Does Checking Your Credit Score Lower It?

Most of us look at our credit score the moment we think of applying for a loan. It feels like the “first checkpoint” before any financial move.

But here’s where confusion kicks in: Does a credit check reduce a credit score? Does checking it too often make it fall? These doubts are common. And today we’ll clear them up in simple, friendly language so you can manage your credit with confidence.

Types of Credit Checks: Soft Inquiry vs Hard Inquiry

First, we need to understand the two kinds of credit checks.

A soft inquiry is a harmless glance at your own credit score. You can check it online, through apps, or through bureau websites, and it won't hurt your score at all. Even lenders sometimes run soft checks to pre-approve offers. These checks never affect creditworthiness.

A hard inquiry, on the other hand, is what happens when you apply for a loan or credit card. The lender pulls your complete report to decide whether to approve you. Because this signals borrowing intent, multiple hard checks in a short time can slightly reduce your score.

Here's a quick comparison of the two-

Parameter | Soft Inquiry | Hard Inquiry |

Impact on Score | No impact at all | May temporarily reduce score |

Who Does It? | You, apps, banks for pre-approved checks | Banks/NBFCs, when you apply for credit |

Visible to Lenders? | No | Yes |

Also Read: Experian Credit Score: The Ultimate Guide to Checking & Improving Your Score

Does Checking Your Credit Score Lower Your Credit Score?

Well, the answer is a firm no. No, checking your own credit score does NOT lower it. Self-checks are always recorded as a soft inquiry and have zero impact on your score. But the story changes when it's a hard inquiry.

Let's take a simple example: If you check your CIBIL score today and again tomorrow, nothing changes. But if you apply for three loans in a week, lenders will pull hard inquiries. That's when scores may dip slightly.

In fact, credit bureaus encourage you to check your score regularly. Following this advice may help you spot errors, detect fraud early, and track your credit health. It's good financial hygiene.

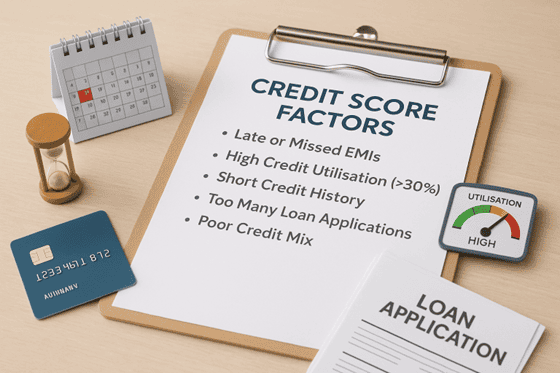

Other Factors That Can Lower Your Credit Score

If checking your credit score does not lower it, then what does? Here's a list of the common culprits -

- Late or missed EMIs

- High credit utilisation (>30%)

- Short or limited credit history

- Too many loan applications

- Poor credit mix

These are the real areas to watch, and not how often you check your score.

Also Read - Common Reasons Personal Loan Applications Are Rejected for Salaried Individuals

How Often Should You Check Your Credit Score?

Checking your CIBIL score will not reduce your score, so you can check it whenever required. Ideally, check it once a month. It keeps you aware, helps you track improvements, and alerts you to suspicious activity.

Regular monitoring is especially helpful if -

- You're planning a major loan (home, car, personal).

- You want to maintain a healthy credit profile.

- You want to catch reporting errors early.

Think of it like checking your weight. The act of checking doesn't change anything. However, it helps you take action in time.

Also Read - How to Increase CIBIL Score: Smart Tips to Improve Your Creditworthiness!

Keep Your Score Healthy, Keep Your Options Open

Credit scores matter, and understanding them gives you an edge. Soft checks don't harm your score. But following good habits does strengthen it. And when you're ready for your next loan, your score helps unlock better rates, faster approvals, and smoother borrowing.

Checked your credit score and planning your next financial move? Hero FinCorp offers easy, fast personal loans for borrowers with solid credit health. Enjoy a fully digital journey, minimal paperwork, and fair interest rates.

Apply for a personal loan today and move forward with confidence.

Frequently Asked Questions

1. Do pre-approved loan checks affect my score?

No. Pre-approved offers involve soft checks.

2. How long do hard inquiries stay on my report?

Usually up to 24 months.

3. Can I dispute a credit inquiry I didn't authorise?

Yes. You can raise a dispute directly with the credit bureau.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.