What is a Digital Wallet? Types, Examples & How to Use It?

- What is a Digital Wallet?

- Types of Digital Wallets Explained

- Benefits of a Digital Wallet

- How Does a Digital Wallet Work?

- What are the Technologies Used by Digital Wallets?

- Popular Digital Wallet Examples in India

- How to Use a Digital Wallet Safely

- Go Digital for Quick and Easy Payments

- Conclusion

- Frequently Asked Questions

A few years back, leaving home meant checking for your wallet first. Cash, bank cards, faded receipts, maybe a few coins rattling around. Now, many of those payments happen through a phone without much thought. Tap at the kirana store, scan to pay the cab driver, and settle a bill while standing in line. Digital wallets have slipped into everyday life across India.

Still, the idea feels fuzzy for a lot of people. What actually sits inside a digital wallet? How safe is it? And with so many apps around, how do you pick one? It’s normal to adopt digital wallets first and learn about them later.

This overview aims to clear things up by covering what they are, the different categories, popular options in India, and how to use them securely.

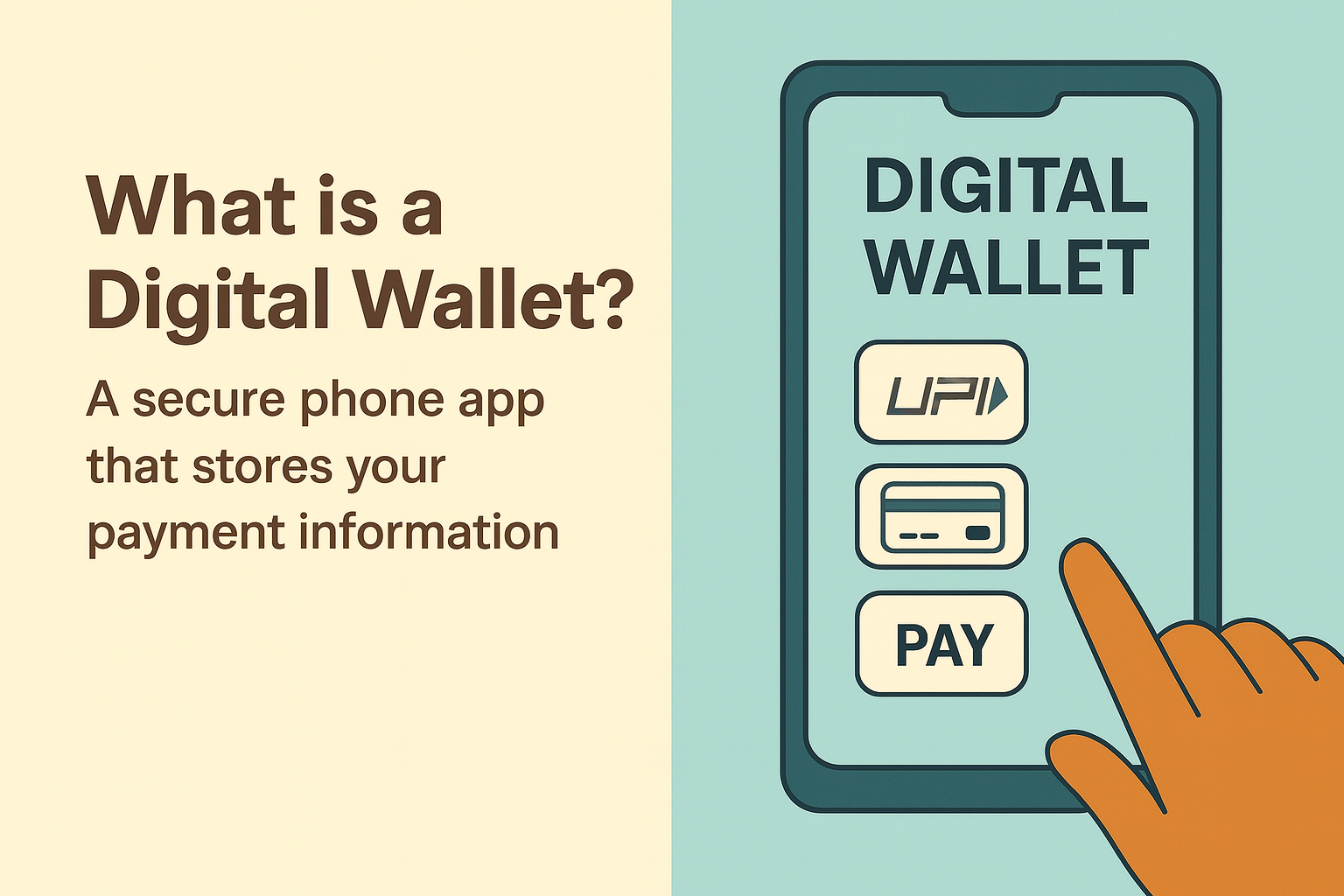

What is a Digital Wallet?

A digital wallet is a protected app or online service that keeps your payment information in one place, including UPI and bank cards. You can use it to pay bills, shop, or send money simply by scanning or tapping your phone.

Across India, digital wallets have expanded rapidly due to UPI, low-cost mobile data, and payment systems regulated by the RBI. For NBFCs, digital wallets support faster loan repayments, quicker disbursals, and easier customer communication.

Also Read: UPI Tap and Pay: The Future of Contactless Payments in India

Types of Digital Wallets Explained

Digital wallets in India are grouped into three main categories, based on how they can be used.

1. Closed Digital Wallets

A single business offers a closed digital wallet and works only on its own app or website. The balance can be used to pay for that company’s products or services, and any refund goes back into the same wallet.

In India, Amazon Pay balance and Ola Money are well-known examples. Closed wallets are useful for customers who regularly buy from the same brand and prefer a simple way to pay without entering card or bank details each time.

2. Semi-Closed Digital Wallets

Semi-closed wallets sit somewhere between brand-only wallets and full banking apps. The money in them can be used at partner outlets, both online and offline. This makes them useful for routine purchases like bill payments, recharges, or a QR payment at a local chemist.

The RBI monitors how these wallets function, and verified KYC users can hold more funds. Many people use options like Paytm Wallet, PhonePe Wallet, Mobikwik, and Freecharge.

3. Open Digital Wallets

Banks and approved financial providers issue open wallets, which support the most flexible payment options. Since they link directly to a regular bank account, users get easier fund access and stronger protection.

RBI approval is required to run these wallets. In India, ICICI Pockets fits this category.

Here's a quick table for your reference:

| Wallet Type | Where It Works | Cash Withdrawal | Common Examples |

|---|---|---|---|

| Closed | One platform | No | Amazon Pay |

| Semi-Closed | Partner stores | No | Paytm, PhonePe, Mobikwik |

| Open | Any merchant or ATM | Yes | ICICI Pockets |

Benefits of a Digital Wallet

Benefits of digital wallets include faster payments and simpler money management in daily life. From shopping and bill payments to ticket bookings and money transfers, digital wallets simplify everyday financial activities.

- Quick Payments: Users can pay instantly through QR codes, mobile numbers, or contactless tap-based systems without carrying cash.

- Better Convenience: Multiple payment methods, cards, and bank accounts can be stored in one application for easier access.

- Enhanced Security: Features like PINs, biometric authentication, OTPs, and encrypted transactions help protect financial information.

- 24/7 Accessibility: Payments, recharges, and transfers can happen anytime without depending on banking hours.

- Useful for Small Businesses: Shopkeepers and local vendors can accept digital wallet payments easily without expensive payment infrastructure.

- Supports Financial Inclusion: Digital wallets help underserved users access digital payments using smartphones and simplified onboarding processes.

- Faster Everyday Transactions: Food delivery, cab bookings, online shopping, and utility bill payments become quicker and more seamless.

- Reduced Cash Dependency: The growing use of digital wallets is encouraging safer and more organised money management across India.

Also Read: Call Money vs Notice Money: Key Concepts and Differences

How Does a Digital Wallet Work?

A digital wallet is an application that securely stores your payment and personal information within a centralised mobile platform

- Linking: Users first link their bank accounts, debit cards, or credit cards to the wallet application.

- Encryption: When making a payment, the wallet encrypts the transaction details and generates a secure authentication code to protect sensitive financial data.

- Verification: It verifies the user through mandatory security checkpoints such as PINs, OTPs, passwords, or biometric authentication.

- Processing: Once approved, the payment is processed through integrated payment gateways, allowing faster digital wallet transactions without repeatedly entering banking details.

What are the Technologies Used by Digital Wallets?

Digital wallets rely on several technologies to process secure, fast, and contactless payments across devices and merchant systems.

- Near Field Communication (NFC): Enables secure "tap-and-pay" transactions by allowing smartphones or smartwatches to communicate over very short distances with contactless POS terminals.

- Quick Response (QR) Codes: Allows users to initiate instant data transfers and payments simply by scanning a two-dimensional matrix barcode using their smartphone camera.

- Bluetooth & Wi-Fi: Helps digital wallet and mobile systems establish stable connections with merchant payment gateways and banking networks.

- Encryption and Tokenisation: Protects core card and banking data by converting sensitive financial details into secure, randomized digital codes (tokens) during live transactions.

Popular Digital Wallet Examples in India

India has many reliable digital wallet options, each offering its own mix of features and payment support.

1. Paytm Wallet

One of the earliest and most widely used wallets in the country. It supports recharges, bill payments, shopping, ticket bookings, and QR payments at lakhs of stores. Paytm Wallet follows RBI rules for prepaid instruments, with KYC needed for higher limits.

2. Google Pay

Built on UPI and linked directly to bank accounts. It enables instant transfers, bill payments, online shopping, and merchant QR payments. Security includes device lock, UPI PIN, and fraud checks.

3. PhonePe

A popular UPI app used for everyday payments, insurance, recharges, and store purchases. It operates under NPCI and RBI guidelines and uses multiple security layers.

4. BHIM UPI

Created by NPCI to make UPI payments simple and accessible across banks. It supports QR payments and fund transfers and offers regional language options.

5. Amazon Pay

Integrated into Amazon for easy checkout, bill payments, rewards, and partner merchant transactions. It works as an RBI-approved prepaid payment instrument.

How to Use a Digital Wallet Safely

Digital wallets save time, but using them wisely keeps your money protected.

- Make sure your phone is locked and set a UPI PIN that isn’t obvious. Keep OTPs and passwords private.

- Run app updates whenever they’re available to keep security tight.

- Scan QR codes from known merchants and install wallets from recognised platforms.

- Enable SMS or push notifications so you know about every payment. Some people prefer adding a daily transaction limit for peace of mind.

- Choose mobile data or a private Wi-Fi connection when paying, rather than shared networks.

- Follow RBI-approved KYC steps to improve account safety.

- Report a lost phone or unknown transaction as soon as you notice it.

Choose official lender apps for EMI payments and loan-related digital transactions. You can apply for a personal loan and manage repayments securely through the Hero FinCorp personal loan app for Android and iOS.

Also Read: Are UPI PIN and ATM PIN the Same?

Go Digital for Quick and Easy Payments

Across India, digital wallets are now a normal part of daily payments, whether you’re shopping, paying bills, or sending money to someone. They reduce the need for cash, speed up checkouts, and follow RBI rules that keep transactions secure.

They also help borrowers manage EMIs without stress. Tracking and paying loans becomes much easier, especially when the lender is a reliable NBFC. If you’re planning a purchase or need quick financial support, Hero FinCorp can help.

Explore Hero FinCorp's personal loans and use the personal loan eligibility calculator today.

Conclusion

Digital wallets continue to reshape everyday financial habits by making payments quicker, safer, and easier to manage. From shopping and bill payments to EMI tracking and fund transfers, they support seamless digital transactions across India. As adoption grows, using trusted and RBI-regulated wallet platforms remains important for maintaining convenience, security, and financial control.

While digital wallets offer a fast and convenient payment experience, users should also understand the disadvantages of digital wallets, such as device dependency and fraud risks without proper security practices.

Frequently Asked Questions

Can I use multiple digital wallets on one smartphone?

Yes. Plenty of people keep a couple of wallet apps on the same phone, as long as their device supports them.

Are digital wallets safe to use for large transactions?

They are generally fine when you use trusted apps, check who you’re paying, and don’t share your UPI PIN. RBI limits still apply.

What should I do if my phone with a digital wallet is lost or stolen?

Stop the SIM, update your UPI PINs, and alert the wallet service.

How are digital wallets regulated in India?

They fall under RBI regulations, and UPI runs through NPCI with rules for identity checks, security, and consumer safety.

Can I link my NBFC loan or credit account to a digital wallet?

Many NBFCs allow repayments through UPI or supported wallet apps, depending on their payment partners.

What happens if my digital wallet provider shuts down?

RBI guidelines require the provider to return the remaining balance to your bank account or offer withdrawal options.

Do digital wallets work without internet connectivity?

Most wallets need data, but UPI 123Pay and USSD still function on basic networks.

How do digital wallets benefit small businesses in India?

They support quick QR payments, reduce cash handling, improve record keeping, and help reach more customers.

What are the main components of a digital wallet?

A digital wallet mainly includes software infrastructure, encrypted payment data, authentication systems, and linked banking or card information.

How are digital wallet transactions processed?

Transactions are processed through encrypted payment gateways, authentication checks, banking networks, and merchant systems for secure fund transfers.

Are digital wallets secure for online payments?

Yes, digital wallets use encryption, OTPs, biometric verification, tokenisation, and PIN-based authentication to improve payment security.

Can digital wallets work without internet access?

Some digital wallets support limited offline payments through NFC or stored credentials, but most features require internet connectivity.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.