ATM Withdrawal Limit in India: Daily, Bank-wise & New Rules

- What is the ATM Withdrawal Limit?

- Types of ATM Withdrawal Limits in India

- ATM Withdrawal Charges & Free Transaction Limits

- RBI Rules for ATM Withdrawal Limits

- Factors Affecting ATM Withdrawal Limit

- ATM Cash Withdrawal Limit vs Online Transfer Limits

- Tips to Manage ATM Withdrawal Limits Efficiently

- Manage your ATM Withdrawals with Confidence

- Frequently Asked Questions

Have you ever been to an ATM to withdraw cash, only to see your request declined?

It can be a frustrating experience and usually comes down to withdrawal limits you didn’t know about.

In India, ATM withdrawal limits aren’t one-size-fits-all and can vary based on bank, card type, and even recent RBI updates.

Having a clear understanding of these limits can help you avoid unnecessary fees, failed transactions, and sudden cash shortages.

Keep reading to know more about ATM withdrawal limits in India.

What is the ATM Withdrawal Limit?

The ATM withdrawal limit refers to the total amount of money that you can withdraw from an ATM within a day, a month or in a single transaction.

These main aim of setting these limits is to ensure easy availability of cash for users, reducing the risk of fraud, and compliance with banking regulations.

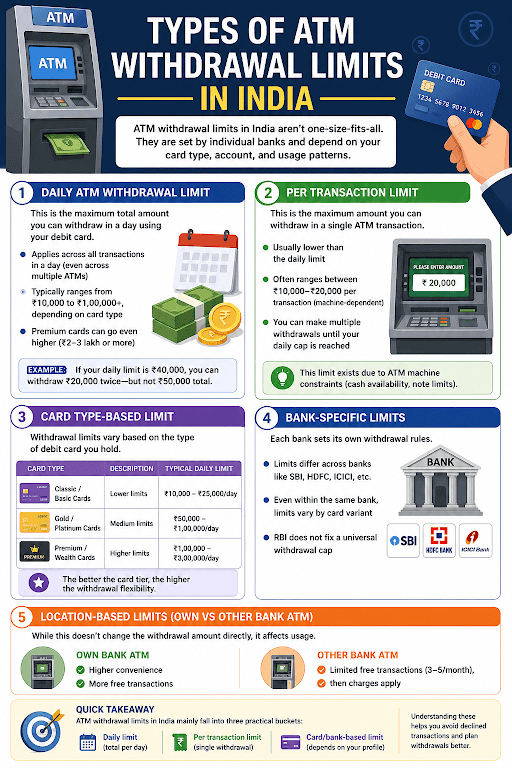

Types of ATM Withdrawal Limits in India

ATM withdrawal limits in India are designed across multiple levels to control cash flow and enhance security. These limits are discussed below-

a. Daily ATM Withdrawal Limit

The daily ATM withdrawal limit is the maximum amount you can withdraw within 24 hours. It usually ranges from ₹20,000 to ₹1,00,000, depending on your bank and card type.

b. Per Transaction Limit

The per-transaction limit is the total amount you can withdraw in a single attempt or transaction. This is often capped between ₹10,000 and ₹25,000.

This restriction is influenced by ATM capacity, denomination availability, and security settings.

For instance, if the per-transaction limit is ₹10,000 and your daily limit is ₹30,000, you’ll need three separate transactions to withdraw the full amount.

ATM Withdrawal Charges & Free Transaction Limits

The Reserve Bank of India regulates ATM withdrawal charges and free transaction limits in India.

Customers can do a maximum of 5 free transactions per month (financial and non-financial combined) at their own bank’s ATMs. Whereas, at other bank ATMs, users typically get 3–5 free transactions, depending on the city.

Once the free limit to withdraw cash from an ATM is exceeded, banks charge up to ₹21 per transaction, plus applicable taxes. These charges apply to both cash withdrawals and balance inquiries.

RBI Rules for ATM Withdrawal Limits

The Reserve Bank of India sets a broad set of rules for ATM withdrawals in India, such as-

- Banks must offer a minimum number of free ATM transactions per month (usually 5 at their own bank ATMs and limited at others).

- Charges apply beyond the above-mentioned limit, capped per transaction.

- While RBI doesn’t fix a uniform daily withdrawal cap, it directs banks to set transparent limits based on account type and security.

- Customers must be informed of fees, limits, and any changes clearly.

Factors Affecting ATM Withdrawal Limit

Multiple factors influence the ATM withdrawal limits in India under guidelines from the Reserve Bank of India. Among these are-

- Account type- Premium or salary accounts generally have higher limits than basic savings accounts.

- Debit card variants (classic, gold, platinum)- Banks define internal policies based on risk management, customer profile, and usage patterns of these variants.

- Location and ATM type- ATM withdrawal limits may differ for on-site vs. off-site ATMs or metro vs. non-metro areas.

ATM Cash Withdrawal Limit vs Online Transfer Limits

ATM withdrawal limits are typically lower and have several restrictions than online transfer limits. Depending on the type of account and card, most banks in India cap ATM cash withdrawals at ₹20,000–₹50,000 per day.

![]()

On the other hand, digital modes offer higher flexibility where UPI transactions can go up to ₹1 lakh per day, while IMPS usually allows up to ₹5 lakh per transaction. NEFT has no fixed upper limit, which makes it suitable for large transfers.

Also Read: NEFT vs. RTGS vs. IMPS vs. UPI: Key Differences

Tips to Manage ATM Withdrawal Limits Efficiently

Managing ATM withdrawal limits smartly can help you avoid unnecessary fees and stay in control of your cash flow.

Here are some of the ways to manage your limits efficiently-

- Know your bank’s daily withdrawal cap and free transaction limit.

- Plan ATM withdrawals in fewer, larger amounts instead of multiple small ones to reduce charges.

- Use your bank’s own ATMs whenever possible, as other bank ATMs may have stricter limits and extra fees.

- Combine ATM usage with digital payments like UPI to reduce dependency on cash.

Manage your ATM Withdrawals with Confidence

Understanding ATM withdrawal limits puts you back in control of your money. Whether it’s planning your daily cash needs or avoiding extra charges, a little awareness goes a long way.

And when your financial needs go beyond ATM withdrawals, having a reliable partner matters.

With flexible solutions and quick access to funds, the Hero FinCorp personal loan app can help you bridge the gap.

Contact us to know more about your personal loan eligibility.

Frequently Asked Questions

1. What is the daily ATM withdrawal limit in India?

The daily ATM withdrawal limit in India ranges from ₹20,000 to ₹1,00,000 per day.

2. How many ATM transactions are free per month?

There are 5 ATM transactions that users get free per month.

3. What happens if I exceed the ATM withdrawal limit?

If you exceed the ATM withdrawal limit, the machine will decline the transaction, return your card and dispense no cash.

4. Can I increase my ATM withdrawal limit?

Yes, you can increase your ATM withdrawal limit, either temporarily or permanently, by contacting your bank.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Missing an EMI payment can happen for many reasons, like a sudden expense, a delayed salary, simply forgetting a due date, etc. But when a repayment is not made on time, it may become an overdue loan.

A lot of borrowers hear "your loan has been written off" and assume the debt is gone. It is not.

A cancelled cheque is a common tool used in daily financial and banking processes.

It is required while applying for a loan, starting an SIP, and on several other occasions. It is an ordinary cheque, which is marked so it can’t be used for any payment.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.