Pre-Qualified vs Pre-Approved Personal Loan: What Every Borrower Should Know

- What is a Pre-Qualified Loan?

- What is a Pre-Approved Loan?

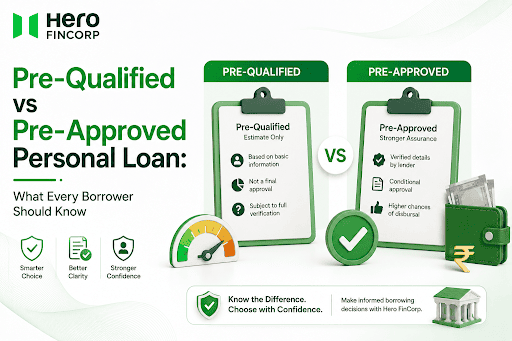

- Pre-Approved vs Pre-Qualified Personal Loan: Key Difference

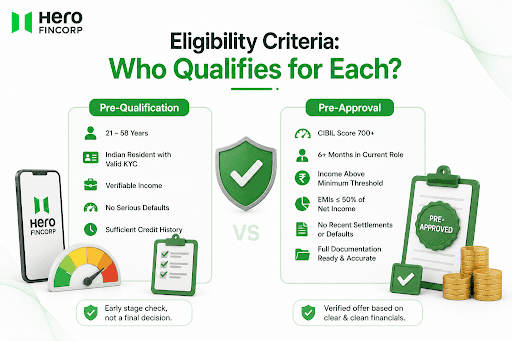

- Eligibility Criteria: Who Qualifies for Each?

- Documents Required for Pre-Qualification vs Pre-Approval

- Pre-Qualified vs Pre-Approved Loan: Which One to Choose?

- How to Get Started with Pre-Approval Process at Hero FinCorp

- Conclusion

- Frequently Asked Questions

Two terms that sound almost identical but represent very different stages of the loan process. Mixing them up costs time, sometimes triggers an unnecessary hard enquiry on the credit report, and occasionally sets up expectations that the final application cannot meet.

The pre-qualified vs pre-approved loan gap is worth understanding before approaching any lender. Both mean a lender has looked at the financial situation and found minimum requirements are met.

Neither one guarantees the loan will actually be sanctioned. What separates them is how deep that review goes.

What is a Pre-Qualified Loan?

Picture the first conversation with a lender before anything formal happens. That is essentially what a pre qualified loan is.

The lender takes basic information, income, employment status, existing debts, and uses it to give a rough estimate of what might be available. No hard check on the credit report. It is an informal, quick process.

What pre-qualification gives the borrower:

- A rough loan amount based on self-reported details

- No credit score impact since the check is soft

- An early read on eligibility before investing time in documents

- The ability to compare multiple lenders without consequence

What it does not give: any firm commitment from the lender's side.

What is a Pre-Approved Loan?

Pre-approval is where things get serious. The lender goes through the full financial history and credit report, runs a hard credit check, and asks for employment verification and income proof.

What a pre approved personal loan actually delivers:

- A specific loan amount with a real interest rate attached

- Much stronger confidence that final approval will come through

- Faster movement when the formal application goes in

- An offer based on verified data rather than a rough calculation

Pre-approved offers come after a hard enquiry. They are more accurate than pre-qualification but that hard pull can marginally affect the credit score.

Also Read: How Does a Personal Loan Impact My Credit Score?

Pre-Approved vs Pre-Qualified Personal Loan: Key Difference

The difference between pre approved and pre qualified loan runs through three things: depth of the review, credit score impact, and how reliable the final number is.

| Factor | Pre-Qualified | Pre-Approved |

| Credit Check | Soft enquiry only, no impact on your credit score | Hard enquiry, may cause a small dip in your credit score |

| Documents | Basic self-reported information | Full income and identity verification |

| Offer Accuracy | Rough estimate of eligibility | Close to the final approved loan amount |

| Speed | Near-instant | Takes a few days |

| Rejection Risk | Higher during the full application process | Considerably lower after verification |

| Best Suited For | Early loan exploration and comparison | Applicants ready to apply for a loan |

Pre-approval carries more weight than pre-qualification. It is a stronger signal that the borrower clears the lender's criteria. Even so, neither one locks in the final loan.

The pre-qualified vs pre-approved personal loan question has a simple answer: pre-qualification is where the journey starts and pre-approval is where it gets real.

Eligibility Criteria: Who Qualifies for Each?

Pre-Qualification Eligibility at Hero FinCorp

The bar for pre-qualification is lower by design. It is an early stage check, not a final decision.

Getting pre-qualified at Hero FinCorp means the lender has reviewed the credit profile at surface level and sees the borrower as a potentially suitable candidate.

Broad requirements:

- Age between 21 and 58 years

- Indian resident with valid KYC documents

- Some verifiable income, salaried or self-employed

- No serious active defaults sitting on the credit report

- Enough credit history for a soft review to draw from

Check your Hero FinCorp personal loan eligibility here without any impact on the credit score.

Pre-Approval Eligibility at Hero FinCorp

Pre-approval needs more. The lender is putting a verified offer on the table, so the financial picture has to be clearer and cleaner.

What typically needs to be in place:

- CIBIL score of 700 or above

- At least six months in the current role for salaried applicants

- Net monthly income above the lender's minimum threshold

- Existing EMIs not eating more than 50% of net monthly income

- No recent loan settlements or defaults on file

- Full documentation ready and accurate across all documents

Reaching pre-approval stage at Hero FinCorp significantly cuts rejection risk because the offer is based on verified numbers rather than estimates.

Documents Required for Pre-Qualification vs Pre-Approval

| Document | Pre-Qualification | Pre-Approval |

| PAN Card | Required | Required |

| Aadhaar Card | Required | Required |

| Salary Slips | Not always needed | Last 3 months |

| Bank Statements | Not required | Last 6 months |

| ITR / Form 16 | Not required | Required for self-employed applicants |

| Employment Proof | Basic details | Formal verification |

| Credit Report | Soft credit check only | Hard credit enquiry |

| Address Proof | Basic proof | Must match all submitted documents |

Pre-Qualified vs Pre-Approved Loan: Which One to Choose?

This depends entirely on where the borrower is in the process and what they actually need right now.

For anyone still in the comparing-options stage, pre-qualification costs nothing and risks nothing. The process is quicker, less involved, and the credit score stays exactly where it is throughout. It is genuinely a no-downside first step

Someone who has already decided to borrow and wants a firm offer before submitting a formal application should go for pre-approval.

The difference between pre approved and pre qualified loan matters most here because the pre-approval number is based on real verified data, not a ballpark.

| Situation | Right Move |

| Still comparing lenders | Pre-Qualification |

| Need the exact loan amount | Pre-Approval |

| Want to protect your credit score | Pre-Qualification |

| Ready to borrow soon | Pre-Approval |

| Need fast loan disbursal | Pre-Approval |

| First-time borrower exploring options | Pre-Qualification |

Download the personal loan app on Google Play to run a soft eligibility check without touching the credit score.

How to Get Started with Pre-Approval Process at Hero FinCorp

The whole thing runs on a phone. No branch visit needed at any point.

- Download the instant loan app from the App Store or visit the Hero FinCorp website directly

- Register with the mobile number linked to the bank account

- Complete e-KYC using Aadhaar OTP and PAN

- Enter employment details, monthly income, and the loan amount needed

- Upload the last three months of salary slips and last six months of bank statements

- Self-employed applicants upload ITR for one to two years alongside bank statements

- The platform assesses the income profile and generates a pre-approval offer with loan amount, rate, and tenure

- Read the Key Facts Statement carefully before accepting, specifically the APR, processing fee, and any applicable charges

- Accept the offer and money moves directly into the bank account per RBI Digital Lending Directions 2025

Hero FinCorp's pre-approval process speeds up the overall loan journey and lowers the chances of rejection because the offer stems from verified financial data.

Conclusion

Pre qualified vs pre approved loan is not a subtle difference. Pre-qualification gives a rough early read with no strings attached.

Pre-qualification is the no-commitment starting point. Pre-approval is where the lender has actually checked the numbers and put something real on the table. Which one makes sense depends entirely on where the borrower is right now and how ready they are to move forward.

Starting with pre-qualification and moving to pre-approval when ready is the practical route for most borrowers. Check your Hero FinCorp personal loan eligibility here and find out which stage applies right now.

Frequently Asked Questions

Can I get a pre-approved loan without a good credit score?

Technically possible but unlikely. Pre-approval involves a hard credit check, and if the score does not clear the lender's minimum threshold, the application does not progress beyond pre-qualification.

How long does a pre-approval last?

Thirty to ninety days with most lenders. If income or debt levels shift significantly during that window, the original offer may no longer hold.

Is pre-qualification free of cost at Hero FinCorp?

Yes. Pre-qualification at Hero FinCorp runs on a soft enquiry with no fee and no credit score impact.

What happens if my financial documents change after pre-approval?

The lender reassesses based on the new documents. Pre-approval reflects the profile at review time. A significant income drop or new debt can change the final approved amount.

Are there any penalties for cancelling a pre-approved loan offer?

None. Accepting a pre-approved offer is the borrower's choice. Declining it carries no penalty, though the hard enquiry from the review stays on the credit report either way.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Flight fares between Delhi and Goa have been known to double in a single week. Spotting a good deal is one thing. Having the full amount sitting in your account on the same day is a different problem entirely.

Seeing a three-digit number flash on your credit report can feel like opening a report card. But when that number reads credit score 777 is it good or bad? In short: it’s not just good, it’s excellent.

Aman had finally started getting regular freelance work. Then his old laptop began shutting down during client meetings. Buying a new one at once meant using all his savings, while waiting meant losing work.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.