Loan Amortization: Meaning, Formula, Schedule & How It Works

- What Is Loan Amortization?

- How Does Loan Amortization Work?

- Loan Amortization Formula Explained

- Example of Loan Amortization

- Types of Loans That Use Amortization

- Benefits of Loan Amortization

- Factors That Affect Loan Amortization

- Loan Amortization vs Loan Term

- How Prepayments Impact Loan Amortization?

- Understanding Your EMI Better

- Frequently Asked Questions

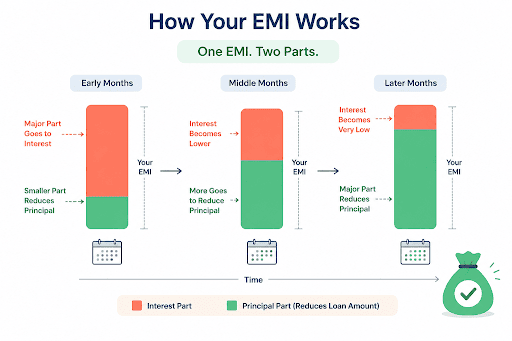

Loan amortization explains how your loan gets repaid little by little through monthly EMIs. Every EMI includes two parts. One part pays the interest, while the other reduces the loan amount.

During the first few months, a bigger share of the EMI goes toward interest because the pending loan amount stays higher. Later, the interest amount starts reducing, and a larger part of the EMI begins cutting down the actual loan balance. This process continues until you repay the full loan.

What Is Loan Amortization?

Loan amortization explains how your loan gets repaid little by little through monthly EMIs. Every EMI includes two parts. One part pays the interest, while the other reduces the loan amount.

During the first few months, a bigger share of the EMI goes toward interest because the pending loan amount stays higher. Later, the interest amount starts reducing, and a larger part of the EMI begins cutting down the actual loan balance. This process continues until you repay the full loan.

How Does Loan Amortization Work?

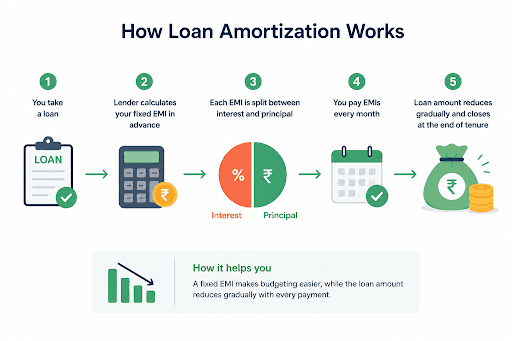

Loan amortization follows a structured repayment system. Lenders calculate the EMI in advance and divide each payment between interest and principal throughout the loan tenure.

Principal and Interest Components

Every EMI contains two parts. One part pays the interest charged by the lender, while the second part reduces the actual loan amount.

Fixed EMI Structure

Most lenders keep EMIs fixed throughout the loan tenure. This helps borrowers manage monthly payments more easily and track repayments.

Changing Interest-to-Principal Ratio Over Time

Interest takes a larger share during the initial months because lenders calculate it on the outstanding balance. Later, the principal share increases as the balance starts falling steadily.

Loan Amortization Formula Explained

Lenders use a standard formula to calculate EMIs and repayment schedules. This formula helps them maintain a structured repayment timeline.

Standard Loan Amortization Formula

EMI = [P × R × (1 + R)^N] ÷ [(1 + R)^N − 1]

Where P stands for the loan amount, R stands for the monthly interest rate, and N stands for the total number of monthly EMIs

Why Lenders Use This Formula

The formula helps lenders calculate fixed EMIs accurately. Borrowers also get a clear repayment structure before taking the loan.

Example of Loan Amortization

A practical example makes loan amortization easier to understand because borrowers can see how EMI distribution changes over time.

Sample Loan Scenario

Loan Amount = ₹5,00,000

Interest Rate = 10% annually

Loan Tenure = 5 years

EMI Breakdown During Initial Months

EMI = Around ₹10,624

Month 1

Interest = ₹4,167

Principal = ₹6,457

Month 2

Interest = ₹4,113

Principal = ₹6,511

EMI Breakdown Near Loan Maturity

During the final months, the interest portion becomes much smaller because the outstanding balance drops significantly. Most of the EMI starts reducing the principal amount directly.

Types of Loans That Use Amortization

Many common loans in India use amortization because lenders collect repayments through structured EMIs.

Personal Loans

Personal loans usually follow shorter repayment schedules with fixed monthly payments.

Home Loans

Home loans use long amortization schedules because borrowers repay them over several years.

Auto Loans

Vehicle loans spread repayments across fixed EMIs to make ownership more manageable.

Education Loans

Education loans also follow amortization once borrowers begin repayment after the moratorium period.

Also Read: What Is the Moratorium Period in a Loan? Meaning and Benefits

Benefits of Loan Amortization

Loan amortization gives borrowers a clear picture of how their loan gets repaid month after month. It also makes EMIs easier to understand and track during the repayment period.

Predictable Monthly Payments

Fixed EMIs help borrowers understand how much money they need every month for repayments.

Structured Debt Repayment

Each EMI reduces the loan balance step by step throughout the repayment period.

Better Financial Planning

Borrowers can plan savings and future expenses with greater confidence.

Clear Loan Closure Timeline

Amortization schedules clearly show when the loan will end.

Factors That Affect Loan Amortization

Several factors directly influence EMI structure and repayment speed.

Loan Amount

Higher loan amounts increase both EMIs and overall interest costs.

Interest Rate

A higher interest rate increases the interest portion within every EMI.

Loan Tenure

Longer tenures reduce monthly EMIs but increase total interest payments.

Prepayments and Part-Payments

Prepayments reduce the outstanding balance faster and improve repayment efficiency.

Loan Amortization vs Loan Term

Loan amortization explains how lenders divide EMIs across the repayment period, while the loan term simply refers to the total duration of the loan. One explains repayment structure, and the other explains repayment length.

How Prepayments Impact Loan Amortization?

Prepayments directly reduce the outstanding loan amount before schedule. This changes the repayment structure in the borrower’s favour.

Reduction in Interest Cost

Lower balances reduce future interest charges significantly.

Shorter Repayment Tenure

Prepayments may help borrowers close loans earlier than planned.

Faster Principal Reduction

A larger share of future EMIs starts reducing the principal amount directly.

Understanding Your EMI Better

Loan amortization helps you understand where your EMI money goes every month and why the loan balance reduces slowly in the beginning. Once you understand this repayment pattern, managing EMIs and planning part payments feels much easier.

If you are looking for a personal loan, choose a lender that keeps the process simple from start to finish. Hero FinCorp offers quick digital access, easy repayment tracking, and flexible loan options designed around your needs. Check your eligibility online and apply now for a smooth borrowing experience.

Frequently Asked Questions

What is the meaning of loan amortization?

Loan amortization means repaying a loan gradually through fixed EMIs over a specific period.

What is the loan amortization formula?

EMI = [Loan amount × monthly interest rate × (1 + monthly interest rate)^total number of EMIs] ÷ [(1 + Monthly interest rate)^total number of EMIs − 1].

What is an amortization schedule?

An amortization schedule shows how every EMI gets divided between interest and principal.

Why do early EMIs contain more interest than principal?

Lenders calculate interest on the outstanding balance, which remains highest during the initial months

Which loans are typically amortized?

Loans such as home loans, personal loans, auto loans, and education loans are amortized.

Can prepayment reduce the amortization period?

Yes. Prepayments can reduce the amortization period.

How does loan tenure affect amortization?

Longer tenures reduce EMIs but increase the total interest paid across the loan period.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.