Quick Loan vs Express Loan: Key Differences, Features, and How to Choose

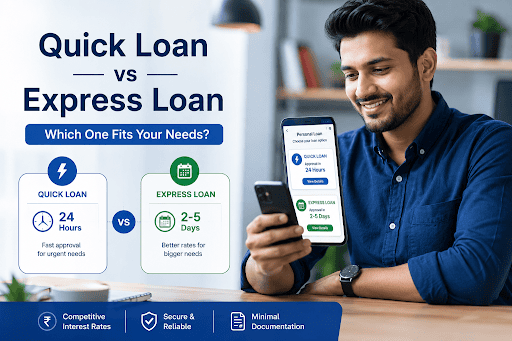

- What Is a Quick Loan?

- Features, Benefits, and Interest Rates of Quick Loans

- What Is an Express Loan?

- Features, Benefits, and Interest Rates of Express Loans

- Key Differences Between a Quick Loan and an Express Loan

- Choosing the Best Option: Use Cases for Quick Loans vs Express Loans

- Conclusion

- Frequently Asked Questions

- Ready to Borrow Fast?

Financial crises do not give prior notice. When you face an unforeseen situation that demands money on the spot, like medical emergencies or any other unplanned expense, two ways to borrow come in handy: quick loans and express loans.

While both are designed for speed, they're not identical. Understanding quick loan vs express loan differences helps you choose the right solution for your situation. This guide breaks down quick loan and express loan features, so you can make an informed decision quickly.

What Is a Quick Loan?

A quick loan is an unsecured personal loan that is paid out very quickly.

When understanding quick loan vs express loan differences, it's important to know what quick loans specifically offer. Quick loans typically offer:

- Approval within 24 hours of application

- Minimal documentation requirements

- Flexible eligibility criteria

- No collateral needed

- You can get loans from ₹5,000 to ₹5 lakhs

Also Read: Quick Cash Loan Apps: What You Must Know Before You Borrow

Features, Benefits, and Interest Rates of Quick Loans

Understanding the features of quick loan vs express loan products helps you decide which suits your needs better. When comparing quick loan and express loan options, knowing their distinct benefits ensures you choose the right fit for your urgency level and financial situation.

Key Features of Quick Loans

- Speed: Funds disbursed within 24–48 hours

- Few documents Needed: Basic proof of identity, income, and bank account

- Credit-flexible: Okay with a score of 600 or more

- Unsecured: No collateral required

- Flexible end-use: Use funds for any purpose

- Interest rates: 12–18% p.a. (competitive for fast lending)

- Tenure: 1–5 years

- Processing fees: 1–3% of loan amount

What Is an Express Loan?

An express loan is another unsecured personal loan category designed for fast processing, but with slightly more rigorous verification than quick loans. When comparing quick loan vs express loan, express loans represent a middle ground between ultra-fast borrowing and standard personal loans.

Express loans typically offer:

- Approval within 2–5 working days

- Moderate documentation requirements

- Stricter credit assessment

- No collateral needed

- The amounts offered can be as low as ₹10,000 to as high as ₹10 lakhs

Features, Benefits, and Interest Rates of Express Loans

Express loans are a distinct option when comparing quick loan vs express loan choices. Understanding the specifics of quick loan and express loan products helps you make an informed decision based on your timeline and financial needs.

Key Features of Express Loans:

- Speed: Funds within 2–5 working days

- Moderate docs: Income proof, bank statements, credit report review

- Credit-important: Higher minimum credit score requirement (650+)

- Unsecured: No collateral needed

- End-use flexibility: Full flexibility on fund usage

- Interest rates: 10–15% p.a. (competitive, often lower than quick loans)

- Tenure: 2–7 years

- Processing fees: 0.5–2% of loan amount

Key Differences Between a Quick Loan and an Express Loan

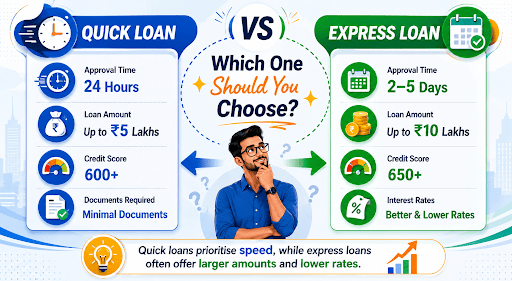

When deciding between borrowing options, understanding quick loan vs express loan distinctions is essential. The table below breaks down the core differences between quick loan and express loan products to help you compare effectively.

| Aspect | Quick Loan | Express Loan |

| Approval Time | 24 hours | 2–5 working days |

| Interest Rate (p.a.) | 12–18% | 10–15% |

| Loan Amount | ₹5,000–₹5 lakhs | ₹10,000–₹10 lakhs |

| Minimum Credit Score | 600+ | 650+ |

| Documentation | Minimal | Moderate |

| Credit Assessment | Quick, basic check | Thorough review |

| Processing Fees | 1–3% | 0.5–2% |

| Repayment Tenure | 1–5 years | 2–7 years |

| Best For | Emergency needs (hours) | Urgent needs (days) |

| Eligibility Criteria | Flexible | Stricter |

Choosing the Best Option: Use Cases for Quick Loans vs Express Loans

When deciding between quick loans and express loans, understanding which best suits your situation is crucial. Here's how to evaluate your needs:

Choose a Quick Loan When:

- You need funds within 24 hours

- Your credit score is below 650

- You want minimal paperwork

- The amount needed is under ₹5 lakhs

- There is a medical or other critical situation (like traveling out-of-country, medical emergency)

Choose an Express Loan When:

- You can wait 2–5 working days

- Your credit score is 650+

- You need a larger loan amount (₹5–₹10 lakhs)

- You want better interest rates

- You prefer a longer repayment tenure

Understanding quick loan vs express loan use cases ensures you pick the right product. Some borrowers might qualify for both but should choose based on urgency and financial capacity.

Conclusion

Quick loan vs express loan - both are valuable tools for financial emergencies. The difference between quick loan and express loan boils down to speed versus better terms. Choose based on how urgently you need funds and your credit profile.

If you are considering applying for a personal loan, remember to decide on your timeline and your eligibility beforehand. Find out if you’re eligible for the personal loan from Hero FinCorp now - we offer affordable rates and speedy processing!

Frequently Asked Questions

Does it take longer to receive money from quick loans than express loans?

Quick loans are faster. When comparing quick loan vs express loan disbursement, quick loans typically disburse within 24 hours, while express loans take 2–5 working days. If speed is your priority in quick loan and express loan comparison, quick loans win.

Do express loans require a higher credit score compared to quick loans?

Yes. Express loans typically require a minimum credit score of 650+, while quick loans accept scores as low as 600+. The difference between quick loan and express loan credit requirements reflects the additional verification in express loans. Both quick loan and express loan products are accessible to most borrowers, but express loans are stricter.

Can I get a quick loan or express loan without formal income proof?

Most lenders require some form of income verification for both. However, quick loans are more flexible - you might provide bank statements or ITR instead of salary slips. Express loans strictly require formal proof. When evaluating quick loan vs express loan, quick loans are easier if you're self-employed or have irregular income.

What are the typical repayment tenures for quick and express loans?

Quick loans offer 1-5 year tenure, while express loans extend to 2–7 years. The difference between quick loan and express loan tenures allows express borrowers to reduce monthly EMI burdens. Both quick loan and express loan options offer flexibility based on your repayment capacity.

Are interest rates generally higher for a quick loan than an express loan?

Yes. Quick loans charge 12–18% p.a., while express loans charge 10–15% p.a. The difference between quick loan and express loan rates reflects verification depth. When choosing quick loan vs express loan, faster approval (quick loans) comes at a higher cost.

Which option should I choose for high-ticket emergency financial needs?

For amounts above ₹5 lakhs, express loans are better suited. They offer higher loan amounts and better rates. However, if you need funds within 24 hours, a quick loan might be your only option. Ideally, understand your timeline before choosing between quick loan and express loan for large amounts.

Ready to Borrow Fast?

Both quick loan and express loan options serve urgent financial needs. The difference between quick loan and express loan depends on your timeline and credit profile. Evaluate your situation and choose wisely.

Looking for personal loan that is both economical in interest rates and flexible in its terms? Check out personal loan schemes from Hero FinCorp and find out how eligible you are in just a minute.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision...

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.