday, Quick, Small-Value Payments

UPI is great for small and frequent transfers. A UPI ID or QR scan is enough, so it is handy for bills, groceries, and simple peer payments.

Use Cases: Daily purchases, routine bills, quick peer transfers.

IMPS for High-Value and Traditional Banking Transfers

IMPS allows larger transfers, often up to ₹5 lakh a day. It works through net banking, mobile banking, SMS or USSD, and sometimes ATMs.

Use Cases: Rent deposits, urgent high-value transfers, and payments to users who prefer bank channels.

Convenience, Bank Policies and Fees

UPI is usually free and very easy to use. IMPS isn’t the same across banks. Some charge a small fee. So if you’re sending a larger amount, it’s better to see what your bank sets.

If you’re trying to handle your usual payments and something bigger pops up, a little backup can help.

Need funds quickly? Download our personal loan app and apply in minutes.

Step-by-Step Guide: How to Transfer Money Using IMPS and UPI

Here is a simple walkthrough of how each method works and when to pick one over the other.

How to Use IMPS

- Open your bank’s mobile app or net banking and sign in.

- Go to fund transfers and select IMPS.

- Enter the recipient’s account number and IFSC, or use their mobile number and MMID if supported.

- Add the amount and review the details.

- Confirm the transfer and complete the OTP or MPIN step if asked.

How to Use UPI

- Open any UPI app linked to your bank account.

- Choose 'send money' or 'pay'. Enter a UPI ID, mobile number, or scan a QR code.

- Enter the amount and select the bank account to debit, if needed.

- Enter your UPI PIN to finish the payment.

If you like keeping everything in one place, you can check out the Hero FinCorp app on Android or iOS. It gives you quick access to personal loan options and a few tools that make managing money easier.

Choosing IMPS or UPI

- Pick IMPS for higher-value transfers or when the recipient is not using UPI

- Use UPI for quick daily payments, smaller amounts or when you just want to scan a QR or enter a UPI ID

Common Problems and Troubleshooting IMPS and UPI Transactions

When making digital transactions, there may be some issues that arise; however, these problems can be avoided by knowing some of them and a few others up front and how to deal with them.

For instance:

- Transaction Failures: They are often caused by wrong information, low balance, or server issues. Thus, you should check your balance, verify the account number, IFSC, or UPI ID, and try again.

- Amount Debited but Not Credited to the Recipient: Sometimes, the bank or UPI server delays the credit. Most refunds are processed automatically within 24 to 72 hours.

- Limit or Restriction Errors: Your bank’s daily or per-transaction limit may be reached. Check your limit rules or try IMPS if the amount is higher.

- Network or Server-Related Problems: Payments may be interrupted by poor connectivity or outages. After a little wait, switch to a reliable network or try again.

Wrapping Up

UPI and IMPS both handle money transfers securely and in real time, but each serves a different purpose. UPI is ideal for small, frequent payments you want to complete quickly, while IMPS is better for higher-value transfers or when you prefer your bank’s traditional channels.

Some financial needs go beyond everyday transfers. When you need funds for larger goals or unexpected expenses, a personal loan can offer support that payment platforms cannot.

With Hero FinCorp, you can explore personal loan options through a simple digital process, helping you manage such situations with greater flexibility and confidence. So why wait? Explore available personal loan solutions and plan your finances with ease!

Frequently Asked Questions

Can UPI transactions fail due to bank server downtime?

Yes. If the issuing or receiving bank’s server is down, the payment may not go through. Trying again later usually resolves it.

Is IMPS safe for large transfers?

Yes. IMPS uses secure bank infrastructure and is considered safe for high-value transfers.

Are UPI transactions free across all apps?

Most UPI payments between individuals don’t cost anything, but a few banks charge for certain types of transactions.

Can IMPS work with multiple linked bank accounts?

Yes, as long as each account is activated for IMPS in your banking app.

What happens if IFSC is entered incorrectly in IMPS?

The transfer will fail because the system cannot route the payment. Always verify account details.

How long does a UPI refund take after a failed transaction?

Most of the time, the money comes back within a day or two, though there are occasions when it takes a few days.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

The Unified Payments Interface (UPI) has transformed the way India transacts, making digital payments faster, simpler, and more accessible than ever.

A decade ago, if someone said cash payments would have a serious rival, no one would’ve believed it. But today, that’s a reality.

For daily necessities like shopping, bill payments, subscriptions, and EMI repayments, people in India rely on a variety of payment methods. With the widespread acceptance of cards, wallets, and UPI apps, digital payments have become commonplace.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.