Personal Loan vs Line of Credit: Which Borrowing Option Is Right for You?

- What Is a Personal Loan?

- Advantages and Disadvantages of a Personal Loan

- When Should You Choose a Personal Loan?

- What Is a Personal Line of Credit?

- How Does a Personal Line of Credit Work?

- Common Uses of a Personal Line of Credit

- Advantages and Disadvantages of a Personal Line of Credit

- Personal Loan vs Personal Line of Credit: Detailed Comparison

- Factors to Consider Before Choosing Between a Personal Loan and a Line of Credit

- Personal Loan vs Line of Credit: Which Option Is Better?

- Choose What Works Best for You

- Frequently Asked Questions

Borrowing money is easy. Choosing the right borrowing option is where most people get confused. A personal loan may work well in one situation, while a line of credit may be the better choice in another.

The difference is not always obvious when you apply. This blog breaks it down in simple language, so you know which option fits your needs before you borrow.

What Is a Personal Loan?

A personal loan works well when you know how much money you need before you borrow. The lender approves one amount and transfers it to your bank account. You then repay the loan through fixed monthly EMIs over a fixed period.

How a Personal Loan Works

Once your loan gets approved, you receive the full amount together. Interest starts on the entire loan amount from the day the money reaches your account. Every EMI includes both the principal and the interest until you repay the loan completely.

Common Uses of Personal Loans

People usually take a personal loan for expenses with a fixed cost. These may include weddings, medical treatment, home renovation, higher education, or paying off multiple small loans.

Also Read: Can you Have Multiple Personal Loans?

Advantages and Disadvantages of a Personal Loan

A personal loan gives you a fixed repayment plan from the beginning. At the same time, it may not suit every type of expense.

Advantages

- Fixed EMIs make monthly budgeting easier

- You receive the full loan amount at one time

- The loan ends on a fixed date if you repay on time

Disadvantages

- Interest applies to the full loan amount

- You need a new loan if you need more money later

- Some lenders charge a fee for early repayment

When Should You Choose a Personal Loan?

You should choose a personal loan when you have a fixed expense to manage. For example, if you need ₹5 lakh for your sister's wedding. In this case, you should opt for a personal loan and repay it through fixed monthly EMIs.

What Is a Personal Line of Credit?

Not every expense needs all the money at once. You may use a part of the money today and need more later. A personal line of credit gives you that choice. You borrow only what you need and use the remaining amount whenever you need it.

How Does a Personal Line of Credit Work?

Instead of giving you one lump sum, the lender approves a credit limit. You can withdraw any amount within that limit whenever you need it. As you repay the borrowed amount, the same limit becomes available again.

For example:

Credit limit = ₹3,00,000

You withdraw = ₹80,000

Available balance = ₹2,20,000

You repay = ₹30,000

Available balance = ₹2,50,000

You pay interest only on the amount you borrow, not on the full credit limit.

Common Uses of a Personal Line of Credit

A personal line of credit suits expenses that come over time. This means that you do not know the fixed amount in advance. It might include expenses such as home repairs, medical expenses, and other costs.

Advantages and Disadvantages of a Personal Line of Credit

A line of credit gives you more freedom while borrowing. You should also use it carefully to avoid borrowing more than you need.

Advantages

- You borrow only when you need money.

- Interest applies only to the amount you use.

- You can use the available limit again after repayment.

Disadvantages

- Easy access to money can lead to unnecessary spending.

- Interest rates may change, depending on the lender.

- Poor repayment habits can increase your borrowing cost.

Also Read: Difference Between Borrowing and Lending

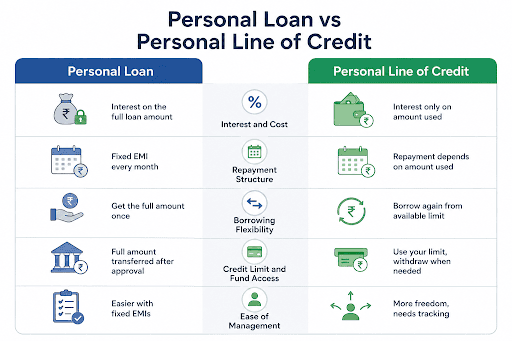

Personal Loan vs Personal Line of Credit: Detailed Comparison

Both options help you borrow money, but they suit different situations. Looking at a few key differences can make your decision much easier.

Interest Rates and Cost of Borrowing

In a personal loan, you have to pay interest on the full loan amount based on the applicable personal loan interest rate. In contrast, with a line of credit, you pay interest only on the amount you actually use.

Repayment Structure

A personal loan usually comes with a fixed EMI every month. A line of credit works differently. Your repayment depends on how much money you use.

Borrowing Flexibility

A personal loan gives you the approved amount only once. If you need more money later, you must apply again. A line of credit lets you borrow again from the available limit after you repay the amount you used.

Credit Limit and Fund Access

A personal loan transfers the full amount to your account after approval. A line of credit gives you a borrowing limit. You can withdraw money from that limit whenever you need it.

Which One Is Easier to Manage?

A personal loan is easier to manage if you like fixed EMIs. A line of credit gives you more freedom, but you need to keep track of how much you borrow.

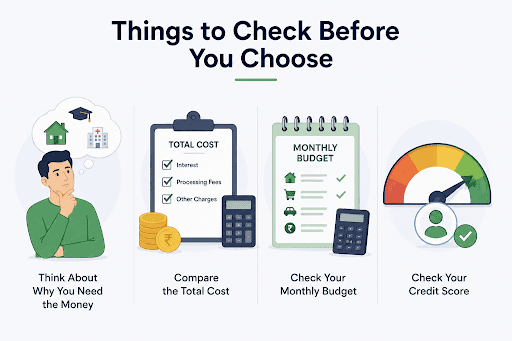

Factors to Consider Before Choosing Between a Personal Loan and a Line of Credit

Every borrower has different needs. Looking at a few simple things before you apply can help you choose the right option.

Think About Why You Need the Money

Start with the reason for borrowing. A personal loan works well when you know the total amount you need. A line of credit may suit you better if your expenses are likely to come over a few weeks or months.

Compare the Total Cost

Do not look only at the interest rate. Check the total amount you may repay before making a decision. Processing fees and other charges can also affect the overall cost.

Check Your Monthly Budget

You should first analyze how much money you can afford for EMIs every month. If you do not want to face difficulties later on, borrow only the amount that you can repay.

Check Your Credit Score

Most lenders check your credit score before approving your application. A good score can improve your chances of getting a loan and may also help you get better terms.

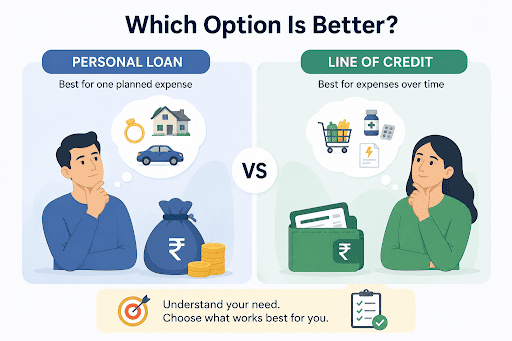

Personal Loan vs Line of Credit: Which Option Is Better?

The answer depends on why you need the money. A personal loan works well for one planned expense, while a line of credit suits expenses that may come up over time. Once you know how you plan to use the money, choosing between the two becomes much easier.

Choose What Works Best for You

Borrowing becomes easier when you understand how each option works. A little planning before you apply can help you save money and avoid repayment stress later.

If you need money for a planned expense, Hero FinCorp offers personal loans with a simple online application process. You can also use the personal loan app to check your eligibility and apply in just a few steps.

Frequently Asked Questions

What is the main difference between a personal loan and a line of credit?

A personal loan gives you the full amount at once. A line of credit lets you borrow money only when you need it.

Is a personal line of credit cheaper than a personal loan?

It can be. In personal line credit, pay interest only on the amount you use.

Which is better for emergencies: a personal loan or a line of credit?

A line of credit can work well for emergencies because you can use funds whenever you need them. You can go for a personal loan if you already know the amount you need.

Do I pay interest on the entire credit limit in a line of credit?

No. You pay interest only on the amount you borrow.

Can I reuse funds after repaying a personal line of credit?

Yes. After you repay the amount you used, that limit becomes available again.

Does a personal loan have fixed monthly payments?

Yes. Most personal loans come with fixed EMIs throughout the loan period.

How do personal loans and lines of credit affect my credit score?

Paying your EMIs or dues on time can improve your credit score. Missing payments can lower it.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Freelancing and gig work are booming in India. In fact, the number has reached over 7.7 million according to NITI Aayog. 21. And that number is set to reach 23.5 million by 2030.

A friend tells you to check your credit report before applying for a loan. You expect everything to look normal, but an active loan appears that you do not recognize. You start panicking and overthinking about now what.

Rohan cleared his credit card bill before applying for a personal loan. Even then, his credit report still showed the old balance, leaving him confused about his score.