TransUnion CIBIL Report: Check Your CIBIL Score for Free

- What is TransUnion CIBIL?

- What is a TransUnion CIBIL Report?

- Key Components of a CIBIL Report

- How to Check TransUnion CIBIL Score for Free?

- Eligibility to Get a Free TransUnion CIBIL Report

- Why Your CIBIL Score Matters?

- Factors Affecting Your TransUnion CIBIL Score

- How to Improve Your CIBIL Score?

- Common Errors in CIBIL Report & How to Fix Them

- Difference Between CIBIL Score and Other Credit Scores

- Understand Your Report Before It Matters

- Frequently Asked Questions

Rahul went into the loan process assuming things would move smoothly. He was consistently on time with every EMI, and his credit score was 742. However, his loan application was rejected, leaving him in shock.

The real explanation usually sits deeper in the report, not in the score that most people focus on. Many borrowers ignore this until a situation like this forces them to look closer. This blog walks you through how to read a TransUnion CIBIL report and understand what lenders actually pay attention to before making a decision.

![]()

What is TransUnion CIBIL?

TransUnion CIBIL collects credit data from banks and financial institutions across India. Every loan you take, and every repayment you make, becomes part of this record.

Over time, this builds your credit profile. Lenders look at this profile when you apply for credit. A clean track record makes their decision easier. Gaps or delays make them pause.

What is a TransUnion CIBIL Report?

A TransUnion credit report is a detailed record of your borrowing history. It shows how you have handled credit, not just where you stand today.

The score gives a quick idea. The report explains the “why” behind that number. That is what lenders really focus on before approving anything.

Also Read: How to Check CIBIL Score Online Without PAN Card

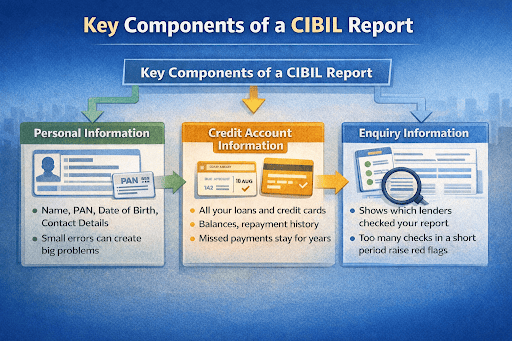

Key Components of a CIBIL Report

The report may look long when you open it for the first time. Once you know what each section means, it becomes much easier to follow.

Personal Information Section

This part covers your name, PAN, date of birth, and contact details. It sounds basic, but errors here are more common than people expect. Even a small mismatch can create unnecessary complications.

Credit Account Information

This part shows all your loans and credit cards. It includes balances, repayment status, and account history. A steady pattern of on-time payments works in your favor. Missed payments stay visible for a long time.

Enquiry Information

Every time you apply for a loan or credit card, lenders check your report. These checks appear here. A few are normal, but too many in a short period can make it look like you depend heavily on credit.

Also Read: Credit Exposure Meaning Explained for Borrowers

How to Check TransUnion CIBIL Score for Free?

Checking your report is simpler than most people expect.

Step 1: Visit the official website of TransUnion CIBIL

Step 2: Enter your basic details like PAN and mobile number

Step 3: Complete the verification process

Step 4: View your report from your account dashboard

You get one free report every year.

Eligibility to Get a Free TransUnion CIBIL Report

Most people can access their CIBIL report without much effort.

- You need to be an Indian resident

- You must have valid identity details

- One free report is available each year

- Additional access may involve a fee

Also Read: How to Check CIBIL Score Online Without PAN Card

Why Your CIBIL Score Matters?

Your CIBIL score matters when you actually need credit, not before. The moment you apply for a loan or a credit card, lenders check it to understand how you have handled repayments so far, because that tells them more than your income alone.

If the score looks strong, things usually move smoothly, and the terms feel reasonable. When the score is on the lower side, the same application may take longer or return conditions that do not work in your favor, even if everything else seems fine on the surface.

Factors Affecting Your TransUnion CIBIL Score

Your score reflects how you manage credit over time. It does not change randomly.

Payment History

Regular payments build trust. Even a single delay can affect your score and stay on your record for a while.

Credit Utilization Ratio

This shows how much credit you use compared to what is available.

Credit limit = 1,00,000

Used amount = 40,000

Utilization = 40%

Lower usage usually helps maintain a stable score.

Credit Mix & Tenure

Having different types of credit shows balanced usage. A longer credit history also gives lenders more context to understand your behavior.

How to Improve Your CIBIL Score?

Improving your score comes down to consistent habits.

- Pay all dues on time

- Keep credit usage under control

- Avoid applying for multiple loans together

- Review your report regularly

Common Errors in CIBIL Report & How to Fix Them

Sometimes the issue is not your behavior but incorrect information.

- Wrong personal details

- Closed loans are still marked as active

- Duplicate account entries

You can raise a dispute through the official portal. Submit proof, clearly explain the issue, and track the request until it is resolved.

Difference Between CIBIL Score and Other Credit Scores

India has multiple credit bureaus, each with its own system.

| Bureau | Score Range | Key Difference |

|---|---|---|

| CIBIL | 300 to 900 | Most commonly used |

| Experian | 300 to 900 | Global database |

| Equifax | 300 to 900 | Strong analytics |

| CRIF High Mark | 300 to 900 | Expanding coverage |

Even though all scores matter, CIBIL remains the one lenders check most often.

Understand Your Report Before It Matters

Most people open their report only after a rejection forces them to look closer. By then, the focus shifts to fixing things quickly instead of understanding what went wrong. Reading it earlier gives you time to spot patterns, correct small errors, and improve your credit profile with clarity.

Hero FinCorp helps you act on that insight. The eligibility calculator shows where you stand and how your CIBIL score fits loan requirements. The personal loan app lets you review your profile and apply here with more confidence.

Frequently Asked Questions

How can I check my CIBIL score for free?

Register on the TransUnion website, complete the verification, and you can get one free report every year.

How many times can I check my CIBIL report for free in India?

You can check it once annually for free. Additional reports may come with a charge.

What is a good CIBIL score for loans?

Most banks feel comfortable when your score is above 725. It tells them you have handled credit well, reducing their risk.

Does checking CIBIL score affect it?

Checking your own score counts as a soft check. Only lender checks during loan applications affect your score, so you are safe here.

How long does it take to improve a CIBIL score?

It usually takes 3-6 months to improve your CIBIL score.

How can I correct errors in my CIBIL report?

You can raise a complaint through the official portal, submit documents, and track the resolution.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Somewhere behind every loan application sits a name most borrowers never bother to ask about. Nine times out of ten it's CRIF, licensed by the Reserve Bank of India alongside just three others. Whatever they report back can be the difference between a quick yes and a frustrating delay, which is reason enough to figure out what CRIF actually is and how it compares to CIBIL.

If you’ve been wondering why my credit score is decreasing, the answer is usually linked to recent changes in how you use credit, repay loans, or how lenders report your activity.

Nobody thinks about their CIBIL score until a loan application is in front of them. By that point, years of high credit card utilisation, a couple of missed EMIs, or just never having borrowed at all have already shaped the number sitting in the bureau's records.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.