What Is A Crossed Cheque?

- What Is The Meaning Of A Crossed Cheque?

- How To Cross a Cheque The Right Way?

- What are The Benefits Of Crossing A Cheque?

- What Are The Key Differences Between A Crossed And Uncrossed Cheque?

- How Does a Crossed Cheque Work?

- Legal Framework Governing Crossed Cheques in India

- Summing It Up

- Frequently Asked Questions

Ever wondered why you still get a cheque book when you open a new bank account in 2026? This is because, even today, they remain a widely used medium for transactions, especially for corporates and businesses, especially when large transactions are involved.

This is primarily due to how safe they are, and one way to do this is to cross a cheque. So, if you want to know more about what a crossed cheque is and how to use them, read on.

What Is The Meaning Of A Crossed Cheque?

A crossed cheque is simply a cheque with two parallel lines in the top left corner. The moment a cheque is crossed, it means that it cannot be encashed directly at the counter. The money has to be deposited into the account instead. This simple action ensures:

- The money goes only to the intended recipient.

- A proper banking trail is created, and as a result, the risk of theft or misuse is reduced.

- Crossed cheques are commonly used for business payments, salary payments, and large transactions where safety and security are of vital importance.

How To Cross a Cheque The Right Way?

The process to cross a cheque is simple:

- Fill in the cheque as you normally would.

- Draw two parallel lines at the top right-hand corner of the cheque, and you are done.

- Optionally, you can add extra wording in between these lines, which will give further instructions to the bank on how to process it.

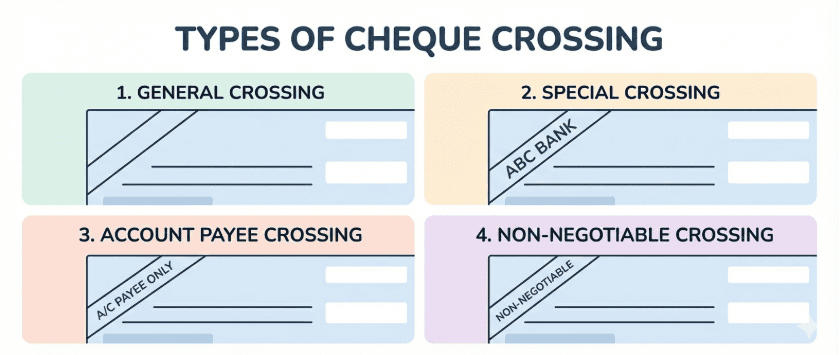

The wording determines the type of crossing and is as follows:

1. General Crossing

It's the most common form, and it simply involves drawing two parallel lines across the top left corner. As mentioned earlier, this means the amount mentioned on the cheque has to be deposited into an account.

2. Special Crossing

Here, you mention the name of a specific bank in between the two parallel lines. When this is done, it means that the cheque in question can only be deposited into an account belonging to the bank mentioned on the cheque.

3. Account Payee Crossing

When you write the letters A/C Payee or Account Payee between the two lines, it becomes an account payee crossing. In this case, the funds can only be deposited into the account of the person or entity mentioned on the cheque. This is one of the safest ways to issue a cheque.

4. Non-negotiable Crossing

A non-negotiable crossing (the words "non-negotiable are written between the parallel lines) means the cheque can still be transferred to someone else, but the recipient doesn't get clean ownership, i.e., be absolved of any risk in case the cheque was initially stolen or misused.

Who Can Cross A Cheque?

The drawer (the person issuing the cheque) is usually the one who crosses a cheque while writing it. However, even the holder of the cheque can add a crossing if it was originally uncrossed. Once crossed, the bank has to follow the instructions mentioned in the crossing.

What are The Benefits Of Crossing A Cheque?

Crossing a cheque immediately unlocks a slew of advantages. It:

- Reduces the chances of fraud.

- Prevents cash withdrawal at counters.

- Creates a record of the transaction.

- Ensures payment reaches the intended recipient.

- Adds a layer of legal protection in case of disputes.

What Are The Key Differences Between A Crossed And Uncrossed Cheque?

The differences between the two forms of cheques are as follows:

| Crossed Cheque | Uncrossed Cheque |

Encashment | Cannot be encashed directly. | Can be encashed over the counter. |

Transaction record | Mandatory | Not always |

Transferability | May be restricted | Easier to transfer |

In short, an uncrossed cheque offers flexibility but carries a higher element of risk. A crossed cheque prioritises safety.

How Does a Crossed Cheque Work?

When a crossed cheque is presented to the bank, the bank verifies the crossing instructions and processes it accordingly. Since there is no direct handover of cash, and the money moves through banking channels, it also creates a clear audit trail.

Legal Framework Governing Crossed Cheques in India

Crossed cheques in India are governed by the Negotiable Instruments Act, 1881. The Act recognises different types of crossings and outlines the responsibilities of banks.

If a bank ignores crossing instructions and allows improper encashment, it can be held liable. This legal backing strengthens the reliability of crossed cheques in financial transactions.

Summing It Up

In a world that's increasingly digital, cheques might seem old-fashioned, but the safeguards built into them are anything but outdated. A small addition like crossing a cheque turns a simple payment instrument into a more controlled and traceable transaction. This tiny detail can make all the difference in securing your money.

The same applies when it comes to managing your broader financial needs. At Hero FinCorp, you can get a personal or a secured loan via a completely secure and transparent process, digitally. Apply via our personal loan app or our dedicated apps for Android or iOS.

Frequently Asked Questions

1. Can a crossed cheque be cashed over the counter?

No. A crossed cheque must be deposited into a bank account.

2. What happens if a check is not crossed?

If a cheque isn't crossed, you can opt to encash it instead of depositing the funds into an account.

3. Is a crossed cheque negotiable?

Yes, unless marked "Account Payee" or "Not Negotiable," which restricts its transferability.

4. Can a crossed cheque be endorsed?

It depends on the type of crossing. Account Payee cheques cannot be transferred.

5. What is the difference between a crossed cheque and a bearer cheque?

A bearer cheque can be encashed by whoever holds it. A crossed cheque must go through a bank account.

6. Can a post-dated cheque be crossed?

Yes. A cheque can be crossed regardless of its date.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.