Overdraft vs Personal Loan: What’s the Difference?

Rajeev was short by ₹12,000 just three days before his salary. Rent had already gone through, and a medical bill showed up at the worst time. His bank app showed an overdraft option, but he also remembered seeing personal loan offers earlier.

One looked quick; the other, structured. He paused because choosing wrong could cost more than he expected. This blog breaks down both options, so you know exactly what works for your situation.

What is Overdraft?

An overdraft lets you use more money than what is in your bank account. The bank sets a limit, and you can dip into it when your balance runs low.

The way interest works here is what really sets it apart. You are not charged the full limit sitting there. You are only charged for the amount you actually use. So if your limit is ₹50,000 and you use ₹8,000, the interest applies only to that ₹8,000. This makes a noticeable difference when you are only covering a short gap.

Repayment also feels less rigid compared to a regular loan. There is no fixed EMI that you have to follow every month. When money is deposited into your account, the used amount starts being adjusted automatically. This is why many people rely on overdraft when something unexpected comes up, and they just need quick support for a few days.

What is a Personal Loan?

A personal loan gives you a fixed amount upfront. Once approved, the full amount is credited to your account, and repayment begins with monthly EMIs.

Before you even accept the loan, you can know everything from the monthly EMI amount to when it will finally end. This benefit of a personal loan helps you plan your expenses properly and keeps you stress-free.

Loan Amount: ₹2,00,000

Interest Rate: 12% per year

Tenure: 24 months

EMI ≈ ₹9,414 per month

Most people choose this when the expense is already decided. It could be a hospital bill, a wedding payment, or clearing a few smaller dues that have been piling up. Many borrowers also prefer using a personal loan app because it clearly shows the EMI, lets you track payments easily, and keeps everything in one place, so you do not have to check multiple sources.

Key Differences Between Overdraft and Personal Loan

The difference becomes clearer when you place both side by side.

| Factor | Overdraft | Personal Loan |

|---|---|---|

| Access | Withdraw as needed | Full amount upfront |

| Interest | Only on the used amount | The entire loan |

| Repayment | Flexible | Fixed EMI |

| Usage | Short-term gaps | Planned expenses |

| Approval | Linked to account | Based on income and score |

| Speed | Instant if available | Takes processing time |

Uses and Benefits

Each option solves a different kind of problem.

- A personal loan works well when you know exactly how much you need

- Fixed EMIs bring discipline and reduce uncertainty

- Overdraft helps when timing is unpredictable

- You borrow only what you need instead of taking excess

- Short-term usage keeps interest under control if managed well

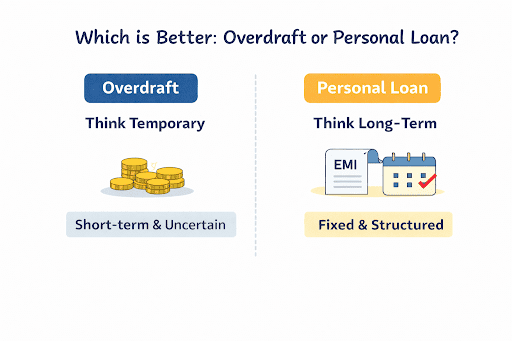

Which is Better: Overdraft or Personal Loan?

Rajeev’s situation makes the answer clear. He needed money for a few days, not for two years. Taking a personal loan would have locked him into fixed EMIs long after the problem ended.

An overdraft would allow him to cover the rent immediately and repay once his salary arrived. That choice keeps costs low and avoids unnecessary commitment.

A personal loan works better when the expense is fixed, and the repayment needs a structure. An overdraft fits better when the need is temporary and uncertain. The right option depends less on the product and more on how long you need the money.

Eligibility and Application Process

Both options look simple from the outside, but approval works differently.

Personal Loan

- Lenders check income stability and credit score

- Documents include identity proof, income proof, and bank statements

- Approval depends on repayment capacity

Overdraft

- Banks look at your account history and transaction behaviour

- Existing relationship improves approval chances

- The limit depends on how your account performs over time

Knowing this upfront saves time and avoids surprises during the application.

Frequently Asked Questions

Is overdraft the same as a personal loan?

No, an overdraft provides flexible access within a limit, while a personal loan provides a fixed amount with a set repayment schedule.

Why is overdraft cheaper than a personal loan?

You pay interest only on the amount used, which can reduce the total cost if usage stays low.

Does overdraft affect credit score?

Yes, missed repayments or overuse can negatively impact your credit profile.

Can I prepay an overdraft or a personal loan?

Overdraft allows repayment at any time, while personal loan prepayment depends on the lender's rules.

What happens if I can’t repay the overdraft?

Banks may apply penalties and report defaults, which affect your credit standing.

Choose Based on What Your Situation Demands

Rajeev chose an overdraft that week because he needed a small amount for a few days. As soon as his salary came in, he cleared it and avoided paying extra interest. A month later, when he planned a bigger expense, he went ahead with a personal loan because fixed EMIs made it easier to manage his monthly budget.

This is how these options are meant to be used. One helps you handle short-term gaps, while the other supports planned expenses with a clear repayment path. Choosing the right lender makes this process much smoother from the beginning.

Hero FinCorp offers personal loans with simple digital access, where you can check eligibility, understand repayment clearly, and manage everything through a reliable Instant loan app without confusion. Apply here.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.