The Future of Central Bank Digital Currencies (CBDCs) in Everyday Banking

Money has continually evolved from coins to notes and from cheques to mobile wallets.

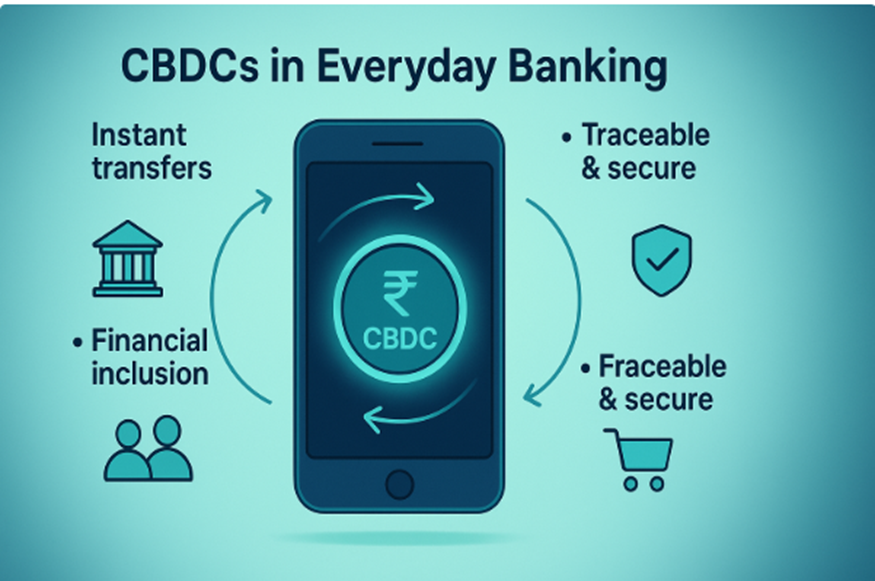

CBDCs are a new form of digital money issued by central banks, such as the Reserve Bank of India, and accessible directly on your mobile phone, similar to UPI or digital wallets.

Unlike other digital currencies, they carry the full credibility and backing of the central bank. For individuals, financial stability, security, and predictability are paramount. CBDCs represent the next step toward safe, traceable, and efficient money for everyday use. But how significant will they be for your daily banking? Let us explore.

What Are Central Bank Digital Currencies?

Central Bank Digital Currencies are digital money issued by the central bank. CBDCs are not like internet-based currencies such as Bitcoin, but they are regulated monies backed by the government, and designed to be secure and feasible.

CBDCs are purely digital, in a tokenised form that you can hold in a wallet on your phone. The RBI is testing CBDCs for the general public (retail) and financial institutions (wholesale).

With a CBDC wallet in your mobile phone, you won’t feel the need to withdraw physical cash. All daily transactions can be recorded immediately and securely. The purpose of CBDCs is to offer the convenience of digital payments and ensure the security of RBI assurances.

How CBDCs Can Transform Daily Banking

For anyone who prefers predictability and control, this is how CBDCs could benefit day-to-day life:

• Faster Payments: You can pay easily without worrying about security or compliance irregularities.

• Low Friction: Fewer integrations with third-party apps, you get the benefit of simpler bill pays like school charges, rents, or EMIs.

• Enhanced Reach: Offline e₹ is already in the works, so small payments could work even with low connectivity. This attribute is convenient on the go or during network failures.

• Specific Applications: "Programmable" payments, for example, time-limited or purpose-specific transfers, can also be used in the case of benefits or rebates.

• Safety Protocols: It's central-bank money, which is beneficial to have around in times when transparency and trust are crucial.

Are CBDCs the Money of the Future?

CBDCs are a practical step towards a transparent and efficient monetary system.

Globally, central banks are moving from experiments to tests. 91% of the BIS-surveyed central banks are investigating CBDCs in some form. That suggests the increasing momentum of CBDC, which is important for:

Usage and Scale

RBI’s annual report indicates e₹ in circulation rose from ₹234 crore in March 2024 to about ₹1,016 crore in March 2025, alongside millions of users and more participating banks.

New Horizons

The RBI has shown interest in cross-border pilots, which could eventually make sending money abroad simpler and more predictable.

CBDCs are following worldwide design lessons with offline person-to-person and peer-to-merchant use cases. This is education on what digital cash needs to be - fast, comforting, and resilient.

Security and Risk Management in CBDCs

Every new device comes with security compliances. Remember the following points in case of CBDCs:

Privacy

People want the ease of digital with the privacy of cash. CBDC architectures show greater anonymity for small offline payments and audit trails for bigger ones. So normal life is business as usual, while larger flows are accountable.

Cyber Resilience

Since CBDCs are electronic, robust security and reliable backup plans are essential. Additionally, continuous monitoring and regular updates are required to protect against evolving cyber threats and ensure system integrity.

Adoption Curve

India already has great real-time payments. A CBDC must feel fundamentally different, with attributes such as offline usage, new capabilities, or some benefit that will keep it in your wallet long term.

Consumer Protection

Simple wallet recovery, clear dispute processes, and easy access to assistance are just as critical as the technology and are clearly acknowledged by CBDCs.

On this note, with Hero FinCorp's instant loan app, managing your finances becomes even easier. Apply in minutes and manage your finances seamlessly alongside emerging tools like CBDCs!

Current Challenges and the Road Ahead

There is no rush to go live!

RBI has been adamant in making the CBDC process an incremental process. The priority is to gain trust, show evidence, ensure safety and security, and not publicity.

• Gradual Rollout: To broaden access, non-bank players have been brought into the pilot along with offline and programmability aspects. This makes the channel wider but not weaker.

• Real-World Integrations: Early CBDC partnerships in India’s payments ecosystem are small but meaningful steps toward broader adoption.

• Building Daily Habits: Just as UPI required time to become mainstream, CBDCs will gradually integrate into daily routines.

Conclusion

If you're planning to take an online personal loan from a quick loan app, or if you are already dealing with EMIs, you need a simple and concrete method of making payments.

CBDCs are primarily focused on facilitating day-to-day payments, offering more convenient benefits, and enabling rebate flows. That's how CBDCs can make your day easier behind the scenes.

When you actually need funds for pre-scheduled milestones or emergency expenses, you can keep your options open.

Check your loan eligibility in minutes through Hero FinCorp's personal loan app. Let the futuristic scope of CBDCs handle finances wisely for you, whether for paying dues, EMIs, or making everyday payments!

Frequently Asked Questions

1. Will CBDCs change the manner in which I repay EMIs?

Not really. Your EMI cycle does not change. What can improve is the speed and certainty of debit, especially if offline and scheduled functionality goes mainstream.

2. Do CBDCs stand a chance of enabling international remittances?

That is the intention. The RBI has signalled cross-border payments as a follow-up step. If successful, this would reduce friction and expense over time.

3. Is the e₹ substituting UPI?

No. CBDC and UPI nowadays serve distinct purposes. UPI is a robust payment vehicle, while the e₹ is a bank-issued digital currency. CBDC offers unique value, such as offline or targeted transfers.

Disclaimer: This guide is intended to provide information and should not be assumed as a financial advisory.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented Here is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.